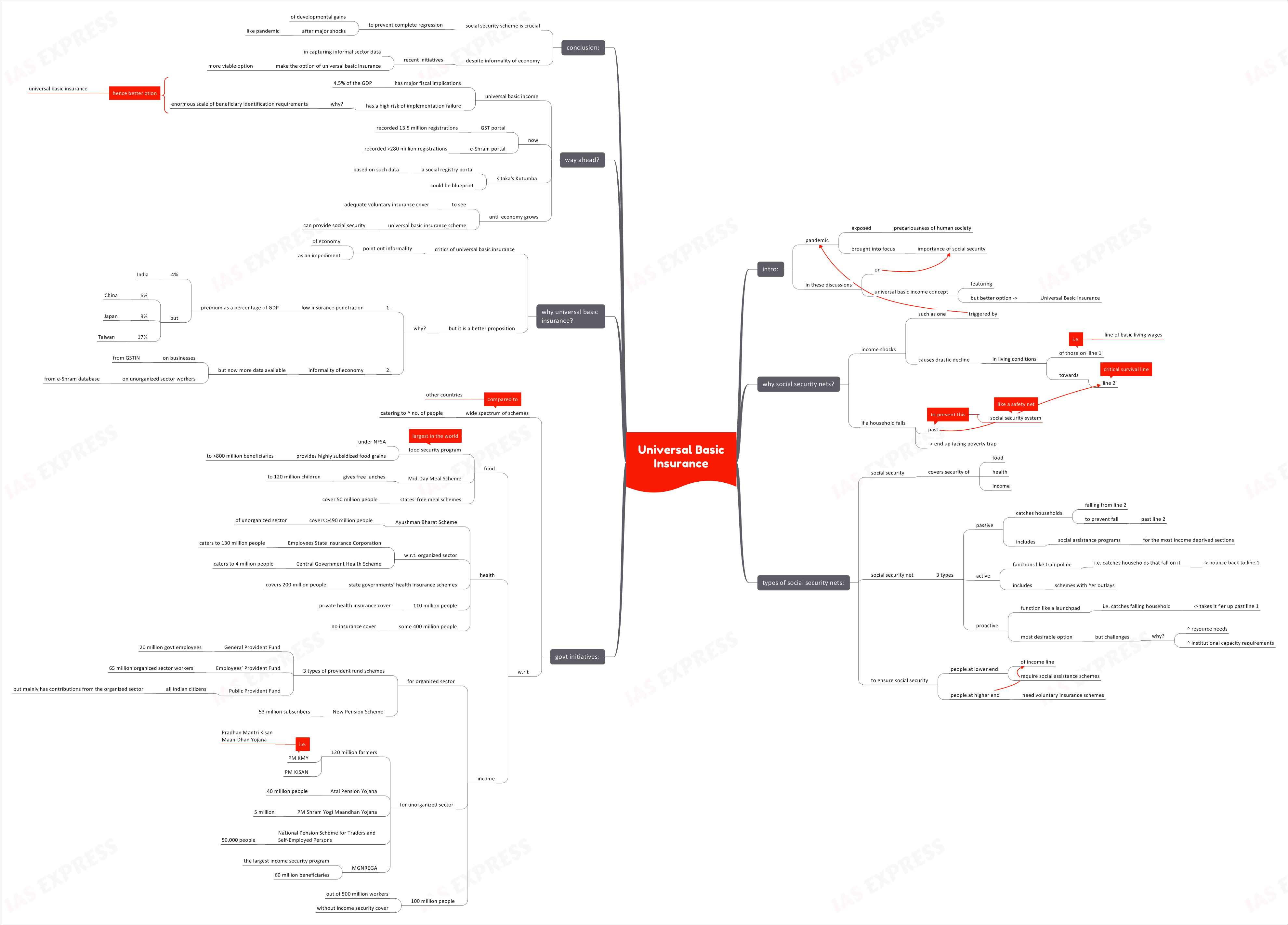

Universal Basic Insurance

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

The precariousness of human society was exposed by the pandemic and the importance of social security came into focus. The concept of Universal Basic Income featured in the discussions on how best to ensure social security for the masses. However, another concept- Universal Basic Insurance- needs to be examined as it may prove to be more suitable in the Indian context.

Why are social security nets needed?

- Income shocks- such as the ones triggered by the pandemic- causes a drastic decline in the conditions of those living on the line of basic living wages (line 1) towards the critical survival line (line 2).

- If a

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses