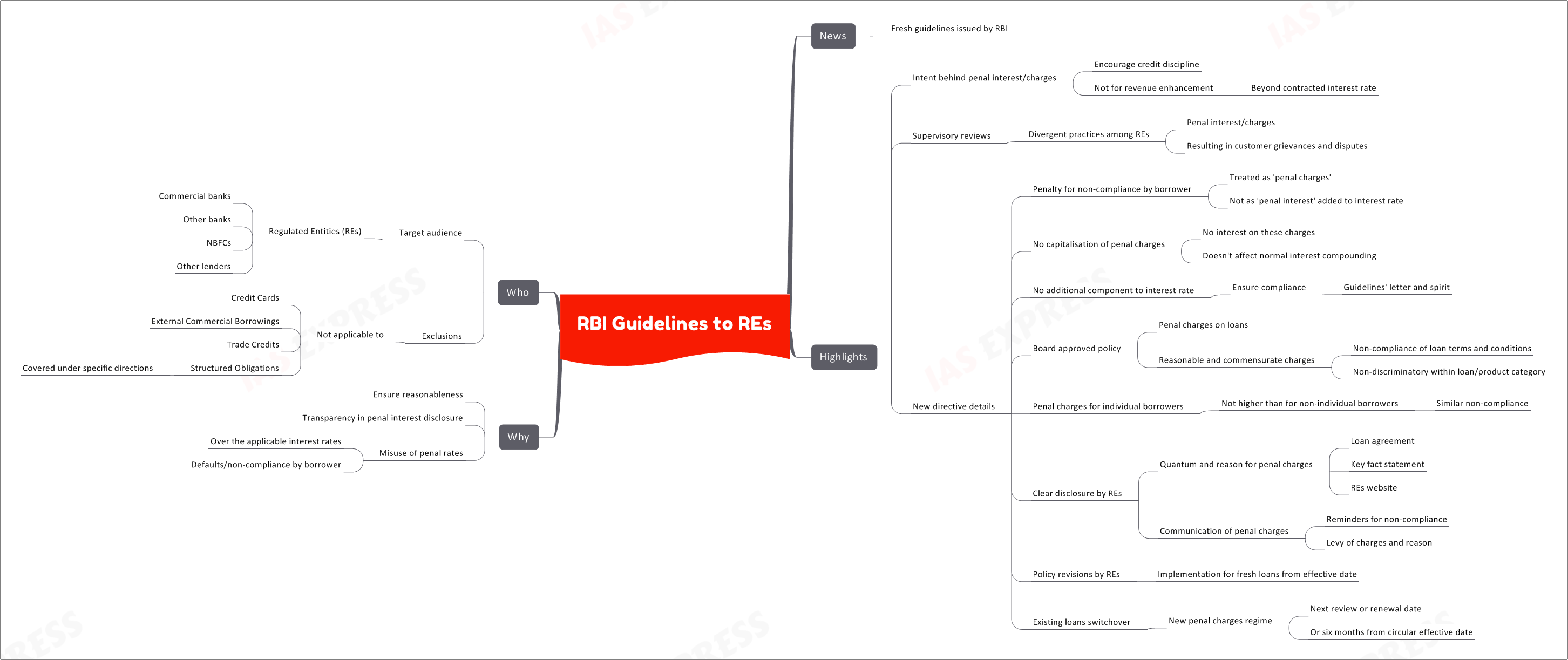

RBI Guidelines to Regulated Entities

The Reserve Bank of India (RBI) has taken a significant stride in refining the lending landscape with its latest guidelines directed towards Regulated Entities (REs). This set of comprehensive directives aims to create transparency, fairness, and credit discipline by streamlining the approach to penal interest and charges associated with non-compliance by borrowers.

Key Highlights of the Guidelines

Intent Behind Penal Interest/Charges

The primary objective of these guidelines is to encourage credit discipline among borrowers. It’s essential to note that the imposition of penal interest/charges is not intended for revenue enhancement beyond the contracted interest rate.

Navigating Supervisory Reviews

The guidelines stem from divergent practices among REs regarding the application of penal interest/charges, which often leads to customer grievances and disputes. The RBI’s intervention seeks to standardize these practices for the benefit of both lenders and borrowers.

Understanding the New Directives in Detail

The guidelines offer clear directives on various aspects:

- Penalty for Non-Compliance: Non-compliance by borrowers is to be treated as ‘penal charges,’ distinct from ‘penal interest’ added to the interest rate. This differentiation ensures fairness in the treatment of borrowers.

- Non-Capitalization of Penal Charges: Penal charges are not to be capitalized, thereby eliminating the imposition of interest on these charges. Normal interest compounding remains unaffected.

- No Additional Component to Interest Rate: The guidelines stipulate that no additional component should be added to the interest rate. This ensures strict compliance with the spirit of the guidelines.

- Board-Approved Policy: REs must have a board-approved policy regarding penal charges. These charges must be reasonable, commensurate with the non-compliance of loan terms, and non-discriminatory within the loan/product category.

- Parity for Individual Borrowers: Penal charges for individual borrowers should not be higher than those for non-individual borrowers for similar non-compliance instances.

Ensuring Clarity and Communication

- Clear Disclosure: REs must clearly disclose the quantum and reason for penal charges in the loan agreement, key fact statement, and on their website.

- Effective Communication: Borrowers must be communicated with reminders for non-compliance, as well as the levy of charges and the reason for their imposition.

Implementing the Guidelines

- Policy Revisions: REs are required to implement these guidelines for fresh loans from the effective date of the circular.

- Transition for Existing Loans: Existing loans will transition to the new penal charges regime on the next review or renewal date or within six months from the circular’s effective date.

The Motive Behind the Guidelines

Establishing Reasonableness and Transparency

The guidelines are designed to instill reasonableness in penal interest/charges and ensure transparency in their disclosure and imposition.

Curbing Misuse of Penal Rates

The guidelines aim to prevent the misuse of penal rates, which sometimes lead to penal charges that exceed applicable interest rates, especially in cases of borrower defaults or non-compliance.

The Target Audience

Who the Guidelines Apply To

The primary audience for these guidelines is Regulated Entities (REs), which include commercial banks, other banks, non-banking financial companies (NBFCs), and various other lenders.

Exclusions

These guidelines are not applicable to specific domains like Credit Cards, External Commercial Borrowings, Trade Credits, and Structured Obligations, which are covered under separate directions.

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses