Disinvestment of Public Sector Units (PSUs) in India – Pros and Cons

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

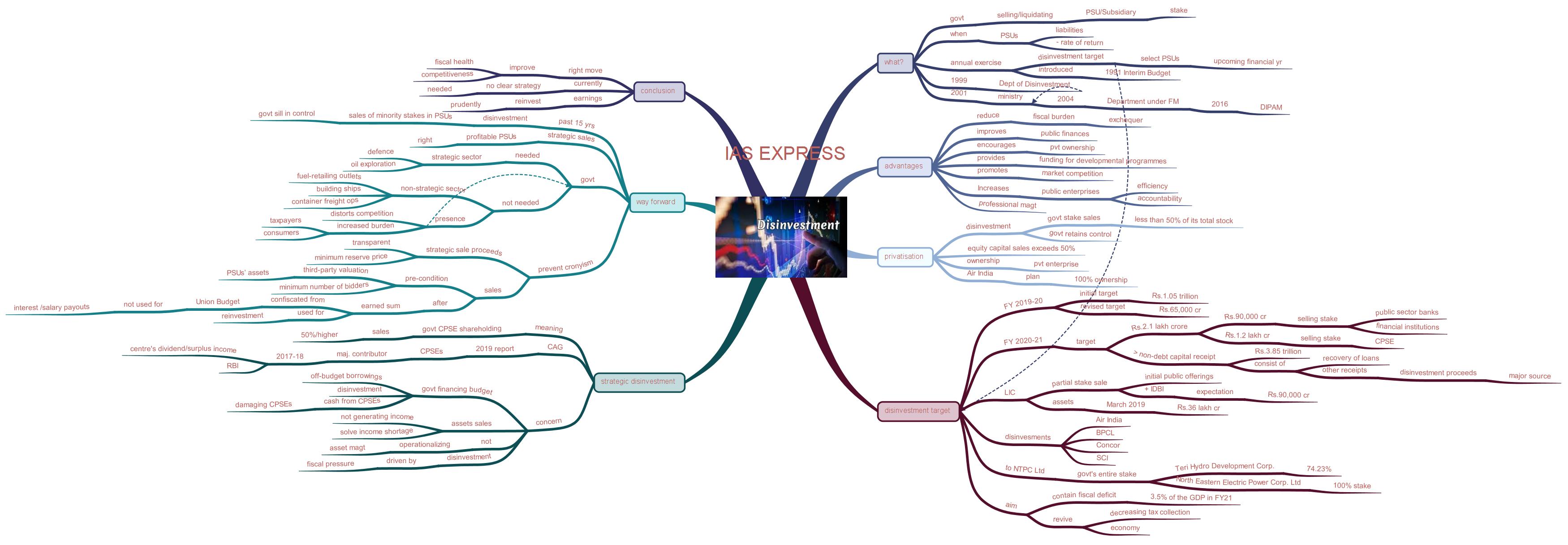

The government has set a disinvestment target for 2020-2021 to Rs.2.10 lakh crore, having failed to achieve the current fiscal year’s target of Rs.1.05 lakh crore. It hopes to achieve the unmet target of this fiscal year in the next fiscal year. A large part is likely to come from the sale of stakes in Life Insurance Corporation and IDBI bank. However, the strategy of how this target is going to be achieved is absent. Nevertheless, selling off stakes from high return public enterprises like LIC can ensure the achievement of targets set by the government. Achieving this alone is not enough. The government must use these earnings not to pay off its loans or achieve its fiscal deficit target but to reinvest in aspects that ensure improvement in economic growth and sustainable returns.

What is d

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses