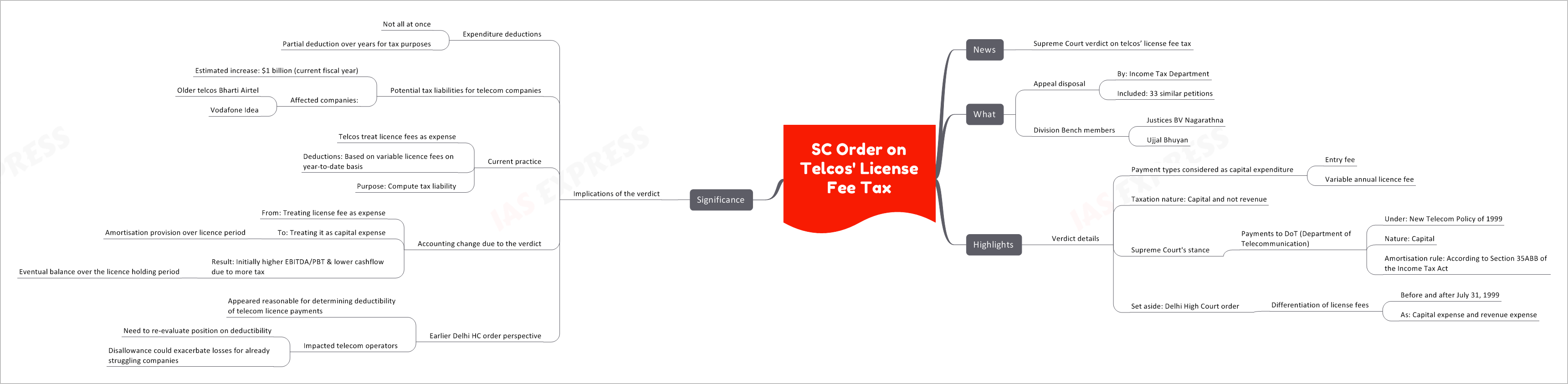

SC Order on Telcos’ License Fee Tax

In recent news, the Supreme Court has delivered a significant verdict concerning the taxation of license fees paid by telecom companies. This verdict has far-reaching implications for telecom operators, particularly in terms of their tax liabilities and accounting practices.

The Appeal Disposal

By the Income Tax Department

The case in question was disposed of in response to an appeal made by the Income Tax Department.

Inclusion of 33 Similar Petitions

The verdict also covers 33 similar petitions related to the taxation of license fees.

Division Bench Members

The case was presided over by a Division Bench consisting of:

- Justice BV Nagarathna

- Justice Ujjal Bhuyan

Verdict Details

Payment Types Considered as Capital Expenditure

The Supreme Court’s verdict focuses on the treatment of certain payments as capital expenditure. These payments include:

- Entry Fee

- Variable Annual License Fee

Taxation Nature: Capital and Not Revenue

The central determination of the verdict is that these payments should be treated as capital expenditures for taxation purposes.

Supreme Court’s Stance on Payments to DoT

The payments made to the Department of Telecommunication (DoT) under the New Telecom Policy of 1999 were deemed to have a capital nature. They should be amortized in accordance with Section 35ABB of the Income Tax Act.

Set Aside: Delhi High Court Order

The verdict sets aside the Delhi High Court’s order, which had differentiated between license fees before and after July 31, 1999, categorizing them as either capital or revenue expenses.

Significance of the Verdict

Implications of the Verdict

Expenditure Deductions

The verdict implies that telecom companies cannot deduct all license fee expenses at once for tax purposes. Instead, they are eligible for partial deductions over several years.

Potential Tax Liabilities for Telecom Companies

- The estimated increase in tax liabilities for the current fiscal year is approximately $1 billion.

- Affected companies include older telecom giants like Bharti Airtel and Vodafone Idea.

Current Practice

Prior to the verdict, telecom companies typically treated license fees as an expense, determining deductions based on variable license fees on a year-to-date basis for computing their tax liability.

Accounting Change Due to the Verdict

The verdict necessitates an accounting change for telecom companies. They must now treat license fees as capital expenses and amortize them over the license holding period. This will result in initially higher EBITDA/PBT (Earnings Before Interest, Taxes, Depreciation, and Amortization/Profit Before Tax) and lower cash flow due to increased tax obligations. However, these effects will eventually balance out over the license holding period.

Earlier Delhi HC Order Perspective

The previous order of the Delhi High Court, which allowed for the deductibility of telecom license payments, appeared reasonable. It had a significant impact on telecom operators, prompting them to re-evaluate their position on deductibility. Any disallowance of these deductions could exacerbate the financial challenges faced by telecom companies, which are already struggling.

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses