Reinsurance

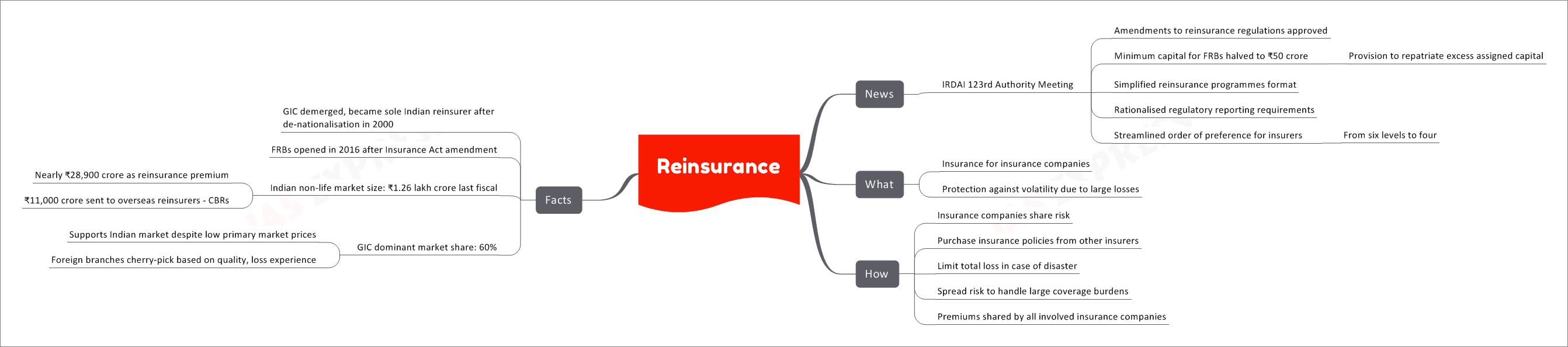

In the recently held IRDAI 123rd Authority Meeting, significant amendments to reinsurance regulations were approved, reflecting efforts to enhance the insurance landscape in India. Reinsurance, a vital component of the insurance industry, serves as a safety net for insurance companies, protecting them from the impact of substantial losses.

Understanding Reinsurance

What is Reinsurance?

Reinsurance can be understood as insurance for insurance companies. It’s a mechanism designed to shield insurers from the volatility that can arise due to large and unexpected losses. Through reinsurance, insurance companies transfer a portion of their risks to other insurers, thereby minimizing their exposure to potential financial shocks.

Sharing Risk for Stability

The process of reinsurance involves insurance companies sharing their risks with other insurers. This is done by purchasing insurance policies from these reinsurers. By doing so, insurance companies limit their potential losses in the event of a disaster or major claim. This strategy also allows them to spread the risk associated with large coverage obligations.

A Collaborative Approach

Reinsurance operates on the principle of shared responsibility. The premiums paid by policyholders are not solely absorbed by the primary insurance companies; they are distributed among all the insurers involved in the reinsurance arrangement. This equitable distribution of premiums ensures that the financial impact of substantial claims is absorbed collectively.

Key Facts and Market Dynamics

Evolution of Reinsurance in India

- Following its demerger and the subsequent de-nationalization in 2000, GIC (General Insurance Corporation) emerged as the sole Indian reinsurer.

- Foreign Reinsurers Branches (FRBs) were introduced in 2016, following an amendment to the Insurance Act.

Reinsurance’s Role in the Indian Insurance Landscape

- In the Indian non-life insurance market, the total size was approximately ₹1.26 lakh crore in the last fiscal year.

- Of this, nearly ₹28,900 crore was in the form of reinsurance premiums.

- A significant portion of these reinsurance premiums, approximately ₹11,000 crore, were ceded to overseas reinsurers known as Cross Border Reinsurers (CBRs).

- GIC, with a dominant market share of 60%, plays a pivotal role in supporting the Indian market, even amid challenges posed by low primary market prices.

Ensuring Quality and Mitigating Risk

- Foreign branches of reinsurers tend to select risks based on quality and loss experience. This practice ensures a well-balanced portfolio that enhances stability for both the primary insurers and reinsurers.

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses