RBI’s Surplus Fund and its Transfer – All You Need to Know

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

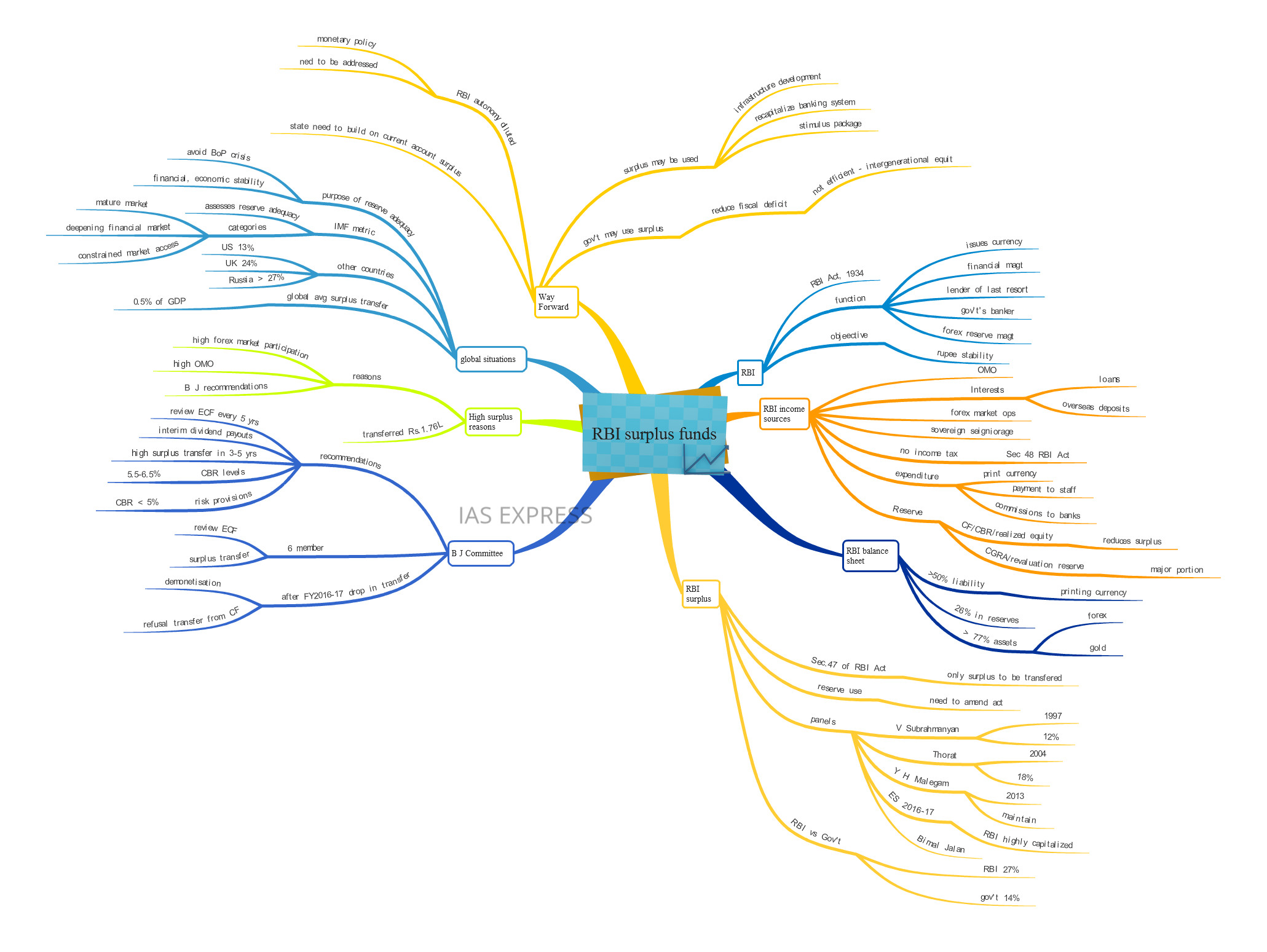

In August 2019, the Reserve Bank of India transferred a record amount of surplus to the Government. The 1.76 lakh crore INR transferred is the highest ever transfer by the apex bank. This amount includes a portion from the RBI’s dividends and a portion from excess surpluses.

What is RBI?

- RBI is the apex bank of India. It was established as an entity held by private stakeholders in 1935. In 1949, the Reserve Bank of India was nationalised and currently has the government as its sole owner.

- It functions under the RBI Act, 1934.

- Its functions include financial management, the lender of last resort, government’s banker, issues currency, forex reserve management, etc.

Wha

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses