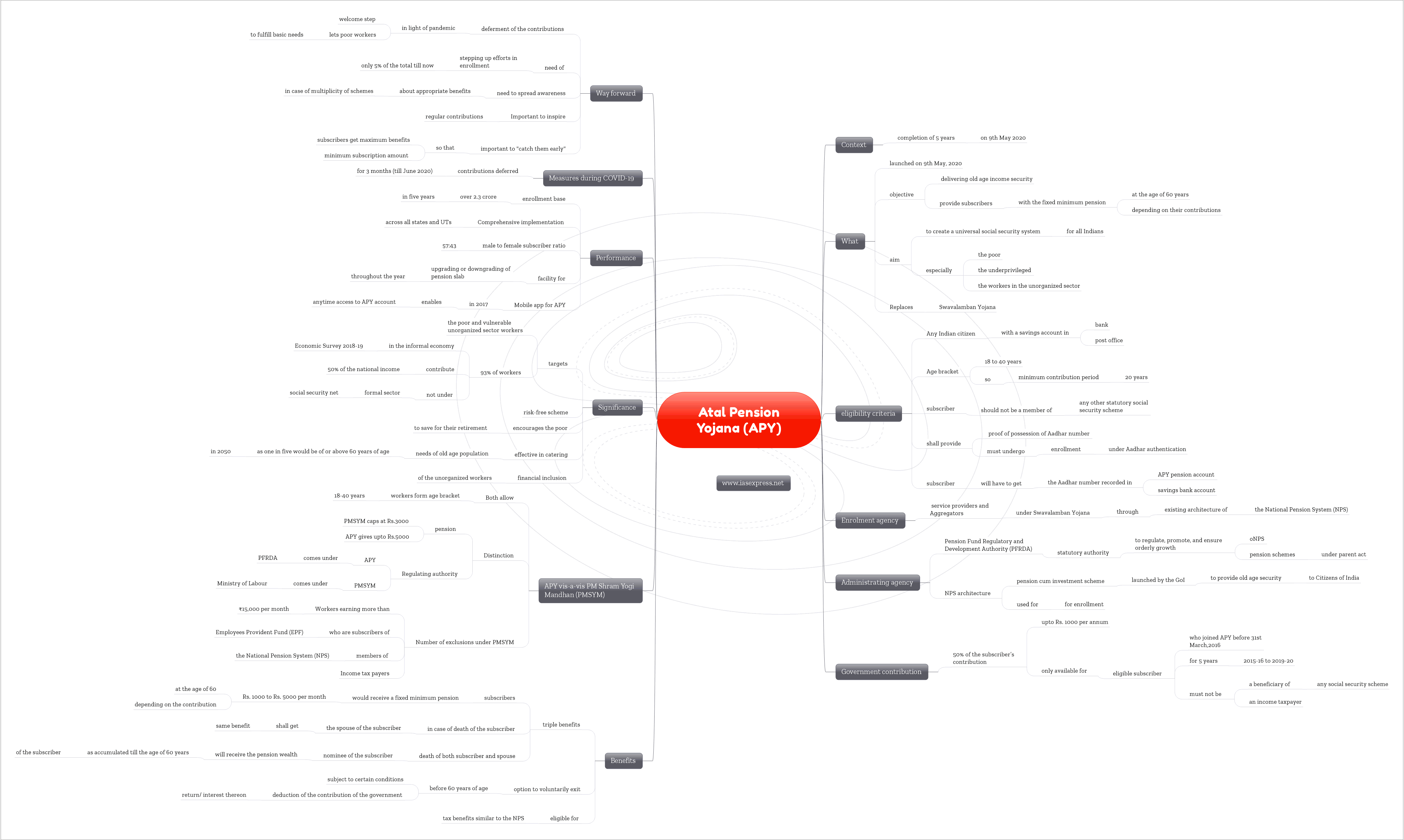

Atal Pension Yojana: Features, Significance, Achievements in five years

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

In a country where around 90% workforce is engaged in an unorganized sector, the framing of social security schemes is a very challenging task. The humungous population with dynamic demographic patterns, diverse socio-economic conditions from state to state, and huge informal sector make the task of designing a foolproof scheme faces many structural and functional challenges. On this backdrop the Atal Pension Yojana, the flagship social security scheme, must be analyzed for its efficacy. Recently, it completed five years of its operation.

What is Atal Pension Yojana (APY)?

- The APY was launched on 9th May, 2020 with an objective of delivering old age income security.

- It aims to create a universal social security system for all Indians, especially the poor,

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses