NPA Crisis in India – Reasons and Responses

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

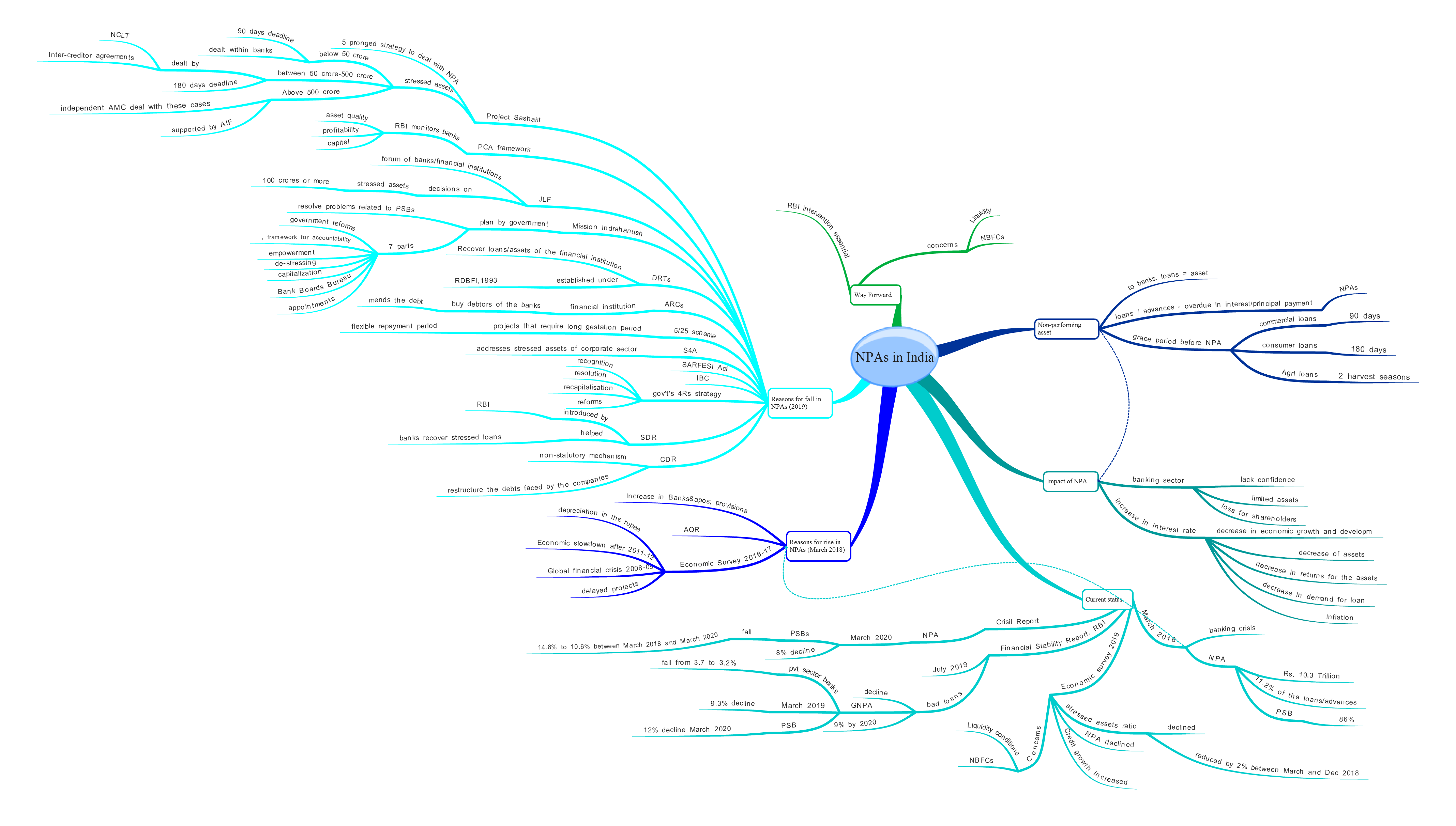

According to the Economic Survey 2018-2019, the functioning of the banking sector has improved due to the decrease in the Non-performing assets (NPAs) and an increase in credit growth. The gross NPAs of the public sector banks have declined from 11.5% to 10.1%, between March 2018 and December 2018.

What is NPA?

- To banks, loans given by it are called assets.

- Non-performing assets are those loans/advances which are in default or arrears on scheduled payments of principal or interests.

- This means that the assets are termed to be NPAs if the interests/principles are unpaid more than the specified time

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses