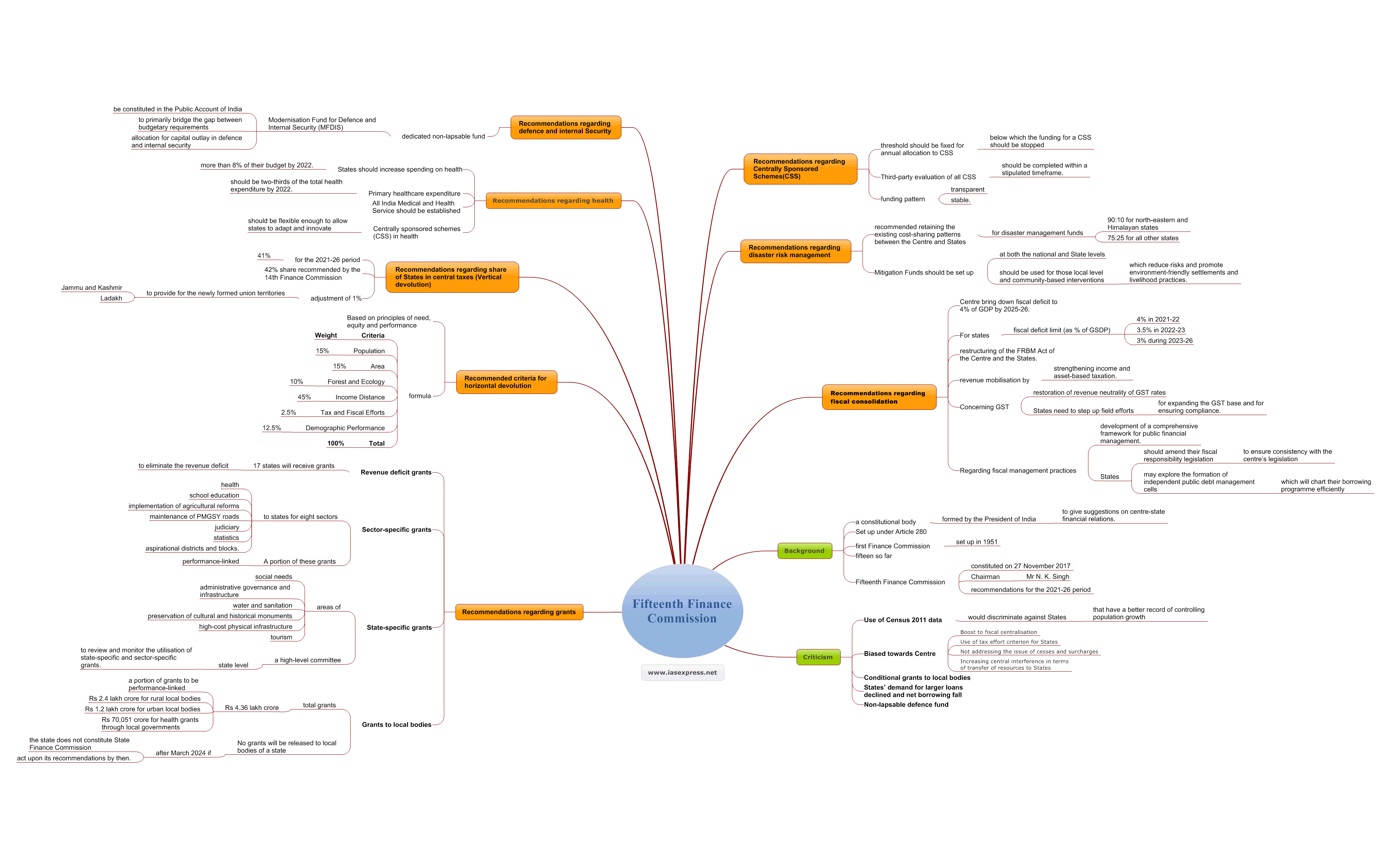

Fifteenth Finance Commission – Background, Recommendations and Criticism

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

The Finance Commission of India deals with the sharing of revenue between the States and the Centre and it has a major role to play in maintaining fiscal federalism through its recommendations. The latest report by the Fifteenth Finance Commission consisting of recommendations for the 2021-26 period has dealt with several issues keeping in mind the needs of the States and Centre. The Finance Commission has been described as the balancing wheel in the Constitution because it is designed to correct the structural and inherent imbalances between the resources and the expenditure of the Union and the States. The Commission faced the unprecedented challenge of making projections and recommendations under the most uncertain circumstances yet it consistently tried to balance the views of all the stakeholders to achieve efficient, equitable, inclusive solutions in this extremely diverse country.

Background

- The Finance Commission is a constitutional body formed by the President of India to give suggestions on centre-state financial relations.

- Set up under Article 280 of the Constitution, its core responsibility is to evaluate the state of finances of the Union and State Governments, recommend the sharing of taxes between them, and lay down the principles determining the distribution of these taxes among States.

- The first Finance Commission was set up in 1951 and there have been fifteen so far.

- The Fifteenth Finance Commission was constituted on 27 November 2017 against the backdrop of the abolition of the Planning Commission and the introduction of the Goods and Services Tax (GST), which has fundamentally redefined federal fiscal relations.

- The Chairman of the Fifteenth Finance Commission was Mr N. K. Singh.

Key Recommendations

- Share of states in central taxes (Vertical devolution)

- The share of states in the central taxes for the 2021-26 period is recommended to be 41%, the same as that for 2020-21.

- This is less than the 42% share recommended by the 14th Finance Commission for the 2015-20 period.

- The adjustment of 1% is to provide for the newly formed union territories of Jammu and Kashmir, and Ladakh from the resources of the Centre.

- Criteria for horizontal devolution

- Based on principles of need, equity and performance, the overall devolution formula is as follows.

Criteria | Weight |

Population | 15% |

Area | 15% |

Forest and Ecology | 10% |

Income Distance | 45% |

Tax and Fiscal Efforts | 2.5% |

Demographic Performance | 12.5% |

Total | 100% |

- Income distance: Income distance is the distance of a state’s income from the state with the highest income. The income of a state has been computed as the average per capita GSDP during the three years between 2016-17 and 2018-19. A state with a lower per capita income will have a higher share to maintain equity among states.

- Demographic performance: The Terms of Reference of the Commission required it to use the population data of 2011 while making recommendations. Accordingly, the Commission used 2011 population data for its recommendations. The demographic performance criterion has been used to reward efforts made by states in controlling their population. States with a lower fertility ratio will be scored higher on this criterion.

- Forest and ecology: This criterion has been arrived at by calculating the share of the dense forest of each state in the total dense forest of all the states.

- Tax and fiscal efforts: This criterion has been used to reward states with higher tax collection efficiency. It is measured as the ratio of the average per capita own tax revenue and the average per capita state GDP during the three years between 2016-17 and 2018-19.

- Population – The population data referred to is of Census 2011 as the 15th Finance Commission thinks Census 2011 data better represents the present need of States

- Grants

- Revenue deficit grants: 17 states will receive grants worth Rs 2.9 lakh crore to eliminate the revenue deficit.

- Sector-specific grants: Sector-specific grants of Rs 1.3 lakh crore will be given to states for eight sectors.

- These include (i) health, (ii) school education, (iii) higher education, (iv) implementation of agricultural reforms, (v) maintenance of PMGSY roads, (vi) judiciary, (vii) statistics, and (viii) aspirational districts and blocks.

- A portion of these grants will be performance-linked.

- State-specific grants: The Commission recommended state-specific grants of Rs 49,599 crore.

- These will be given in the areas of (i) social needs, (ii) administrative governance and infrastructure, (iii) water and sanitation, (iv)preservation of cultural and historical monuments, (v) high-cost physical infrastructure, and (vi) tourism.

- The Commission recommended a high-level committee at the state level to review and monitor the utilisation of state-specific and sector-specific grants.

- Grants to local bodies: The total grants to local bodies will be Rs 4.36 lakh crore (a portion of grants to be performance-linked) including (i) Rs 2.4 lakh crore for rural local bodies, (ii) Rs 1.2 lakh crore for urban local bodies, and (iii) Rs 70,051 crore for health grants through local governments.

- The grants to local bodies will be made available to all three tiers of Panchayat- village, block, and district.

- The health grants will be provided for: (i) conversion of rural sub-centres and primary healthcare centres (PHCs) to health and wellness centres (HWCs), (ii) support for diagnostic infrastructure for primary healthcare activities, and (iii) support for urban HWCs, sub-centres, PHCs, and public health units at the block level.

- Grants to local bodies (other than health grants) will be distributed among states based on population and area, with 90% and 10% weightage, respectively.

- The Commission has prescribed certain conditions for availing these grants (except health grants).

- The entry-level criteria include: (i) publishing provisional and audited accounts in the public domain and (ii) fixation of minimum floor rates for property taxes by states and improvement in the collection of property taxes (an additional requirement after 2021-22 for urban bodies).

- Urban local bodies have been categorised into two groups, based on population, and different norms have been used for the flow of grants to each, based on their specific needs and aspirations.

- Basic grants are proposed only for cities/towns having a population of less than a million. For Million-Plus cities, 100 per cent of the grants are performance-linked through the Million-Plus Cities Challenge Fund (MCF).

- No grants will be released to local bodies of a State after March 2024 if the state does not constitute State Finance Commission and act upon its recommendations by then.

- Disaster risk management

- The Commission recommended retaining the existing cost-sharing patterns between the Centre and States for disaster management funds.

- The cost-sharing pattern between centre and states is (i) 90:10 for north-eastern and Himalayan states, and (ii) 75:25 for all other states.

- Mitigation Funds should be set up at both the national and State levels, in line with the provisions of the Disaster Management Act.

- The Mitigation Fund should be used for those local level and community-based interventions which reduce risks and promote environment-friendly settlements and livelihood practices.

- It has recommended the total corpus of Rs.1,60,153 crore for States for disaster management for 2021-26, of which the Union’s share is Rs. 1,22,601 crore and States’ share is Rs. 37,552 crore.

- Fiscal consolidation

- Provided range for fiscal deficit and debt path of both the Union and States.

- The Commission suggested that the Centre bring down fiscal deficit to 4% of GDP by 2025-26.

- For states, it recommended the fiscal deficit limit (as % of GSDP) of: (i) 4% in 2021-22, (ii) 3.5% in 2022-23, and (iii) 3% during 2023-26.

- If a state is unable to fully utilise the sanctioned borrowing limit during the first four years (2021-25), it can avail of the unutilised borrowing amount in subsequent years (within the 2021-26 period).

- Extra annual borrowing worth 0.5% of GSDP will be allowed to states during the first four years (2021-25) upon undertaking power sector reforms.

- Given the uncertainty that prevailed at the stage that the 15th Finance Commission has done its analysis, as well as the contemporary realities and challenges, it recommended restructuring of the FRBM Act of the Centre and the States.

- It recommended forming a high-powered inter-governmental group to (i) review the Fiscal Responsibility and Budget Management Act (FRBM), (ii) recommend a new FRBM framework for the Centre as well as States and oversee its implementation.

- It preferred revenue mobilisation by strengthening income and asset-based taxation.

- Concerning GST, it recommended the restoration of revenue neutrality of GST rates. States need to step up field efforts for expanding the GST base and for ensuring compliance.

- Regarding fiscal management practices, it recommended the development of a comprehensive framework for public financial management.

- An independent Fiscal Council should be established with powers to assess records from the centre as well as states.

- The Council will only have an advisory role.

- Both Centre and States should strive to improve the accuracy and consistency of macroeconomic and fiscal forecasting.

- States should amend their fiscal responsibility legislation to ensure consistency with the centre’s legislation, in particular, with the definition of debt.

- State Governments may explore the formation of independent public debt management cells which will chart their borrowing programme efficiently.

- Health

- States should increase spending on health to more than 8% of their budget by 2022.

- Primary healthcare expenditure should be two-thirds of the total health expenditure by 2022.

- Given the inter-State disparity in the availability of medical doctors, All India Medical and Health Service should be established as is envisaged under Section 2A of the All-India Services Act, 1951.

- Centrally sponsored schemes (CSS) in health should be flexible enough to allow states to adapt and innovate. The focus of CSS in health should be shifted from inputs to outcomes.

- .Defence and Internal Security

- A dedicated non-lapsable fund called the Modernisation Fund for Defence and Internal Security (MFDIS) will be constituted in the Public Account of India to primarily bridge the gap between budgetary requirements and allocation for capital outlay in defence and internal security.

- The fund will have an estimated corpus of Rs 2.4 lakh crore over the five years (2021-26).

- Centrally Sponsored Schemes(CSS)

- A threshold should be fixed for annual allocation to CSS below which the funding for a CSS should be stopped (to phase out CSS which outlived its utility or has insignificant outlay).

- Third-party evaluation of all CSS should be completed within a stipulated timeframe.

- The funding pattern should be fixed upfront in a transparent manner and be kept stable.

Criticism

- Use of Census 2011 data – It has been observed that the sole reliance on the 2011 population figures would discriminate against States such as Kerala that have a better record of controlling population growth and reducing their share in the national population.

- Biased towards Centre

- Boost to fiscal centralisation – It is being criticised for being inclined towards the Centre by implicitly endorsing the central government’s tendency to adopt fiscally adverse, neoliberal policies and make up for the revenue loss by depriving states of revenues as a means to shore up the Centre’s fiscal position.

- Use of tax effort criterion for States – Critics argue that the 15th Finance Commission does not take account of the revenue loss the former’s policies of the central government have resulted in. It has included in its formula for determining the sharing of devolved resources among the States a new tax-effort criterion, captured by the three-year average of per-capita own tax revenues and Per-Capita Gross State Domestic Product (GSDP). While a state’s share is linked to its tax performance, the centre’s tendency to forego tax revenues when spending is at a premium is passed by.

- Not addressing the issue of cesses and surcharges – The 15th Finance Commission has been criticised for not addressing the issue of increasing cesses and surcharges by the central government which are not required to be shared with the States.

- Increasing central interference in terms of transfer of resources to States – The 15th Finance Commission has been further criticised for changing the terms of transfer in ways that erode the policy independence of the state government and increases the room for central interference in the determination of state-level priorities through instruments such as (i) to increase the share of resources transferred to the States and local bodies that are tied to areas, sectors or schemes; and (ii) linking transfers to performance criteria.

- Conditional grants to local bodies – Critics argue that grants based on conditions to be met decreases States’ autonomy. States are required to set up state finance commissions to determine State government grants to report on the implementation of recommendations by March 2024. 60 per cent of grants will be linked to the provision of sanitation and water services. While these are desirable but such provisions infringe upon the right of the States and Local Bodies to determine their priorities.

- States’ demand for larger loans declined and net borrowing fall – The 15th FC has not acceded to the demand of the States that they be permitted to borrow larger sums to meet their immediate fiscal strain, and do so without being subjected to conditions. Furthermore, the base limit for net borrowings of state governments has been reduced for consecutive financial years. The additional borrowing space of 1 per cent offered after the Covid crisis has been reduced to 0.5 per cent of GSDP for States, which too is conditional on the completion of power sector reforms.

- Non-lapsable defence fund – The 15th FC has also accepted the Centre’s suggestion to set up a non-lapsable dedicated fund to support defence and internal security modernisation. While a major part of the fund will be funded from the Consolidated Fund of India, there is an ambiguity over other sources to be tapped. Given the Centre’s claim that the States should share the burden of defence and security, there is a possibility of diverting a part of the States’ share of resources to financing this facility.

Conclusion

The age-old established institution faces varying challenges every time it is constituted. It is often compared to its predecessors and criticised yet it has a crucial role to play in balancing the fiscal federalism in India. A correction of imbalances it creates and a well-organised discussion with all the stakeholders may be the way forward.

Practise question

- Critically analyse the recommendations made by the Fifteenth Finance Commission of India and suggest the way forward.

- https://www.theleaflet.in/15th-finance-commission-recommendations-favour-neo-liberal-fiscal-centralisation-that-may-affect-states/

- https://pib.gov.in/PressReleasePage.aspx?PRID=1693868

- https://prsindia.org/policy/report-summaries/report-15th-finance-commission-2021-26

- https://fincomindia.nic.in/

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

A comprehensive evaluation. 👍