Reviving National Family Benefit Scheme

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

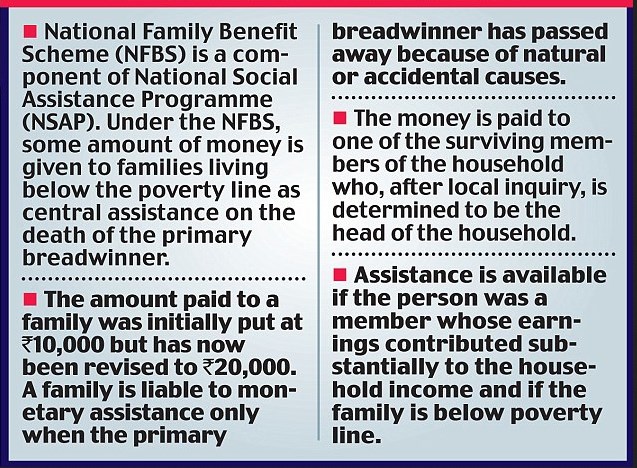

What is National Family Benefit Scheme?

- The NFBS or National Family Benefit Scheme was launched under the National Social Assistance Program in 1995.

- It was a significant step towards the fulfilment of the state’s responsibility of providing public assistance to citizens in case of sickness, disablement, old age, unemployment, etc.- as provided for in Article 41 of the Constitution.

Why isn’t the scheme delivering?

- The scheme covers only those below the poverty line (BPL families).

- It provides only 20,000 INR as emergency assistance to the beneficiaries. In addition to this, the formalities are often daunting for the applicants.

- The NSAP is facing neglect in these recent years. For example, the centre’s contribution to old age pensions has stagnated at a meagre sum of 200 INR/ month for some 15 years. There have been repeated calls for an increase in the contribution, including an open letter in 2018 from many eminent economists, but to no avail.

- The scheme’s budget has been stagnating– making it difficult to increase the benefits or the coverage. There has been a decline in central expenditure on this scheme between 2014-15 (862 crore INR) and 2020-21 (623 crore INR) according to budget estimates. This shows that the scheme is being phased out gradually.

- The NSAP is being undermined in order to promote contributory schemes like APY (Atal Pension Yojana). Such schemes require the beneficiaries to be able to save up, comprehend formalities and trust their money with the government. Hence, these contributory schemes don’t suit the conditions and requirements of the poorest who have little literacy and low earnings.

- The Mihir Shah task force submitted a report on NSAP in 2013. This report included many recommendations for improving the NFBS. Some have even influenced the 2014 revised guidelines for NSAP. Eg: the eligibility for assistance under NFBS was extended to cases where an adult woman (18-60 year old), who works at home, dies. However, no corresponding financial provision was made. The main recommendations on coverage and benefits were ignored.

How can the scheme be revived?

- A substantial increase in the amount given out as emergency assistance is long overdue. One of the 2013 task force members, K P Kannan said that the initial intention was to set the benefits at 80% of the country’s per capita GDP. In this light, the benefits should be increased to nearly 1 lakh INR. Even this amount isn’t sufficient for a poor family to survive with dignity, but it would atleast help.

- The restriction of the scheme’s applicability to BPL households should be removed. This is because BPL lists are unreliable, outdated and bear exclusion errors in most of the states. In the past 2 decades, most social security programs have shifted away from the use of BPL targeting-

- School meal programs are universal

- MGNREGS is self-targeted

- In some states, PDS is based on ‘exclusion approach’– i.e., privileged households are excluded from the beneficiary list based on simple criteria and leaves all the rest eligible for the benefits by default.

- The formalities under the scheme are in dire need of transparency, simplification and people-friendliness.

- Currently, the identification of beneficiary families is the responsibility of the municipalities or the Gram Panchayats. Though this isn’t a bad thing, the applications are moved through the block level and district level bureaucracy for months. Meanwhile, the applicants are left without any means of tracking the applications or of demanding a timely response.

- Better facilities must be put in place to enable access to information and assistance for completing formalities, tracking applications, submitting complaints and grievance redressal.

- Timely disbursal of the scheme’s benefits could be achieved if compensations are given to the beneficiaries in case of delays.

- Significantly increasing the scheme’s budget is a major requirement. For starter, the coverage could be doubled to 7.2 lakh families/ year and the benefits could be enhanced to 1 lakh INR/ family. In this case, the annual cost would come to 7,200 crore INR– 10 times more than the current budget for NFBS. However, the sum is still modest given the importance of such a national scheme for social security.

Conclusion:

For a poor household, losing a breadwinner is a serious contingency. With the advent of the COVID-19 pandemic, this is a situation being faced by many poor households. A revamped NFBS could have helped many of these families tide through such a critical period. Revival of this scheme could help address the gap in our social security system- especially in the absence of an appropriate life insurance for poor households.

Referred Sources

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses