Gold Monetization Scheme & Sovereign Gold Bond Scheme – Success or Failure?

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

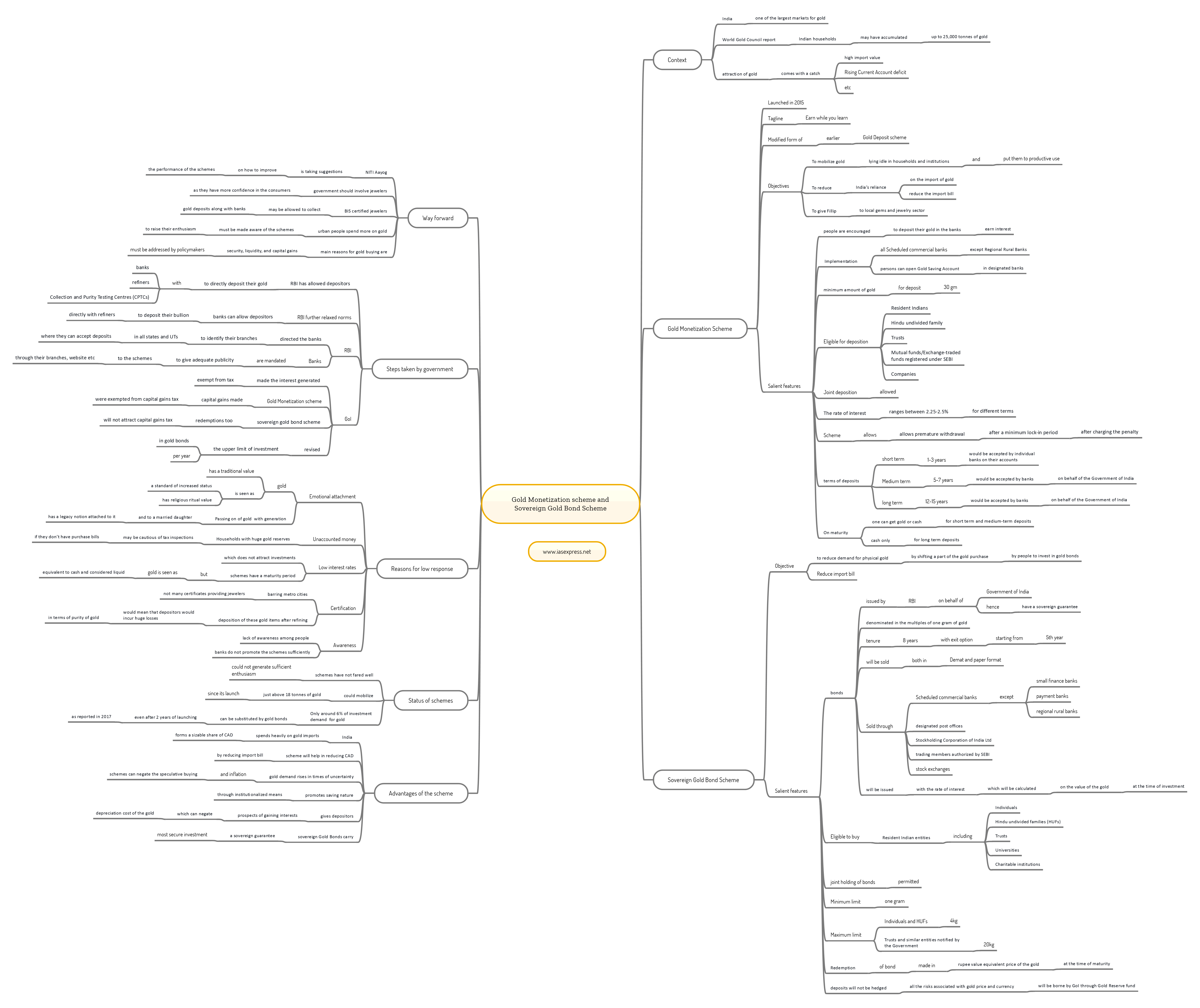

India has been one of the largest markets for gold. Its growing affluence is making the demand to grow even more. Gold has an important place in the country’s culture. Gold has a store of value, is a symbol of wealth and status and a fundamental part of many rituals. Indian households may have accumulated up to 25,000 tonnes of gold, thereby retaining the tag of the world’s largest holders of the metal, according to the World Gold Council (WGC). The attraction of gold comes with a catch of high import value among other things. So, the government of India launched the two schemes to attract investment and provide earning options to the people.

Gold monetization scheme

The Gold monetization scheme was launched with the tagline of ‘Earn, while you secure’ in November 2015. It is a modified form of the earlier Gold deposit scheme (GDS).

What are its objectives?

- To mobilize gold lying idle in households and institutions and put them to productive use.

- To reduce India’s reliance on the import of gold and reduce the import bill.

- To give Fillip to local gems and jewelry sector by making them gold available as raw material

What are the salient features of the scheme?

- The people are encouraged to deposit their gold in the banks and earn interest rather than lying idle in their homes unproductively

- Implementation – According to RBI guidelines, all the scheduled commercial banks (except Regional Rural Banks) can implement this scheme

- The persons can open Gold Saving Account in designated banks and anyone can deposit physical gold (via BIS certified collection, purity testing centers (CPTCs)).

- The minimum amount of gold thus deposited is 30 gm and has no upper limit.

Eligibility for deposition

- Resident Indians

- Hindu undivided family

- Trusts

- Mutual funds/Exchange-traded funds registered under SEBI

- Companies

- Joint deposits are allowed with a minimum of two holders with no cap on the maximum number.

- The rate of interest ranges between 2.25-2.5% for different terms.

- after a minimum lock-in period, the scheme allows premature withdrawal after charging the penalty for such withdrawals.

- There are three kinds of terms for gold deposition. For the short term the term is 1-3 years, medium-term is 5-7 years and the long term is 12-15 years.

- Short term deposits would be accepted by individual banks on their accounts. The medium-term and long-term deposits would be accepted by banks on behalf of the Government of India.

- On maturity, one can get gold or cash for short term and medium-term deposits, and cash only for long term deposits.

Sovereign Gold Bond (SGB) Scheme

Along with Gold Monetization Scheme, the government of India launched the Sovereign gold bond scheme

What are its objectives?

Its objective is to reduce demand for physical gold by shifting a part of the gold purchase by people to invest in gold bonds.

What are the salient features of the scheme?

- The bonds are issued by the Reserve Bank of India on behalf of the Government of India. Hence the bonds will have a sovereign guarantee.

- The SGBs are denominated in the multiples of one gram of gold.

- The tenure of the bond is 8 years with an exit option starting from the 5th year onwards.

- The bonds will be sold both in Demat and paper format.

- These bonds are sold through scheduled commercial banks (Except small finance banks, payment banks, RRBs), designated post offices, Stockholding Corporation of India Ltd, trading members authorized by SEBI, stock exchanges.

- Eligibility- Resident Indian entities including

- Individuals

- Hindu undivided families (HUF)

- Trusts

- Universities

- Charitable institutions

- Joint holding is permitted.

- The minimum investment limit is one gram of gold and maximum limits are

- Individuals- 4kg

- HUF- 4kg

- Trusts and similar entities notified by the Government- 20kg

- The bonds will be issued with the rate of interest which will be calculated on the value of the gold at the time of investment.

- These bonds can be issued as collateral for loans.

- Redemption is made in rupee value equivalent price of the gold at the time of maturity.

- The deposits will not be hedged and all the risks associated with gold price and currency will be borne by GoI through Gold Reserve fund. The Gold reserve fund is a fund created to serve this purpose only.

What are the advantages of these schemes?

- India spends heavily on gold imports. It forms a sizable share of CAD along with crude imports. This scheme will help in reducing CAD by reducing import bill.

- The gold demand rises in times of uncertainty (as can be seen now as COVID-19 impact began to rise) and inflation. The schemes can negate the speculative buying.

- It promotes saving nature through institutionalized means.

- It gives depositors prospects of gaining interests which can negate the depreciation cost of the gold.

- The sovereign Gold Bonds carry a sovereign guarantee. It is one of the most secure means of investment.

How successful the schemes are?

- The schemes have not fared well as they could not generate sufficient enthusiasm among the people.

- It could mobilize just above 18 tonnes of gold since its launch.

- Only around 6% of investment demand for gold can be substituted by gold bonds even after 2 years of launching as reported in 2017.

What are the reasons for the low response?

- Emotional attachment

Most of the gold stock in houses has a traditional attachment value. It is seen as a standard of increased status, has religious ritual value. Passing on of gold with generation and to a married daughter has a legacy notion attached to it.

- Unaccounted money

Households with huge gold reserves may be cautious of tax inspections if they don’t have purchase bills.

- Low-interest rates

The interest rates are low which does not attract investments. The schemes have a maturity period. Gold is seen as equivalent to cash and considered liquid.

- Certification

In India, barring metro cities, there are not many certificates providing jewelers. The deposition of these gold items after refining would mean that depositors would incur huge losses in terms of purity of gold they hold.

- Awareness

There is a lack of awareness among people to generate sufficient interest. The banks do not promote the schemes sufficiently.

What are the steps taken by the government to improve the situation?

- Last year, RBI has allowed depositors to directly deposit their gold with either banks, refiners, or Collection and Purity Testing Centres (CPTCs).

- The RBI has further relaxed norms by which banks can allow depositors to deposit their bullion directly with refiners.

- It has also directed the banks to identify their branches in all states and UTs where they can accept deposits. They are mandated to give adequate publicity to the schemes through their branches, websites, etc.

- The government has given a tax boost to the schemes. The Union Budget 2016-17 made the interest generated exempt from tax. In Gold monetization scheme, capital gains made were exempted from capital gains tax. The sovereign gold bond scheme redemptions too will not attract capital gains tax.

- The government has revised the upper limit of investment in gold bonds per fiscal year.

Way forward

- NITI Aayog is taking suggestions on how to improve the performance of the schemes.

- Among many suggestions, one was that the government should involve jewelers as they have more confidence in the consumers. BIS certified jewellers may be allowed to collect gold deposits along with banks.

- The urban people spend more on gold. They must be made aware of the schemes to raise their enthusiasm.

- The main reasons for gold buying are security, liquidity, and capital gains. These concerns must be addressed by policymakers.

Practice Question for Mains

Critically examine the Gold Monetization Scheme and Sovereign Bond Schemes. Suggest measures to improve their performance. (250 words.)

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses