Forensic Audit – Meaning, Importance, Way Ahead

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

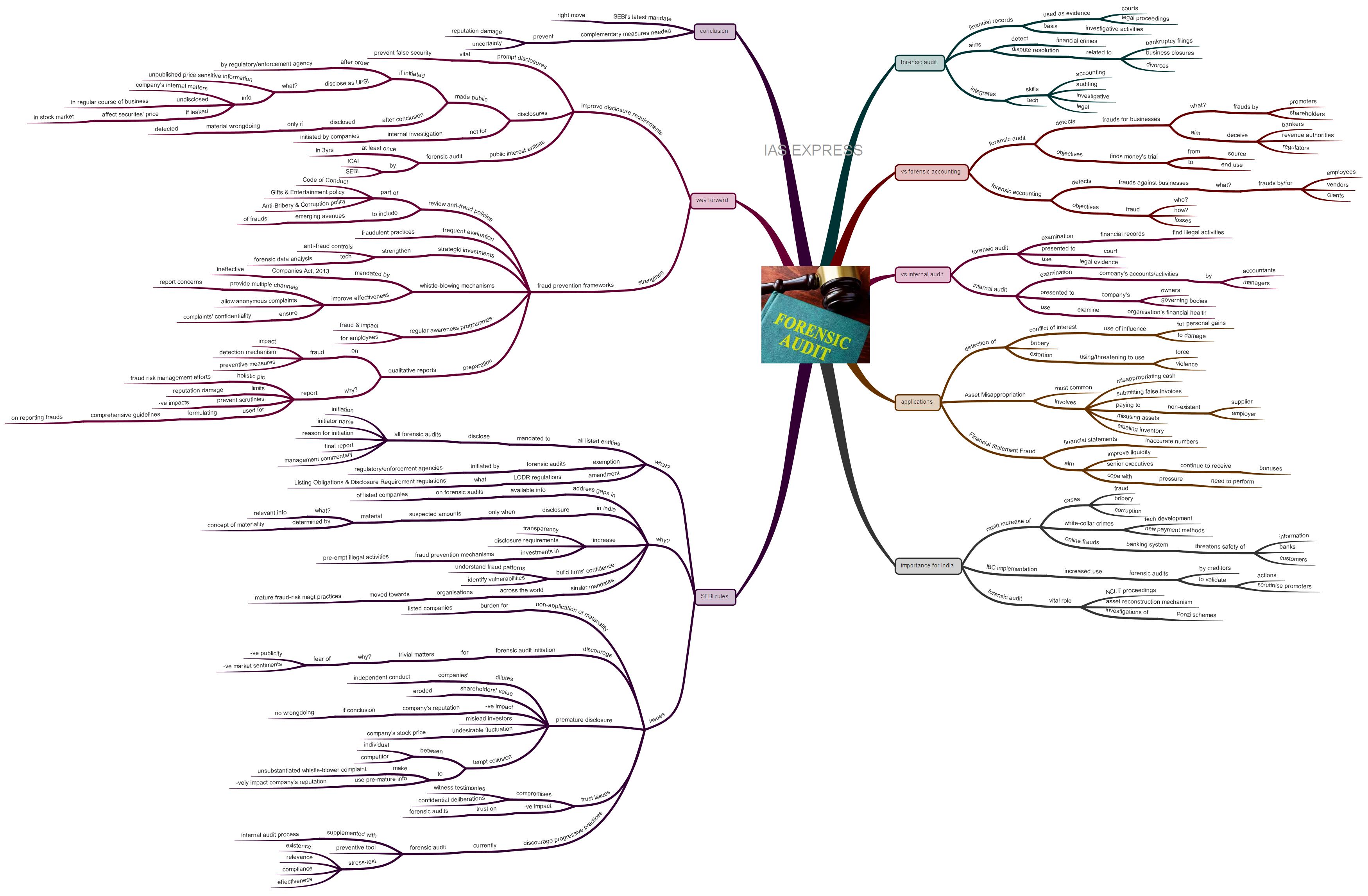

Securities and Exchange Board of India (SEBI) has amended Listing Obligations and Disclosure Requirement (LODR) regulations to remove the gaps in the availability of information on forensic audits of listed entities. However, companies may regard these requirements as onerous, as they may adversely impact their reputation. Measures must be taken to address this issue for intended objectives of improving transparency and increasing disclosure requirements to be effectively achieved.

What is a forensic audit?

- “Forensic” means “suitable for use in a court of law”.

- A forensic audit is the examination and evaluation of an individual’s or firm’s financial records to derive evidence that can be used

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses