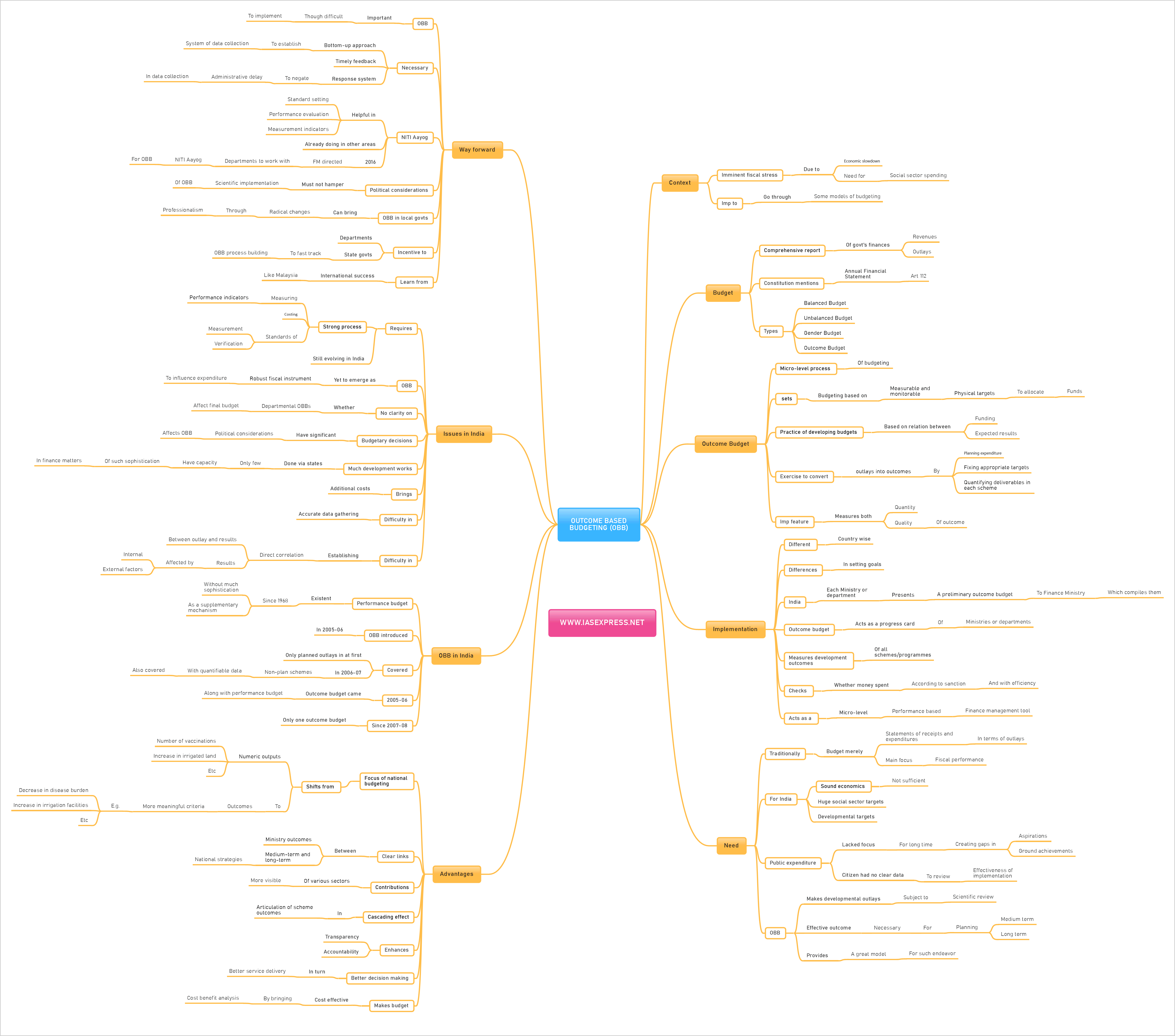

Outcome Based Budgeting: Features, Advantages, Issues

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

As the government of India grapples with the fiscal deficit issues in the wake of slowdown in the economy, there is a rising churn about the fiscal management of government. As the fiscal strategy is one of the functions of budgetary process, it is important to understand some of the key models in budgetary effectivity. The Outcome based budgeting is on such model of budgeting which strives to bring result-based decision making.

What is a Budget?

- Budget is a comprehensive report of the government’s finances in which revenue from all sources and outlays for all activities are consolidated.

- The Budget also contains estimates for the government’s accounts for the next fiscal year which is called budget estimates.

- The term budget is of British origin and not mentioned in Indian constitution. It uses the term Annual Financial Statement under article 112.

- Budgets are of different types such as

Balanced Budget: Estimates of government receipts are equal to estimated government expenditure

Unbalanced Budget: Estimates of governments receipts are not equal (less or more) than estimated government expenditure

Gender Budget: A general budget by the government which allocates funds and responsibilities on the basis of gender is gender budgeting. It started in India with the union budget of 2006-07.

Outcome Budget: It is a kind of result-oriented budgeting process. We shall see this type in detail below.

What is an outcome budget or outcome-based budget (OBB)?

- The outcome budget is a micro-level process of budgeting that sets measurable and monitorable physical targets for the allocation on every plan project under various ministries.

- It is the practice of developing budgets based on the relationship between funding and expected results.

- An important feature of outcome-based budget is that it not only measures quantitative outcome of the budget but also in terms of quality of outcomes. Both quantitative and qualitative perspectives are given equal importance.

- The conventional budget indicates the resources allocated to various programmes and schemes of the government, but does not focus much on the use of those resources to achieve certain agreed results.

- OBB is an exercise to convert outlays into outcomes by planning the expenditure, fixing appropriate targets, quantifying deliverables in each scheme and bringing to the knowledge of all, the outcomes for each scheme/programme.

- So, it is effectively an effort of the government to be accountable and transparent to the people.

What is the procedure of OBB?

- The OBB practice varies from country to country. There are differences in setting goals such as whether output or outcome should be considered as the basic of assessment. Outputs are things such as roads to rebuild, number of vaccinations done, area to be irrigated etc. while outcome means indicators of progress achieved such as decline in disease, infrastructure improvement, achievements in education etc.

- Under OBB, each ministry presents a preliminary outcome budget to the Finance Ministry, which then compiles them.

- The Outcome budget becomes a progress card on what various Ministries and Departments have done with the outlays in the previous annual budget.

- It measures the development outcomes of all government programmes and checks whether money has been spent for the purpose it was sanctioned including the outcome of the fund usage.

- It acts as a micro-level performance-based finance planning and management tool.

Why outcome-based budget is needed?

- Traditionally, budget has been viewed merely as a statement of receipts and expenditure in terms of outlays.

- The budget focus has been prioritizing fiscal deficit containment and increasing outlays for each scheme, programme, Ministry.

- But for a country like India, only a sound economics is not sufficient as we are still a developing nation. We have huge targets to be achieved in social sectors such as poverty alleviation, literacy, health infrastructure, etc.

- Public expenditure in India for long time lacked focus and outcomes that matter to the citizens were not being achieved. Such attitude leaves big gaps in aspirations and ground achievements.

- Merely outlayswithout any scientific performance review is not sufficient as the process of development must be efficient and effective as well as speedy so as to bring more population under good human development scenario.

- Also, the citizenry has no clear data on performance/outcome of different schemes vis-à-vis their outlays.

- The efficiency in outcome is of key importance as it gives relative and absolute improvements in performance of different departments and Ministries and helps in medium- and long-term planning.

- In such a scenario, outcome-based budgeting provides a model of transparent and improvement based financial planning.

What are the advantages of outcome-based budgeting?

- The focus of national budgeting shifts from numeric outputs to more meaningful criteria. outcomes.

- With OBB, clear links are established between ministry outcomes and the medium-term and long-term national strategies.

- Contributions of various sectors of economy becomes clearer and more visible.

- OBB helps in cascading effect in articulation of scheme outcomes with key performance indicators established at both levels.

- OBB enhances transparency and accountability with schemes being defined for positive interventions rather than mere numeric improvement.

- OBB results in better decision making and in turn better last-mile service delivery.

- It makes budget cost effective as it brings in cost-benefit analysis into budgeting process by better result analysis of failing schemes and proper direction.

Outcome based budgeting in India

- The performance budget had been in existence in India since 1968 when government departments started linking financial aspects with physical results. However, this remained a supplementary activity without any impact.

- To bring in professionalism and transparency in India, outcome budget was introduced in India as a revision of earlier performance budgeting in 2005-06.

- For the first time in 2005-06, the outcome budget was presented to the parliament covering only plan outlays. In 2006-07, non-plan schemes with quantifiable and deliverable outputs were also covered.

- In 2005-06, the achievements of outcome budget were presented in the form of a performance budget. But since 2007-08, the outcome and performance budget have been merged and is presented to the parliament as a combined document, i.e., the Outcome budget.

What are issues with the outcome budgeting in India?

- The management of Outcome budgets requires a strong process-measuring the performance indicators, costing the services and programmes.

- The building blocks of OBB such as standard specifications, measurement of performance indicators, and evaluating and ma are still evolving in India.

- The OBB is yet to emerge as a robust fiscal instrument to influence the decision over public expenditure.

- As the regular budget is presented in parliament is a separate process as compared to the Ministry-wise outcome budgets presented later, it is unclear whether outcome budget influences the main budget allocations in any substantial way.

- The budgetary decisions have significant political considerations which largely affect the scientific implementation of OBB.

- Much of the developmental works in India are done via stategovernments. Here, other than few relatively developed states, much of the states’ machinery is yet to adopt such sophistication in budget planning.

- It results in additional costs as additional analysis has to be done for assigning funds.

- Getting accurate outcome data is difficult and outcomes are driven by multiple internal and external factors. So. It is difficult to derive a direct correlation between resources delayed and outcome achieved.

Way forward

- The transformation from the comforts of outlay budget to fully functional outcome budget is difficult yet not impossible.

- It is necessary to bring operational standards in a bottom-up approach so that flow of data becomes more robust and data driven outcome budgeting is possible.

- A timely feedback system and response system is necessary for implementing OBB as the data on various departmental performance is a little delayed due to administrative causes.

- There is a need to build proper standards of evaluation, performance indicators and implementation strategies further. NITI Aayog as research and analysis think tank of the government must work on this. It has developed many good indicators for other sectors such as water management.

- In 2016, this has already begun as the Finance Ministry has directed that each ministry and department must prepare outcome budget in consultation with the NITI Aayog.

- Budgeting is a primarily a developmental driver in India. Hence, political considerations must be minimized in scientific OBB process.

- OBB in local governments can bring radical changes in working of local self-governments by aligning finance commission outlays with performance.

- The Union government can guide the states in developing processes and implementation machinery in a planned way so that synergies are developed in overall data collection and programme implementation.

- Success of such endeavor will also depend on incentives for adopting required measures. Union government can consider such incentive-based nudging.

- There are international success stories such as Malaysia which are recognized by World Bank. India must learn the experiences trough collaborations.

Conclusion

The public finance management in India is a critical process as we are short of investment and also have huge developmental targets. To negate leakages, underperformance and to bring in professional effectiveness in budget implementation, Outcome based budgeting is a handy process. India needs to further finetune OBB to achieve targets of social sector and economic prudence.

Practice Question for Mains

What is Outcome based budgeting? Critically analyze its importance in social sector development in India. (250 words)

https://www.outlookindia.com/newswire/story/chidambaram-unveils-maiden-outcome-budget/318992

https://www.business-standard.com/about/what-is-outcome-budget

https://www.deccanherald.com/business/budget-2020/budget-faq-what-is-outcome-budget-799691.html

https://www.pwc.com.au/consulting/assets/publications/pwc-consulting-outcome-based-budgeting.pdf

https://www.indianeconomy.net/splclassroom/what-is-outcome-budgeting/

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Very helpful