5.4.2 Private-Public Partnerships (PPP) | Planning and Economic Development

Public-Private Partnerships (PPPs) represent a critical and evolving instrument in the toolkit of modern economic planning and development, particularly for emerging economies like India. These long-term contractual arrangements between a government entity and a private sector firm are designed to deliver public assets and services by leveraging private sector capital, technological innovation, and operational efficiency. As India aims to bridge its substantial infrastructure deficit, estimated to require investments of around ₹111 lakh crore by 2025, PPPs have moved from a peripheral option to a central pillar of its development strategy. This framework facilitates not only the infusion of much-needed private finance but also an optimal allocation of risks and responsibilities, promising enhanced value-for-money for the public exchequer and improved quality of services for citizens, thereby playing a pivotal role in accelerating sustainable and inclusive economic growth.

Defining Public-Private Partnerships

- A Public-Private Partnership (PPP) is fundamentally a long-term, cooperative arrangement between two or more public and private sectors. This collaboration is typically geared towards financing, building, and operating infrastructure projects, such as transportation networks, public utility systems, and social infrastructure like hospitals and schools.

- Core to the PPP concept is the sharing of risk and reward between the public and private partners. The private entity typically invests its own capital and expertise, and in return, receives a stream of payments over the life of the project. These payments can be derived from user fees (e.g., tolls on a highway), payments from the government (e.g., availability payments for a hospital), or a combination of both. As of November 2020, India had initiated 1,103 PPP projects, representing a substantial committed investment of approximately $275 billion, underscoring the model’s significance in the national development agenda.

- The Government of India, in a 2011 notification, defined a PPP as “an arrangement between a statutory/government-owned entity on one side and a private sector entity on the other, for the provision of public assets and/or public services, through investments being made and/or management being undertaken by the private sector entity, for a specified period of time, where there is a well-defined allocation of risk between the private and public entity.”

- This definition highlights several key characteristics:

- Long-Term Nature: PPP contracts are not short-term arrangements; they often span 20 to 30 years, or even longer, to allow the private partner sufficient time to recoup its investment.

- Risk Allocation: A crucial element of a PPP is the allocation of risks to the party best equipped to manage them. For instance, the private sector might bear the construction and operational risks, while the public sector might retain risks related to land acquisition and policy changes.

- Private Sector Investment and Management: The private partner brings not only capital but also managerial and technical expertise, which is expected to lead to greater efficiency and innovation.

- Performance-Based Payments: The private partner’s remuneration is linked to its performance in delivering the specified service or asset, creating a strong incentive for quality and efficiency.

- This definition highlights several key characteristics:

Historical Evolution and Global Context

- The concept of collaboration between public and private entities for infrastructure development is not new. Historically, governments have granted concessions to private companies for building and operating infrastructure like railways and canals since the 18th and 19th centuries.

- The modern wave of PPPs gained momentum in the 1980s and 1990s, particularly in the United Kingdom, as a means of bringing private sector discipline and finance into the delivery of public services. This model, known as the Private Finance Initiative (PFI), was subsequently adopted and adapted by many other countries.

- Globally, PPPs have become a mainstream tool for infrastructure development. Developed countries like Australia and Canada have mature PPP markets and sophisticated frameworks for managing these projects. In the United States, there is a growing interest in using PPPs to address its aging infrastructure. Many continental European countries, including France and Spain, have a long tradition of using concessions for motorway development.

- In developing countries, PPPs are seen as a vital mechanism to bridge the infrastructure financing gap. Organizations like the World Bank and the Asian Development Bank actively promote and support the use of PPPs in these regions. Global trends in 2024 show a stable credit outlook for PPPs, with a particular resilience noted in availability-based models where the government pays for the service, reducing demand risk for the private partner. There is also a growing emphasis on using PPPs to achieve sustainable development goals and address climate change, for example, by financing renewable energy projects and climate-resilient infrastructure.

PPPs in the Indian Context

- India’s journey with PPPs began in earnest in the early 2000s, driven by the need to accelerate infrastructure development to support a rapidly growing economy. The government recognized that public funds alone would be insufficient to meet the country’s vast infrastructure needs.

- A key milestone was the establishment of a formal institutional framework to support PPPs. This included:

- The creation of the PPP Cell in the Department of Economic Affairs, Ministry of Finance, to act as the nodal agency for all PPP-related matters.

- The establishment of the Public Private Partnership Appraisal Committee (PPPAC) in 2006 to streamline the appraisal and approval process for central sector PPP projects. As of early 2023, the PPPAC had appraised 390 projects with a total project cost of over ₹8.1 lakh crore.

- The launch of the Viability Gap Funding (VGF) scheme in 2006 to provide financial support to PPP projects that are economically justified but not financially viable on their own. The scheme provides a capital grant of up to 20% of the project cost, which can be increased under certain conditions.

- The setting up of the India Infrastructure Finance Company Limited (IIFCL) in 2006 to provide long-term debt financing for infrastructure projects.

- The road sector has been the frontrunner in the adoption of PPPs in India, with the National Highways Authority of India (NHAI) implementing a large number of projects under various PPP models. Ports, airports, and urban infrastructure have also seen significant PPP activity.

- The evolution of PPP models in India reflects a learning process. The initial reliance on the Build-Operate-Transfer (BOT) model, where the private partner bore most of the risks, faced challenges, leading to the introduction of more balanced models like the Hybrid Annuity Model (HAM).

Rationale and Objectives of PPPs

- The primary rationale for governments to adopt the PPP model is to achieve “Value for Money” (VfM). This does not simply mean choosing the cheapest option, but rather securing the optimum combination of whole-life costs and quality of service.

- Key objectives of pursuing PPPs include:

- Leveraging Private Sector Finance: PPPs provide an additional source of funding for infrastructure development, reducing the immediate burden on the public exchequer. This is particularly important for developing countries with fiscal constraints. The National Infrastructure Pipeline (NIP) of India estimates an investment requirement of ₹111 lakh crore by 2025, a significant portion of which is expected to come from the private sector.

- Enhancing Efficiency and Innovation: The private sector is often perceived as being more efficient in project management, construction, and operations. Competition in the bidding process and the profit motive are expected to drive innovation and cost-effectiveness.

- Optimal Risk Allocation: A well-structured PPP allocates risks to the party best able to manage them. Transferring construction and operational risks to the private sector can incentivize on-time, on-budget project delivery and efficient long-term maintenance.

- Improving Service Quality: By linking payments to performance standards, PPPs can ensure a higher quality and more reliable delivery of public services.

- Accelerating Infrastructure Delivery: By bringing in private sector capacity and finance, PPPs can help to deliver a larger number of infrastructure projects more quickly than would be possible through traditional public procurement alone.

Core Families of PPP Models

- Public-Private Partnership models are not monolithic; they exist on a spectrum, defined by the degree of private sector involvement, risk transfer, and responsibility. The World Bank categorizes these into several “families,” each representing a different level of private participation. Understanding these distinctions is crucial for policymakers and economists to select the most appropriate structure for a given project.

- Management and Lease Contracts:

- These models represent the lower end of the private participation spectrum.

- Management Contract: Here, the government retains ownership of the asset and responsibility for capital investment. A private firm is contracted for a specific period (typically 3-5 years) to manage the operations and maintenance of a public utility or facility. The private operator is paid a fee for its services. This model is useful for improving operational efficiency without significant private capital investment. For example, a municipality could contract a private firm to manage its solid waste collection services.

- Lease Contract (Lease-Develop-Operate): In this model, the private sector leases an asset from the public sector and takes on the responsibility for operating and maintaining it. The private lessee is responsible for commercial risk and is entitled to the revenue generated by the asset. This model transfers more risk to the private sector than a management contract but still keeps the asset under public ownership.

- Concessions:

- Concessions are a more integrated form of PPP where a private partner (the concessionaire) takes on responsibility for the full lifecycle of an infrastructure project, including financing, design, construction, operation, and maintenance.

- The concessionaire operates the facility for a specified long period (e.g., 25-30 years) and recovers its investment through user charges (e.g., tolls, tariffs) or government payments.

- At the end of the concession period, the asset is typically transferred back to the public sector. Concessions involve a very high degree of risk transfer to the private sector.

- Build-Operate-Transfer (BOT) and its Variants:

- This is the most widely recognized family of PPP models, especially for greenfield infrastructure projects (new projects).

- The private sector is responsible for designing, building, financing, and operating the facility.

- The key variants are distinguished by the specifics of ownership and transfer:

- Build-Operate-Transfer (BOT): The private partner builds and operates the facility for the concession period, after which ownership and operational responsibility are transferred to the public authority. This has been the most common model for highway projects in India.

- Build-Own-Operate-Transfer (BOOT): This is similar to BOT, but the private partner formally owns the asset during the concession period. This can have implications for taxation and financing. Greenfield minor port concessions in Gujarat have often been on a BOOT basis.

- Build-Transfer-Operate (BTO): In this model, the private partner builds the facility and then immediately transfers ownership to the public sector. The private partner then operates the facility for a specified period under a lease or management agreement. This reduces the private partner’s risk associated with long-term asset ownership.

- Build-Own-Operate (BOO): Under this model, the private partner builds, owns, and operates the facility in perpetuity. The government acts as a regulator and/or a purchaser of the services provided. This model is more akin to privatization and is less common for core public infrastructure in India but can be seen in sectors like power generation.

- Design-Build-Finance-Operate (DBFO):

- This is a comprehensive model where all responsibilities—design, build, finance, and operate—are bundled into a single contract and transferred to the private partner.

- The DBFO model is designed to maximize private sector innovation and efficiency across the entire project lifecycle. The private partner is incentivized to design and build a high-quality, durable asset to minimize its long-term operational and maintenance costs.

- Management and Lease Contracts:

Specific PPP Models in the Indian Context

- India has experimented with and adapted various PPP models to suit its specific needs, particularly in the infrastructure sector. The evolution from toll-based BOT models to the Hybrid Annuity Model (HAM) for highways is a prime example of this policy innovation.

- Engineering, Procurement, and Construction (EPC) Model:

- While not a true PPP in the sense of long-term risk sharing, the EPC model is often discussed in the same context.

- Under this model, the government bears the full financial cost of the project. A private contractor is engaged to execute the project, covering engineering, procurement, and construction, for a fixed lump-sum price.

- The private contractor’s responsibilities typically end after the construction phase, and they do not take on operational or revenue risk. This model is preferred for projects where the government wants to retain control over operations and revenue.

- BOT (Toll) Model:

- This has been the traditional PPP model for Indian highways.

- The private concessionaire finances and builds the road, and recovers its investment and a return by collecting tolls from users for a specified concession period (e.g., 20 years).

- The concessionaire bears the construction risk, operational risk, and, crucially, the traffic (revenue) risk. If traffic volumes are lower than projected, the concessionaire’s revenue will suffer. Many BOT (Toll) projects in the past decade faced financial distress due to overly optimistic traffic projections.

- BOT (Annuity) Model:

- This model was introduced to mitigate the traffic risk for the private developer.

- The concessionaire finances and builds the road, but instead of collecting tolls, it receives fixed, semi-annual payments (annuities) from the government (NHAI) over the concession period.

- While the developer is shielded from traffic risk, the government bears this risk. The payments from the government are contingent on the developer maintaining the road to pre-specified standards.

- Hybrid Annuity Model (HAM):

- Introduced in 2016, HAM is a mix of the EPC and BOT (Annuity) models, designed to revive private investment in the road sector.

- Under HAM, the government pays 40% of the project cost to the developer during the construction phase, in five equal installments. This reduces the upfront financial burden on the private partner.

- The remaining 60% of the project cost is paid as annuity payments over the operational period, along with interest and operation and maintenance (O&M) costs.

- In this model, the government bears the traffic risk (as it collects the toll), and the financial risk is shared between the government and the private developer. The developer is still responsible for construction and maintenance risks. The NHAI plans to award projects worth ₹2.44 lakh crore under HAM in the current fiscal year.

- Engineering, Procurement, and Construction (EPC) Model:

Financial and Contractual Structure: The Special Purpose Vehicle (SPV)

- A central feature of the financial and legal architecture of most large-scale PPPs is the creation of a Special Purpose Vehicle (SPV).

- What is an SPV?: An SPV, also known as a project company, is a distinct legal entity created specifically for the purpose of executing a single PPP project. It is formed by the consortium of private companies (sponsors) that wins the PPP bid.

- Legal Structure: The SPV is the entity that signs the concession agreement with the government authority. It also enters into all other project-related contracts, such as construction contracts with contractors, loan agreements with lenders, and O&M agreements with operators.

- Financial Structure:

- The SPV raises finance for the project. This is typically done through a combination of equity and debt.

- Equity: This is the capital invested by the sponsors of the project (the shareholders of the SPV). Equity holders are the ultimate risk-takers and are remunerated through dividends from the project’s profits.

- Debt: This constitutes the majority of the project’s funding, often in a ratio of 70:30 or 80:20 (debt to equity). The debt is raised from banks and financial institutions.

- Project Finance: PPPs typically use “project finance,” which can be either “non-recourse” or “limited-recourse.” This means that the lenders’ claim for repayment is limited to the project’s assets and cash flows, and they have little or no recourse to the sponsors’ other assets. This “ring-fencing” of the project is a key advantage of the SPV structure, as it isolates the project’s risks from the sponsors’ parent companies.

The Indian Highway Sector: A Laboratory for PPP Models

- The development of National Highways in India has been a flagship area for the application of PPPs, showcasing a dynamic evolution of models in response to changing economic conditions and risk perceptions.

- The Early Push with BOT (Toll):

- The National Highways Development Project (NHDP), launched in the early 2000s, heavily relied on the BOT (Toll) model. This was driven by the government’s objective to leverage private capital and transfer a significant portion of the risk to the private sector.

- Under this model, private developers were responsible for financing, constructing, and operating highways, recovering their costs through the right to collect tolls for a concession period of 20-30 years.

- Challenges Encountered: By the early 2010s, the BOT (Toll) model ran into significant headwinds.

- Aggressive Bidding: Intense competition led to private players making overly optimistic traffic projections to win bids, which often did not materialize.

- Land Acquisition Delays: The government’s inability to provide encumbrance-free land on time led to major construction delays and cost overruns, severely impacting project viability.

- Financing Issues: Following the 2008 global financial crisis, lenders became more risk-averse, and many developers struggled to achieve financial closure for their projects. By 2014, the BOT model had effectively collapsed, with very few new projects being awarded under this route.

- The Rise of the Hybrid Annuity Model (HAM):

- To revive private sector participation, the government introduced the Hybrid Annuity Model (HAM) in 2016. HAM represents a strategic shift in risk allocation.

- Key Features of HAM:

- Shared Financial Risk: The National Highways Authority of India (NHAI) provides 40% of the project cost as a grant during the construction period. This significantly reduces the equity contribution and debt requirement for the private developer.

- Government Assumes Revenue Risk: The NHAI is responsible for toll collection, thereby shielding the developer from traffic and revenue risks.

- Performance-Based Annuity Payments: The developer receives the remaining 60% of the project cost in the form of bi-annual annuity payments over a 15-year operational period. These payments are linked to the developer’s performance in maintaining the highway.

- Impact: HAM proved to be highly successful in attracting private players back into the highway sector. It balanced the risk profile, making projects more bankable. In the fiscal year 2024, the NHAI is expected to continue its focus on HAM, with projects worth ₹2.44 lakh crore planned under this model, compared to only 12 projects worth ₹62,125 crore under the traditional BOT (Toll) model.

- Revamping the BOT Model:

- Despite the success of HAM, the government is now attempting to revive the pure BOT (Toll) model. This is driven by the need to tap into a wider pool of private capital and reduce the fiscal burden on the NHAI.

- The revamped BOT model includes more equitable risk-sharing provisions and a more transparent process for assessing project viability, aiming to attract over ₹1 trillion in private capex by 2030.

- The Early Push with BOT (Toll):

Transforming India’s Ports through PPPs

- The port sector in India has been a remarkable success story for PPPs, leading to significant capacity augmentation, efficiency improvements, and modernization.

- The Landlord Port Model:

- The dominant PPP model in Indian ports is the “Landlord Port” model. In this model, the port authority (which is publicly owned) acts as a regulatory body and a landlord, while private companies carry out port operations, primarily cargo handling.

- The port authority retains ownership of the land and basic infrastructure, which it leases to the private operators. The private operators invest in and operate the cargo handling equipment and terminal infrastructure.

- Jawaharlal Nehru Port (JNP): A PPP Pioneer:

- JNP, located near Mumbai, is India’s largest container port and a prime example of successful PPP implementation. It became the first 100% Landlord Major Port in India, with all its berths operated under the PPP model.

- The first PPP agreement in the Indian port sector was signed in 1997 at JNP. This 25-year-long partnership has been instrumental in driving efficiency and capacity growth.

- A recent PPP project at JNP involves the private operator investing ₹872 crore to upgrade the Jawaharlal Nehru Port Container Terminal (JNPCT), which is expected to increase its handling capacity from 1.5 million to 1.8 million TEUs (Twenty-foot Equivalent Units).

- Impact and Future Outlook:

- Over the past 25 years, PPPs have facilitated investments of around ₹55,000 crore in the Indian port sector.

- A substantial portion of the cargo at major ports is now handled by private operators through PPPs, a share that is projected to increase to 85% by the end of the decade.

- The Ministry of Ports, Shipping and Waterways (MOPSW) is actively promoting further PPPs. Under the Sagarmala Programme, numerous PPP projects are underway, and the ministry aims to initiate additional projects worth ₹42,300 crore by the end of fiscal year 2025.

- A recent development is the approval for setting up a new major port at Vadhavan in Maharashtra at a cost of ₹76,220 crore, a significant portion of which will be on PPP mode.

- The Landlord Port Model:

Challenges and Opportunities in Urban Infrastructure PPPs

- While PPPs have made significant inroads in national-level infrastructure like highways and ports, their adoption in urban infrastructure has been more challenging and less widespread.

- The Need for Urban PPPs:

- India is rapidly urbanizing, putting immense pressure on urban infrastructure and services like water supply, sewerage, solid waste management, and urban transport.

- Urban Local Bodies (ULBs) often lack the financial resources and technical capacity to meet this growing demand, making PPPs a potentially attractive solution.

- Challenges Faced by Urban PPPs:

- Weak Financial Health of ULBs: Many municipalities in India have a weak revenue base and poor creditworthiness, making them less attractive partners for the private sector. Private investors are often concerned about the ULB’s ability to make timely payments.

- Political and Social Risks: Urban projects, especially those involving user charges for services like water, can be politically sensitive. There is often public resistance to the “privatization” of essential services.

- Lack of Capacity: ULBs often lack the technical and managerial expertise to structure, procure, and manage complex PPP contracts.

- Data from The India Infrastructure Report 2023 reveals that only 10% of all PPP projects in the country are in urban areas, and these are concentrated in a few states like Gujarat, Uttar Pradesh, and Maharashtra.

- Successful Examples and Innovative Models:

- Despite the challenges, there are successful examples of urban PPPs.

- Tirupur Water Supply and Sewerage Project, Tamil Nadu: This was one of the first water and sanitation projects in India developed under a PPP framework. It involved creating a new water source and distribution system for the industrial town of Tirupur.

- Nagpur Water Supply Project: This project involves a 25-year concession for the rehabilitation and operation of the water supply system for the entire city.

- New Delhi Municipal Corporation (NDMC) Public Toilet Utilities (PTUs): NDMC has used a PPP model where it provides space for constructing PTUs, and the private partner builds and maintains them, generating revenue from advertising space provided alongside the toilets.

- Eco-restoration of Villivakkam Tank, Chennai: This is another example of an innovative urban PPP project.

- The Need for Urban PPPs:

Healthcare PPPs: Bridging the Accessibility and Quality Gap

- Public-Private Partnerships in the healthcare sector in India are increasingly being explored as a strategy to supplement public healthcare systems, improve service quality, and expand access, particularly in underserved areas.

- Rationale for Healthcare PPPs:

- India faces a significant deficit in healthcare infrastructure and personnel. The private sector accounts for a large portion of healthcare delivery, but it is often expensive and concentrated in urban areas.

- PPPs aim to leverage the private sector’s efficiency, technology, and management expertise to enhance public healthcare services. They can help in areas like hospital management, diagnostic services, and primary healthcare delivery.

- Models of Healthcare PPPs:

- Management of Primary Health Centers (PHCs): State governments have entered into PPPs where private entities or NGOs are contracted to manage and operate PHCs in rural and remote areas. The private partner is responsible for ensuring the availability of doctors, staff, medicines, and services, and is paid by the government based on performance.

- Diagnostic Services: PPPs are widely used for providing high-tech diagnostic services like MRI and CT scans in public hospitals. The private partner installs and operates the equipment within the public hospital premises, and services are provided at government-prescribed rates.

- Hospital Management (The Manipal Model): A prominent and long-standing example is the partnership between the Government of Karnataka and the Manipal Foundation. Under this arrangement, Manipal manages government hospitals, upgrading them into teaching hospitals for its medical college. This provides quality tertiary care to the public at affordable rates while providing clinical training facilities for the college.

- Health Insurance Schemes (Rashtriya Swasthya Bima Yojana – RSBY): The RSBY, a national health insurance scheme for below-poverty-line families, was implemented through a PPP model involving private insurance companies. The insurance companies were responsible for empaneling hospitals, enrolling beneficiaries, and settling claims.

- Challenges and Criticisms:

- Equity Concerns: A major criticism is that PPPs may lead to a two-tiered system, where the quality of care depends on the ability to pay. There are concerns that the profit motive could lead to a focus on more lucrative procedures, neglecting basic healthcare.

- Regulatory Oversight: Effective regulation and monitoring are crucial to ensure that private partners adhere to quality standards and do not overcharge patients. This has been a significant challenge.

- Performance Measurement: There is a lack of robust evidence and high-quality research on the long-term impact of healthcare PPPs on health outcomes in India. Most assessments are based on a limited number of case studies.

- Rationale for Healthcare PPPs:

PPPs in the Indian Education System

- The Indian education system, both at the school and higher education levels, faces challenges of access, equity, and quality. PPPs are being promoted as a means to address these challenges, although their adoption has been slower and more controversial than in the infrastructure sectors.

- Rationale for Education PPPs:

- Public spending on education in India has remained below the recommended 6% of GDP. PPPs can help bridge the funding gap for building and maintaining educational infrastructure.

- The private sector can bring in innovation in curriculum development, teaching methodologies, and the use of technology in education.

- Prominent Forms of Education PPPs:

- Infrastructure-led Partnerships: The private sector is involved in building and maintaining school infrastructure (e.g., classrooms, labs, toilets), while the government is responsible for the academic aspects.

- Management Partnerships (School Vouchers/Adoption): In some models, the government provides funding (e.g., through vouchers) to students to attend private schools. In others, private entities “adopt” government schools to improve their management and academic performance.

- Curriculum and Teacher Training Partnerships: Private organizations with expertise in specific areas are roped in to provide teacher training, develop new curricula, and introduce digital learning tools in government schools. For instance, the implementation of PPPs varies based on parameters such as ownership of institutes, infrastructure, teacher types, and the extent of financial aid.

- Challenges and Debate:

- Commercialization of Education: A major concern is that PPPs could lead to the commercialization of education, making it unaffordable for the poor.

- Equity and Social Justice: There are fears that PPPs could exacerbate existing inequalities, with better-resourced private schools benefiting more than underprivileged government schools.

- Regulation and Accountability: Ensuring that private partners are accountable for learning outcomes and adhere to social objectives is a significant regulatory challenge. The Indian Ministry of Human Resource Development (now Ministry of Education) has proposed PPP models to improve access to quality school education while ensuring equity, but implementation has been patchy.

- Rationale for Education PPPs:

PPPs in Other Social Sectors

- Beyond healthcare and education, PPPs are also being employed in other critical social sectors to enhance service delivery and create new opportunities.

- Skill Development (Skill India Mission):

- The Skill India Mission, a flagship initiative of the Government of India, heavily relies on a PPP framework.

- The National Skill Development Corporation (NSDC) is a key institution in this domain. It is a not-for-profit public limited company set up as a PPP. The government holds a 49% stake, while the private sector holds 51%.

- The NSDC’s mandate is to catalyze the skilling landscape in India. It does this by funding training providers and creating a robust ecosystem for skill development in partnership with industry. This collaboration aims to ensure that the training provided is aligned with industry requirements, thereby improving employability.

- Sanitation (Swachh Bharat Mission):

- While the Swachh Bharat Mission (Clean India Mission) is primarily a government-led and community-driven movement, it has created opportunities for private sector participation and PPPs.

- Private companies have been involved through their Corporate Social Responsibility (CSR) initiatives, funding the construction of toilets.

- There are also emerging PPP models in urban sanitation, particularly in fecal sludge and septage management, where private operators are contracted to manage and operate treatment plants. The New Delhi Municipal Council’s project for solid waste collection and transportation serves as a case study where the right of citizens to a clean environment was upheld through a PPP initiative.

- Affordable Housing:

- Addressing the urban housing shortage is a major policy priority in India. The government has explored various PPP models to encourage private developers to build affordable housing.

- Cross-subsidy Models: A common PPP model in this sector is cross-subsidization. The government provides land or additional development rights (higher Floor Space Index – FSI) to a private developer for a commercial or high-end residential project, in exchange for the developer building a certain number of affordable housing units. A key challenge in this area is that only about 10% of PPP projects in India are in urban areas, which can be attributed to poor planning and low tax collections by urban local bodies.

- Skill Development (Skill India Mission):

Sourcing Finance: The Debt-Equity Mix

- The financing of a PPP project is a complex process that involves structuring a careful balance between debt and equity to ensure the project is bankable and sustainable over the long term. The financial structure is housed within the Special Purpose Vehicle (SPV) created for the project.

- Equity Financing:

- Equity represents the ownership capital invested by the project sponsors (the private consortium members).

- Equity holders bear the highest risk in the project. If the project fails, they are the last to be repaid, after all lenders and other creditors.

- Because they bear the highest risk, equity investors expect the highest returns, typically in the form of dividends from the project’s profits.

- The equity component of a project is usually smaller than the debt component, but it is crucial as it demonstrates the sponsors’ commitment and provides a financial cushion to absorb initial losses.

- Debt Financing:

- Debt is the borrowed capital that makes up the bulk of a project’s financing, often constituting 60% to 85% of the total project cost.

- Sources of Debt: Debt can be sourced from various places, including commercial banks, international financial institutions (like the World Bank or Asian Development Bank), and the capital markets (through the issuance of project bonds).

- Types of Debt:

- Senior Debt: This is the primary source of debt financing. Senior lenders have the first claim on the project’s cash flows and assets in case of default.

- Subordinated Debt (or Mezzanine Debt): This is a riskier form of debt that ranks below senior debt but above equity. It carries a higher interest rate than senior debt to compensate for the additional risk.

- Non-Recourse vs. Limited-Recourse Financing:

- In non-recourse project finance, the lenders can only be repaid from the project company’s revenues and have no claim on the assets of the project sponsors.

- In limited-recourse financing, the sponsors may provide some guarantees or undertakings to the lenders for specific risks or for a certain period (e.g., during the construction phase). This is the more common structure.

- The Debt-to-Equity Ratio:

- The ratio of debt to equity is a key determinant of the project’s financial structure. A higher debt-to-equity ratio (high leverage) can increase the potential returns for equity investors but also increases the project’s financial risk, as the debt service obligations are higher. The appropriate ratio depends on the project’s risk profile and the stability of its expected cash flows. For instance, a project with stable, predictable revenues (like an annuity-based road project) can support a higher level of debt than a project with volatile revenues (like a toll-based road project).

- Equity Financing:

The Role of Government Support and Viability Gap Funding (VGF)

- Many infrastructure projects, particularly in developing countries or in social sectors, are economically justified (i.e., they generate significant benefits for society) but are not financially viable on their own (i.e., their revenues are not sufficient to cover their costs and provide an adequate return to private investors). In such cases, government support is crucial to make the project attractive for private participation.

- Viability Gap Funding (VGF):

- VGF is a form of government financial support provided as a one-time capital grant to a PPP project to bridge the “viability gap.”

- The Indian VGF Scheme: India has a well-established VGF scheme, administered by the Ministry of Finance.

- The scheme provides a capital subsidy to infrastructure projects that are selected through a competitive bidding process.

- The total VGF from the central government is capped at 20% of the Total Project Cost (TPC). The sponsoring government authority (e.g., a state government) can provide an additional 20% of the TPC.

- In 2020, the scheme was revamped to enhance support for social sectors. For social infrastructure projects like water supply and health, the total VGF can be up to 60% of TPC (30% each from the central and state governments). For pilot or demonstration projects in these sectors, it can be up to 80% of TPC.

- How VGF Works: The private developer who bids for the project with the lowest VGF requirement is typically awarded the contract. This ensures that the government’s financial support is minimized.

- Other Forms of Government Support:

- Annuity Payments/Availability Payments: As seen in the BOT (Annuity) and HAM models, the government can provide a steady stream of revenue to the project company, insulating it from demand risk.

- Guarantees: The government can provide guarantees to lenders against specific risks, such as political risk or the risk of default by the public authority on its payment obligations. This reduces the risk for lenders and can lower the cost of debt.

- Credit Enhancement: The government can help enhance the credit rating of project bonds, making them more attractive to institutional investors like pension funds and insurance companies. For example, India’s National Bank for Financing Infrastructure and Development (NaBFID), established in 2021, is working on designing credit enhancement instruments to de-risk infrastructure projects.

- In-kind Support: The government can provide support in non-financial forms, such as providing land for the project free of cost or with a long-term lease.

- Viability Gap Funding (VGF):

Financial Appraisal of PPP Projects

- Before a PPP project is approved, it must undergo a rigorous financial appraisal to assess its viability and bankability. This involves analyzing the project’s expected cash flows and calculating key financial metrics.

- Financial Modeling: A detailed financial model is created for the project, projecting its revenues, capital costs, and operational costs over the entire concession period. This model is the foundation for all financial analysis.

- Key Financial Metrics:

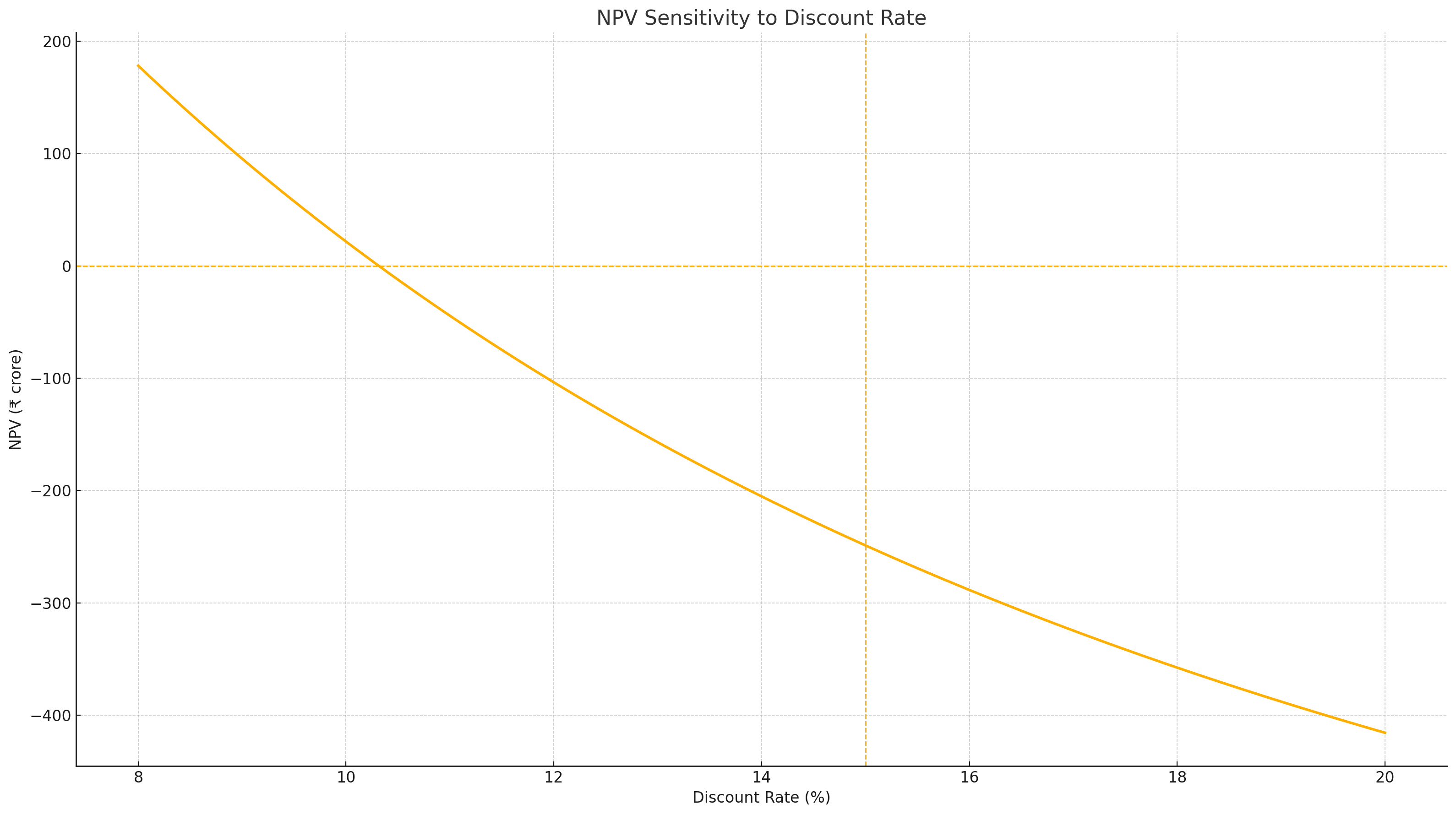

- Net Present Value (NPV):

- NPV is the difference between the present value of a project’s future cash inflows and the present value of its cash outflows. A positive NPV indicates that the project is expected to generate value and is financially acceptable.

- The formula for NPV is: [latex]NPV = \sum_{t=1}^{n} \frac{CF_t}{(1+r)^t} – C_0[/latex], where [latex]CF_t[/latex] is the cash flow in year [latex]t[/latex], [latex]r[/latex] is the discount rate, [latex]n[/latex] is the life of the project, and [latex]C_0[/latex] is the initial investment.

- The discount rate used is typically the project’s Weighted Average Cost of Capital (WACC), which reflects the cost of its debt and equity financing.

- Internal Rate of Return (IRR):

- IRR is the discount rate at which the NPV of a project becomes zero. It represents the project’s expected rate of return.

- A project is considered financially viable if its IRR is greater than the cost of capital (WACC). The main advantage of using IRR is that it considers the time value of money.

- Debt Service Coverage Ratio (DSCR):

- DSCR measures the project’s ability to service its debt. It is calculated as the ratio of cash flow available for debt service to the total debt service obligation (principal + interest).

- Lenders typically require a minimum DSCR (e.g., 1.2x or 1.3x) to be maintained throughout the loan period, ensuring a sufficient cash cushion.

- Net Present Value (NPV):

Numerical Problem: VGF Calculation for a Highway Project

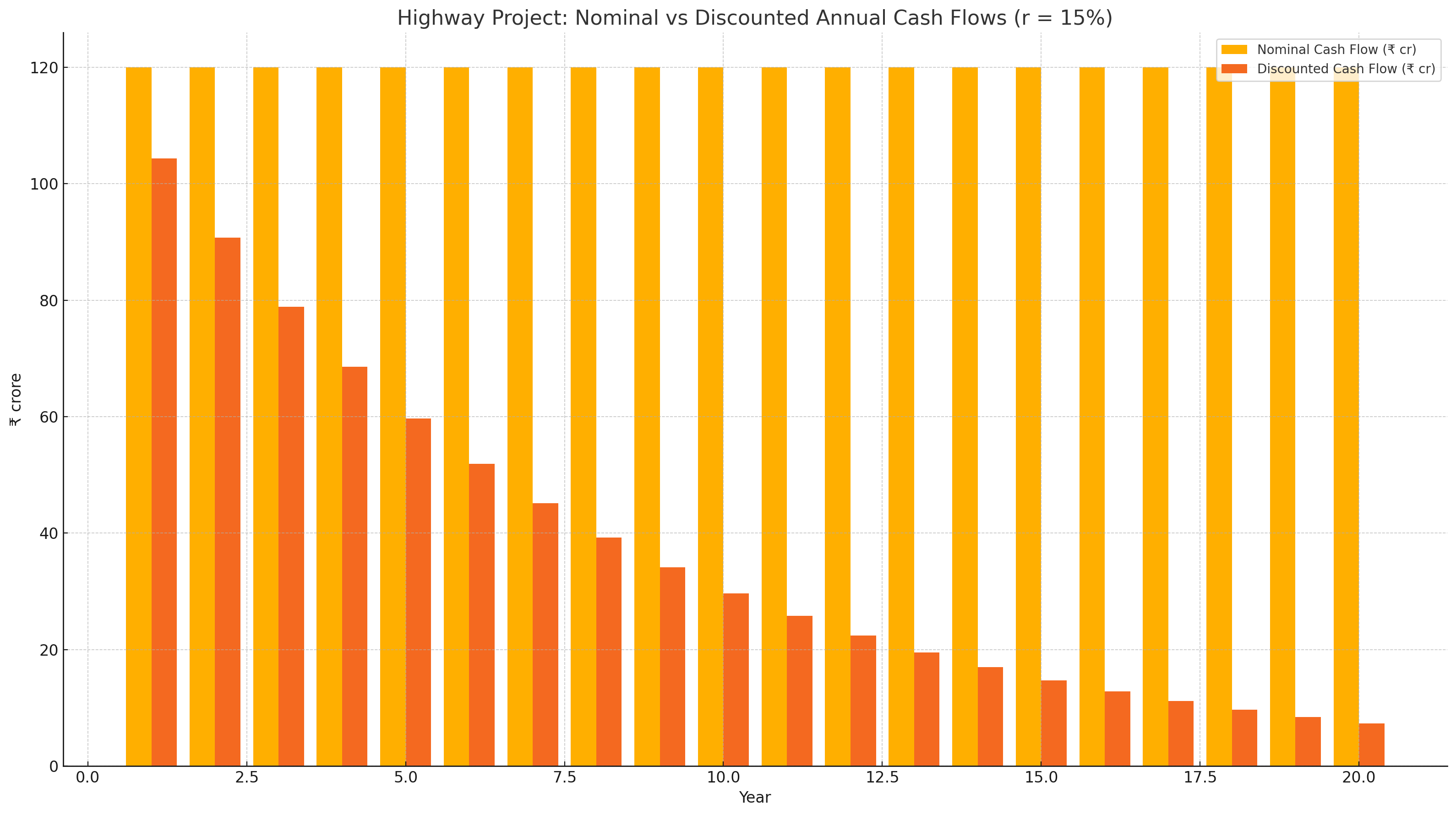

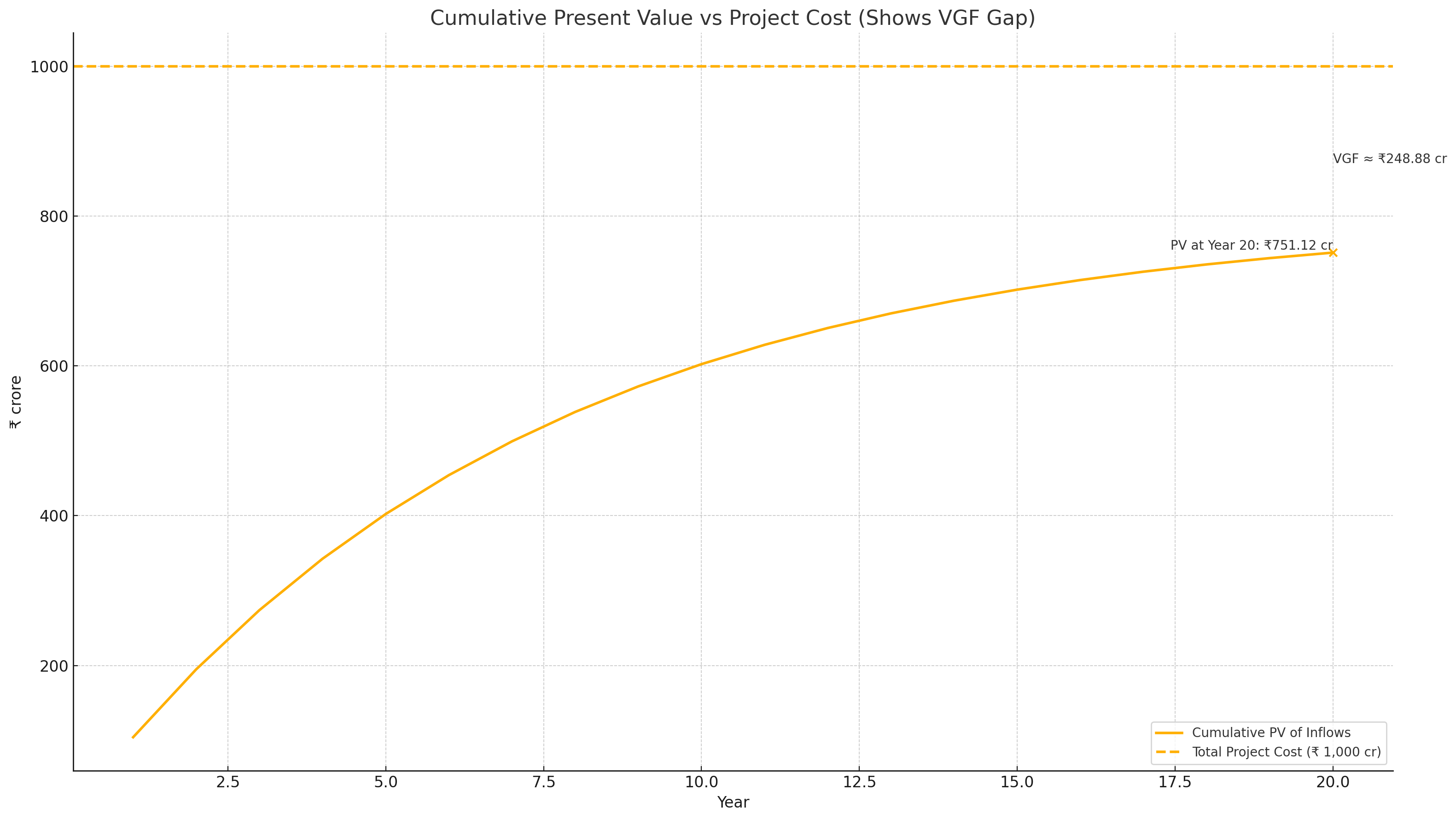

- Problem Statement: A private developer is bidding for a 4-lane highway project under a BOT (Toll) model. The Total Project Cost ([latex]C_0[/latex]) is ₹1,000 crore. The concession period is 20 years. The developer’s required rate of return (discount rate, [latex]r[/latex]) is 15%. The projected net annual cash flow from tolls ([latex]CF_t[/latex]) is ₹120 crore per year for the 20-year period. Determine if the project is financially viable. If not, calculate the Viability Gap Funding (VGF) required to make the project viable for the developer.

- Solution:

- Calculate the Present Value (PV) of future cash inflows: The cash flow is an annuity of ₹120 crore for 20 years. The formula for the present value of an annuity is: [latex]PV = CF_t \times \left[ \frac{1 – (1+r)^{-n}}{r} \right][/latex] [latex]PV = 120 \times \left[ \frac{1 – (1+0.15)^{-20}}{0.15} \right][/latex] [latex]PV = 120 \times \left[ \frac{1 – (1.15)^{-20}}{0.15} \right][/latex] [latex]PV = 120 \times \left[ \frac{1 – 0.0611}{0.15} \right][/latex] [latex]PV = 120 \times \left[ \frac{0.9389}{0.15} \right][/latex] [latex]PV = 120 \times 6.2593[/latex] [latex]PV = ₹751.12 \text{ crore}[/latex]

- Calculate the Net Present Value (NPV) of the project without VGF: [latex]NPV = PV – C_0[/latex] [latex]NPV = 751.12 – 1000[/latex] [latex]NPV = -₹248.88 \text{ crore}[/latex]

- Assess Viability: Since the NPV is negative, the project is not financially viable on its own. The present value of its expected earnings (₹751.12 crore) is less than the initial investment required (₹1,000 crore).

- Calculate the Viability Gap: The viability gap is the shortfall in the present value of earnings compared to the initial cost. This is the amount of funding needed at the beginning of the project to make the NPV equal to zero. Viability Gap = [latex]C_0 – PV[/latex] = ₹1,000 crore – ₹751.12 crore = ₹248.88 crore.

- Conclusion: The developer would need a Viability Gap Funding (VGF) of ₹248.88 crore from the government to make the project financially viable, i.e., to achieve their required 15% rate of return. This VGF amount is approximately 24.89% of the Total Project Cost, which falls within the typical VGF guidelines in India.

| Year | Annual Cash Flow (₹ cr) | Discount Factor | Discounted CF (₹ cr) | Cumulative PV (₹ cr) |

|---|---|---|---|---|

| 1 | 120.00 | 0.8696 | 104.35 | 104.35 |

| 2 | 120.00 | 0.7561 | 90.73 | 195.08 |

| 3 | 120.00 | 0.6575 | 78.90 | 273.98 |

| 4 | 120.00 | 0.5717 | 68.60 | 342.58 |

| 5 | 120.00 | 0.4971 | 59.65 | 402.23 |

| 6 | 120.00 | 0.4322 | 51.86 | 454.09 |

| 7 | 120.00 | 0.3758 | 45.09 | 499.18 |

| 8 | 120.00 | 0.3268 | 39.22 | 538.40 |

| 9 | 120.00 | 0.2842 | 34.10 | 572.50 |

| 10 | 120.00 | 0.2471 | 29.65 | 602.15 |

| 11 | 120.00 | 0.2140 | 25.68 | 627.83 |

| 12 | 120.00 | 0.1861 | 22.33 | 650.16 |

| 13 | 120.00 | 0.1618 | 19.42 | 669.58 |

| 14 | 120.00 | 0.1407 | 16.88 | 686.46 |

| 15 | 120.00 | 0.1224 | 14.69 | 701.15 |

| 16 | 120.00 | 0.1064 | 12.77 | 713.92 |

| 17 | 120.00 | 0.0925 | 11.10 | 725.02 |

| 18 | 120.00 | 0.0804 | 9.65 | 734.67 |

| 19 | 120.00 | 0.0699 | 8.39 | 743.06 |

| 20 | 120.00 | 0.0609 | 7.31 | 750.37 |

The Absence of a Single PPP Law

- Unlike some countries that have a single, overarching law governing Public-Private Partnerships, India has adopted a more flexible and decentralized approach. There is no central PPP Act. Instead, the legal and regulatory framework for PPPs in India is a composite structure built upon several pillars.

- Constitutional and Existing Legal Provisions:

- PPP projects operate within the existing legal system of the country. This includes the Indian Contract Act, 1872, which governs the contractual relationship between the public and private parties; the Transfer of Property Act, 1882; company law; and various tax laws.

- Sector-specific legislation, such as the National Highways Act, 1956, and the Major Port Trusts Act, 1963 (now the Major Port Authorities Act, 2021), also provide the legal basis for PPPs in their respective sectors.

- Policies and Guidelines:

- The Government of India has issued a comprehensive National Public Private Partnership Policy, which serves as a guiding document outlining the principles, objectives, and framework for implementing PPPs.

- The Department of Economic Affairs, Ministry of Finance, periodically issues guidelines on various aspects of PPPs, including project appraisal, procurement, and contract management.

- Standardized Contracts:

- A key element of India’s PPP framework is the development of Model Concession Agreements (MCAs) for different sectors. These are standardized, pre-approved legal documents that form the basis of the PPP contract.

- Constitutional and Existing Legal Provisions:

Key Institutions and Governance Structure

- A robust institutional framework has been established at the central level to manage and guide the PPP program in India, ensuring a streamlined and transparent process for project approval and oversight.

- Department of Economic Affairs (DEA), Ministry of Finance:

- The DEA is the nodal department for PPPs at the central government level.

- The PPP Cell: Housed within the DEA, the PPP Cell is responsible for all policy-level matters concerning PPPs. Its functions include formulating policies, schemes, and programs; developing Model Concession Agreements; and promoting capacity building initiatives for government officials involved in PPPs.

- Public Private Partnership Appraisal Committee (PPPAC):

- Established in 2006, the PPPAC is the apex body for the appraisal and approval of central sector PPP projects.

- Composition: The PPPAC is chaired by the Secretary of the Department of Economic Affairs. Its members include the secretaries of the Department of Expenditure, the Department of Legal Affairs, NITI Aayog (formerly the Planning Commission), and the sponsoring administrative ministry of the project.

- Mandate: The PPPAC’s role is to ensure that PPP projects are well-structured, financially viable, and provide value for money to the public. It conducts a rigorous appraisal of the project’s feasibility, risk allocation, and procurement process before granting approval. Its mandate covers projects with a capital cost of ₹250 crore or more.

- NITI Aayog:

- NITI Aayog (National Institution for Transforming India) plays a crucial role in the long-term policy and planning aspects of infrastructure, including PPPs. It is involved in appraising PPP projects and has been instrumental in driving policy reforms and promoting new models like asset monetization.

- Department of Economic Affairs (DEA), Ministry of Finance:

The Role of Model Concession Agreements (MCAs)

- The development and adoption of Model Concession Agreements have been a cornerstone of India’s strategy to promote PPPs by standardizing the contractual framework.

- What is an MCA?: An MCA is a pre-approved, template contract that defines the legal relationship, rights, and obligations of the public authority and the private concessionaire for a PPP project.

- Objectives of MCAs:

- Standardization: MCAs provide a standard template for PPP contracts, which reduces the time and cost associated with drafting and negotiating individual contracts for each project.

- Balanced Risk Allocation: The MCAs are designed to provide a fair and equitable allocation of risks between the public and private partners, based on the principle of allocating risk to the party best able to manage it. This balanced approach is crucial for attracting private investment. For example, in the roads sector, the MCA clearly defines the allocation of risks related to land acquisition, traffic revenue, and force majeure events.

- Increased Transparency and Certainty: By providing a clear and standardized framework, MCAs enhance transparency in the procurement process and provide greater legal and commercial certainty to bidders and lenders.

- Sector-Specific MCAs: The government has developed different MCAs for various sectors, including National Highways (for both BOT-Toll and HAM models), ports, and urban water supply, recognizing that the risk profile and contractual requirements vary from sector to sector.

Dispute Resolution Mechanisms

- Given the long-term and complex nature of PPP contracts, disputes are inevitable. An effective, efficient, and credible dispute resolution mechanism is therefore a critical component of the legal framework, as it directly impacts investor confidence.

- Common Causes of Disputes: Disputes in PPP projects can arise from various issues, such as delays in land acquisition, disagreements over performance standards, changes in law, or disputes over payment calculations.

- Multi-Tiered Approach: PPP contracts in India typically provide for a multi-tiered dispute resolution process:

- Negotiation/Amicable Settlement: The first step is usually for the parties to try and resolve the dispute through mutual negotiation and discussion.

- Dispute Resolution Board (DRB)/Expert Adjudication: Some contracts provide for the referral of disputes to a pre-constituted board of independent experts who can provide a non-binding or binding recommendation.

- Arbitration: If the dispute cannot be resolved through the earlier stages, it is referred to arbitration. This is the most common formal dispute resolution mechanism in Indian PPP contracts. The proceedings are governed by the Arbitration and Conciliation Act, 1996. Arbitration is often preferred over court litigation because it can be faster, more flexible, and allows for the appointment of arbitrators with specific technical expertise.

- Litigation: The final recourse is to the courts, typically for challenging the arbitral award on limited grounds.

- Challenges in Dispute Resolution:

- Despite the established mechanisms, dispute resolution in Indian PPPs has faced challenges, including lengthy arbitration proceedings and frequent challenges to arbitral awards in courts.

- To address this, there has been a push for reforms to make arbitration more efficient and to explore other mechanisms like statutory expert bodies for adjudication, similar to the Electricity Appellate Tribunal. The NHAI, which has a large number of payment-related disputes, has been actively seeking to resolve them through conciliation committees.

Identifying and Classifying PPP Risks

- Risk management is the heart of a Public-Private Partnership. A PPP is essentially a contract for managing the risks associated with delivering a public service or asset. The process begins with the comprehensive identification and classification of all potential risks throughout the project’s lifecycle.

- The Risk Management Process: This is a systematic process that involves:

- Risk Identification: Creating a comprehensive list of all possible risks that could affect the project.

- Risk Analysis: Assessing the likelihood (probability) and impact (consequences) of each identified risk.

- Risk Allocation: Assigning the responsibility for managing each risk to either the public or private partner.

- Risk Mitigation: Developing strategies to reduce the likelihood or impact of the risks.

- Common Categories of PPP Risks: Risks in PPP projects are typically grouped into several categories:

- Site and Pre-Development Risks:

- These risks occur before construction begins. They include delays in land acquisition, unforeseen adverse geological conditions, and failure to obtain necessary environmental clearances and permits. In India, land acquisition has historically been one of the biggest risks, causing significant delays and cost overruns in highway and other infrastructure projects.

- Design and Construction Risks:

- These relate to the project’s construction phase. They include design errors, cost overruns due to increases in material or labor prices, construction delays, and failure to meet technical specifications. This category of risk is almost always transferred to the private partner.

- Operational Risks:

- These risks arise during the long-term operational phase of the project. They include higher-than-expected operation and maintenance (O&M) costs, failure of the asset or technology, and inability to meet the specified service level or performance standards.

- Demand or Revenue Risk:

- This is the risk that the actual usage of the asset, and therefore the revenue generated from it, will be lower than forecasted. This is a major risk in user-fee based projects like toll roads. For example, the Delhi Airport Metro Express Line project suffered from significantly lower ridership than projected (averaging only around 11,000 passengers per day against a projection of over 46,000), which was a key factor in its financial troubles.

- Financial and Macroeconomic Risks:

- These include risks related to the project’s financing. Examples are increases in interest rates, inflation, and currency exchange rate fluctuations (particularly for projects with foreign debt or imported equipment).

- Regulatory and Political Risks:

- These risks stem from the actions of the government. They include changes in law or tax policy that adversely affect the project, delays in getting necessary government approvals, and in extreme cases, expropriation of the asset. A change in government can also lead to a change in policy or a desire to renegotiate contracts, creating uncertainty.

- Force Majeure Risk:

- This refers to the risk of unforeseeable and uncontrollable events, such as natural disasters (earthquakes, floods), war, or pandemics. The COVID-19 pandemic was declared a force majeure event by the Indian government, allowing for extensions and relief measures for many PPP projects.

- Site and Pre-Development Risks:

- The Risk Management Process: This is a systematic process that involves:

The Principle of Optimal Risk Allocation

- The central tenet of risk management in PPPs is the principle of optimal risk allocation. A successful PPP does not aim to transfer the maximum possible risk to the private sector, but rather to allocate each specific risk to the party that is best able to manage it.

- Who is “Best Able to Manage” a Risk?: This principle is based on several factors:

- Control: The party that has the most control over the factors that influence the risk is best placed to manage it. For example, the private contractor has direct control over construction quality and timelines, so it is best placed to manage construction risk.

- Expertise: The party with the most experience and expertise in dealing with a particular risk should manage it. Private construction and operations companies typically have more expertise in these areas than government departments.

- Cost of Management: The risk should be allocated to the party that can manage or mitigate it at the lowest cost.

- Incentives: Allocating a risk to a party also creates a strong incentive for that party to prevent the risk from materializing or to minimize its impact.

- The Risk Allocation Matrix:

- The outcome of the risk allocation process is documented in a “Risk Allocation Matrix.” This is a table that lists all identified risks and clearly specifies whether each risk is to be retained by the public sector, transferred to the private sector, or shared between the two. This matrix is a critical part of the PPP contract.

- Risk Allocation in Indian PPP Models:

- BOT (Toll): In this model, the private sector bears the construction, O&M, financial, and revenue (traffic) risks. The public sector typically retains risks related to land acquisition, political events, and changes in law. The high revenue risk borne by the private sector was a key reason for the model’s challenges.

- BOT (Annuity): Here, the revenue risk is transferred back to the public sector, as the government provides fixed annuity payments. The private sector still bears construction and O&M risks.

- HAM: This model involves a more balanced sharing of financial risk, with the government providing 40% of the capital cost. The revenue risk is fully retained by the government. This sharing of risks has made the HAM model more bankable and attractive to private developers.

- Who is “Best Able to Manage” a Risk?: This principle is based on several factors:

Risk Mitigation Strategies

- Once risks are allocated, both parties must employ strategies to mitigate or manage them. These strategies can be contractual, financial, or operational.

- Government Support and Guarantees:

- As discussed earlier, the government can mitigate risks for the private partner by providing financial support (like VGF), revenue guarantees (like annuity payments), or guarantees to lenders against specific political or default risks. This reduces the overall risk profile of the project and lowers the cost of finance.

- Contractual Provisions:

- Force Majeure Clause: The PPP contract clearly defines what constitutes a force majeure event and specifies the consequences, such as extension of the concession period or termination of the contract with compensation. Indian contract law recognizes the doctrine of frustration, but specific force majeure clauses in PPP contracts provide more clarity.

- Change in Law Clause: This clause protects the private partner from adverse financial impacts resulting from changes in laws or regulations after the contract is signed. It typically provides a mechanism for adjusting tariffs or the concession period to restore the private partner to the same economic position.

- Termination Clauses: The contract specifies the conditions under which either party can terminate the agreement and outlines the compensation payable in different termination scenarios (e.g., termination due to public sector default vs. private sector default).

- Financial Mitigation Measures:

- Escrow Accounts: An escrow account, managed by a neutral third-party bank, is often used to ensure the security of payments. Project revenues are deposited into this account, and funds are disbursed according to a pre-agreed “waterfall” mechanism, with lenders typically having the first claim. This mitigates the payment risk for lenders and the private operator.

- Hedging: For projects exposed to financial risks like interest rate or currency fluctuations, the SPV can use financial instruments like interest rate swaps or currency futures to hedge against these risks.

- Insurance:

- The private partner is required to take out comprehensive insurance policies to cover various risks, such as “Contractor’s All Risk” insurance during construction and insurance against property damage and third-party liability during operations. This transfers some of the financial impact of these risks to the insurance market.

- Government Support and Guarantees:

The Need for Performance Measurement in PPPs

- Evaluating the performance of Public-Private Partnerships is essential to determine whether they are achieving their intended objectives and delivering the promised Value for Money (VfM). A robust performance evaluation framework is crucial for accountability, learning, and improving future PPP projects.

- Performance evaluation in PPPs is a continuous process that occurs throughout the project lifecycle, from the initial appraisal to the post-implementation review.

- Ex-ante Evaluation (Appraisal): This is done before the project is procured. It involves assessing the project’s feasibility, potential VfM, and comparing the PPP option with traditional public procurement.

- Concurrent Evaluation (Monitoring): This happens during the construction and operation phases. It involves monitoring the private partner’s performance against the standards set in the contract.

- Ex-post Evaluation (Review): This is conducted after the project has been operational for some time. It assesses the project’s actual outcomes and impacts against its initial goals.

Key Performance Indicators (KPIs)

- Key Performance Indicators (KPIs) are the specific, measurable metrics used to track and evaluate the performance of a PPP project. They are a central part of the PPP contract and are directly linked to the payment mechanism.

- Characteristics of Good KPIs:

- Specific: Clearly defined and unambiguous.

- Measurable: Can be quantified and measured objectively.

- Achievable: Realistic and attainable by the private partner.

- Relevant: Directly related to the project’s objectives and the quality of service.

- Time-bound: Measured over a specific time frame.

- Categories of KPIs in PPP Projects: KPIs can be categorized based on the aspect of performance they measure. A study on PPP infrastructure projects proposed a framework with several key performance indicators:

- Financial Performance Indicators:

- Construction Cost: Whether the project was completed within the budgeted cost.

- Operational Cost: The efficiency of the project’s operations and maintenance.

- Return on Investment (ROI): The financial return generated by the project.

- Time Performance Indicators:

- Construction Period: Whether the project was completed on schedule.

- Quality and Technical Performance Indicators:

- Quality of Construction: Adherence to design and material specifications.

- Service Availability: The percentage of time the asset or service is available for use (e.g., a highway lane is not closed for repairs).

- Service Quality: Meeting the specified standards of service delivery (e.g., smoothness of a road surface, cleanliness of a hospital).

- Stakeholder Satisfaction Indicators:

- User Satisfaction: The level of satisfaction of the end-users of the service.

- Public/Community Support: The level of support for the project from the local community.

- Risk Management Indicators:

- Effectiveness of Risk Allocation: Whether the risk allocation proved to be efficient in practice.

- Financial Performance Indicators:

- Linking KPIs to Payments:

- In a PPP, the private partner’s revenue is directly linked to its performance against the agreed KPIs.

- If performance falls below the required standard, penalties are applied in the form of deductions from the government’s payments (in the case of annuity/availability-based projects) or other contractual remedies. This creates a powerful financial incentive for the private partner to maintain high standards of performance.

- Characteristics of Good KPIs:

Methodologies for PPP Evaluation

- Several methodologies are used to evaluate the performance and viability of PPP projects, particularly during the appraisal stage.

- Value for Money (VfM) Analysis:

- VfM analysis is the core evaluation method used to decide whether to procure a project as a PPP or through traditional public means.

- It compares the total lifecycle cost of the project under the PPP model with the cost of the project if it were delivered by the public sector.

- The analysis is not just about the lowest cost; it also considers the quality of service and the value of the risks transferred to the private sector.

- The Public Sector Comparator (PSC):

- The PSC is the key tool used in quantitative VfM analysis. It is a risk-adjusted estimate of the total lifecycle cost of the project if the public sector were to deliver it.

- Components of a PSC:

- Raw PSC: The estimated capital and operating costs of the project under public procurement.

- Competitive Neutrality Adjustment: An adjustment to account for any competitive advantages the public sector might have, such as exemption from certain taxes, to ensure a fair comparison.

- Transferable Risk Adjustment: An estimate of the value of the risks that would be transferred to the private partner under a PPP.

- Retained Risk Adjustment: An estimate of the value of the risks that would be retained by the public sector.

- The VfM Test: The final PSC value is then compared to the bid price submitted by the private partner for the PPP. If the PPP bid is lower than the PSC, the project is considered to offer Value for Money.

- Social Return on Investment (SROI):

- While VfM and PSC focus on the financial value to the government, SROI is a broader methodology used to measure the social, economic, and environmental value created by a project.

- SROI attempts to monetize social outcomes, such as improved health, reduced travel time, or a cleaner environment.

- The SROI ratio is calculated as: [latex]SROI = \frac{\text{Net Present Value of Benefits}}{\text{Net Present Value of Investment}}[/latex]. An SROI ratio of 3:1 means that for every ₹1 invested, ₹3 of social value is created.

- SROI is particularly useful for evaluating social sector PPPs, where the financial returns may be low, but the social benefits are high.

- Post-Implementation Review (PIR):

- A PIR is a formal review conducted after a project has been completed and is operational.

- It assesses whether the project has met its original objectives, delivered the expected benefits, and stayed within its budget and timeline.

- A key objective of a PIR is to identify lessons learned that can be applied to future projects.

- Value for Money (VfM) Analysis:

Performance Evaluation in India: The Role of the CAG

- In India, the Comptroller and Auditor General (CAG) plays a crucial independent oversight role in the performance evaluation of PPP projects.

- CAG’s Mandate: The CAG conducts performance audits of PPP projects to examine their economy, efficiency, and effectiveness. The audit scrutiny extends to checking whether the PPP arrangement has achieved the desired policy objectives and delivered VfM.

- Key Findings from CAG Audits: CAG reports have often been critical of the implementation of PPP projects in India, highlighting several issues:

- Unfavorable Risk Allocation: In some projects, risks were not properly transferred to the private partner, or the government ended up bearing unforeseen risks. The CAG report on the Delhi Airport PPP, for instance, made adverse comments on this aspect.

- Lack of Transparency: Reports have pointed to a lack of transparency in the bidding and contract award process.

- Inadequate Monitoring: CAG has highlighted weaknesses in the government’s capacity to monitor the performance of private concessionaires.

- Revenue Loss to Government: In some port projects, CAG found issues with the fixation of royalties and other charges, leading to potential revenue loss for the port authorities. A 2014 performance audit on PPPs in Indian Railways noted significant shortfalls in achieving the expected private investment and outcomes.

Comparison of Core PPP Models

- The selection of an appropriate PPP model is a critical decision that significantly influences a project’s risk profile, financial structure, and ultimate success. A comparative understanding of the most common models used in India—EPC, BOT (Toll), BOT (Annuity), and HAM—is essential for economic analysis.

- Comparative Chart of Indian Infrastructure ModelsFeatureEPC (Engineering, Procurement, Construction)BOT (Toll) (Build-Operate-Transfer)BOT (Annuity) (Build-Operate-Transfer)HAM (Hybrid Annuity Model)Primary ResponsibilityPrivate contractor executes the project for a fixed fee.Private concessionaire finances, builds, operates, and maintains.Private concessionaire finances, builds, and maintains.Private developer designs, builds, operates, and maintains.Capital Funding100% Government funded.100% Private sector funded.100% Private sector funded.40% Government, 60% Private sector.Revenue/PaymentFixed payment from government to contractor.Concessionaire collects toll from users.Fixed annuity payments from government to concessionaire.Fixed annuity payments plus O&M costs from government.Construction RiskPrimarily with the government (cost overruns).Borne by the private concessionaire.Borne by the private concessionaire.Borne by the private developer.O&M RiskBorne by the government.Borne by the private concessionaire.Borne by the private concessionaire.Borne by the private developer.Traffic/Revenue RiskBorne by the government (no direct revenue).Borne by the private concessionaire.Borne by the government.Borne by the government.Financing RiskBorne by the government.Borne by the private concessionaire.Borne by the private concessionaire.Shared between government and private developer.Government OutflowFull capital cost paid during construction.No direct outflow (may provide VGF).Annuity payments over concession period.40% during construction, annuity payments thereafter.SuitabilityProjects with clear scope, low complexity.Projects with high and predictable traffic flow.Projects with socio-economic benefits but uncertain traffic.Projects where private funding is constrained and traffic risk is high.

International Best Practices in PPPs

- Countries with mature PPP markets like the United Kingdom, Australia, and Canada offer valuable lessons and best practices that can inform and improve the implementation of PPPs in India.

- Strong Legal and Institutional Framework:

- Best practice demands a clear, stable, and transparent legal and institutional framework for PPPs. This includes a dedicated PPP law or policy, a central PPP unit with technical expertise, and standardized procurement procedures.

- Example: Australia has well-established PPP units at both the national and state levels (e.g., Infrastructure Australia, Partnerships Victoria) that provide expert guidance and ensure consistency in project development and procurement.

- Rigorous Project Preparation and Appraisal:

- Successful PPP programs emphasize the importance of thorough project preparation and appraisal before a project is brought to market. This includes conducting detailed feasibility studies, robust Value for Money (VfM) analysis, and comprehensive risk assessments.

- Example: The UK Treasury’s “Green Book” provides detailed guidance on the appraisal and evaluation of all central government projects, including a systematic process for assessing the case for a PPP.

- Focus on Whole-Life Costing and Value:

- A key lesson is that the lowest bid price does not always equate to the best value. Procurement processes should be designed to reward durability, reliability, and long-term public benefit.

- Evaluation criteria in best-practice jurisdictions are multi-faceted, weighting a bidder’s technical capacity, financial stability, innovation, and environmental, social, and governance (ESG) credentials alongside the price.

- Transparency and Stakeholder Engagement:

- Ensuring transparency throughout the PPP lifecycle—from procurement to contract management—is crucial for maintaining public trust and accountability. This includes the proactive disclosure of key project information and contract details.

- Early and continuous engagement with all stakeholders, including the local community, is vital for building support and mitigating social and political risks.

- Effective Contract Management:

- The role of the government does not end once the contract is signed. Best practice requires a dedicated and skilled contract management team on the public side to monitor the private partner’s performance, manage the relationship, and handle contract variations and disputes effectively. A rushed project often becomes a failed project, highlighting the need for patience and diligence.

- Developing a Mature Financial Market:

- A deep and liquid financial market is essential for financing PPPs. This includes a robust banking sector, as well as the development of a market for long-term project bonds, which can attract institutional investors like pension funds and insurance companies.

- Example: Canada has successfully used project bonds to finance many of its large infrastructure PPPs, tapping into its large pool of pension fund capital.

- Strong Legal and Institutional Framework:

A Comparative Look at Global PPP Case Studies

- Examining specific case studies from different countries provides concrete insights into the application and outcomes of various PPP approaches.

- The London Underground PPP, UK:

- Context: A massive project to upgrade and maintain London’s aging subway system, structured as three separate 30-year PPP contracts.

- Challenges: The project was marred by complexity, cost overruns, and conflicts between the private contractors and the public operator. The contracts were eventually terminated, and the maintenance responsibilities were brought back in-house.

- Lesson: This case highlights the risks of overly complex PPP structures and the difficulty of applying PPPs to highly integrated, existing “brownfield” infrastructure systems. It underscores the importance of clear interfaces and a strong public sector capacity to manage complex contracts.

- The Confederation Bridge, Canada:

- Context: A 12.9 km bridge connecting Prince Edward Island to the mainland, built under a DBFO (Design-Build-Finance-Operate) model. The private consortium receives an annual subsidy from the government and collects tolls.

- Success: The project was completed on time and on budget. It is often cited as a successful example of a large-scale infrastructure PPP.

- Lesson: The success was attributed to a well-defined project scope, a transparent and competitive procurement process, and a clear allocation of risks.

- The Madinah Airport Expansion, Saudi Arabia:

- Context: The first airport project in the Middle East to be procured as a full PPP. A private consortium was given a concession to expand and operate the Prince Mohammed bin Abdulaziz International Airport.

- Success: The project was completed on time and has been operating successfully, serving as a model for other airport PPPs in the region.

- Lesson: This case demonstrates the potential of PPPs to bring private sector finance and operational expertise to complex infrastructure projects even in emerging PPP markets, provided there is strong government commitment and a well-structured concession agreement.

- The Rewa Ultra Mega Solar Park, India:

- Context: A 750 MW solar power project in Madhya Pradesh, structured as a PPP.

- Success: The project achieved a record-low tariff for solar power in India at the time of its bidding. It has mobilized significant private investment (around $575 million) and is reducing greenhouse gas emissions by 1 million tons per year.

- Lesson: This project showcases how the PPP model can be effectively used to drive investment in renewable energy and achieve climate goals. The innovative risk mitigation measures and payment security mechanisms used in the project were key to attracting bidders and achieving a low tariff.

- The London Underground PPP, UK:

The Imperative of Strong PPP Governance

- Effective governance is the bedrock upon which successful and sustainable Public-Private Partnerships are built. It encompasses the institutions, policies, processes, and systems that a government puts in place to plan, procure, manage, and oversee its PPP projects. Weak governance can lead to poor project selection, inefficient procurement, value erosion, and fiscal risks, ultimately undermining the public interest.

- The OECD has outlined several key principles for the public governance of PPPs, which serve as an international benchmark. These principles emphasize the need for:

- A clear, predictable, and legitimate institutional framework.

- Ensuring that the PPP procurement process is competitive and transparent.

- Budgetary transparency and robust fiscal management.

- Integrity and the prevention of corruption.

Institutional Framework: The Role of a Central PPP Unit

- A common feature in countries with successful PPP programs is the establishment of a dedicated, central Public-Private Partnership Unit.

- What is a PPP Unit?: A PPP unit is a specialized organization or agency within the government, often located in the Ministry of Finance or a central planning agency, that is responsible for promoting, facilitating, and overseeing the country’s PPP program. India’s PPP Cell in the Department of Economic Affairs serves this function.

- Key Roles and Responsibilities of a PPP Unit:

- Policy and Framework Development: Developing and updating the national PPP policy, guidelines, and standardized documentation (like Model Concession Agreements).

- Technical Expertise and Support: Acting as a center of excellence for PPPs, providing technical assistance and expert advice to the government line ministries and agencies that are implementing projects. This can include help with project identification, feasibility studies, risk analysis, and contract structuring.