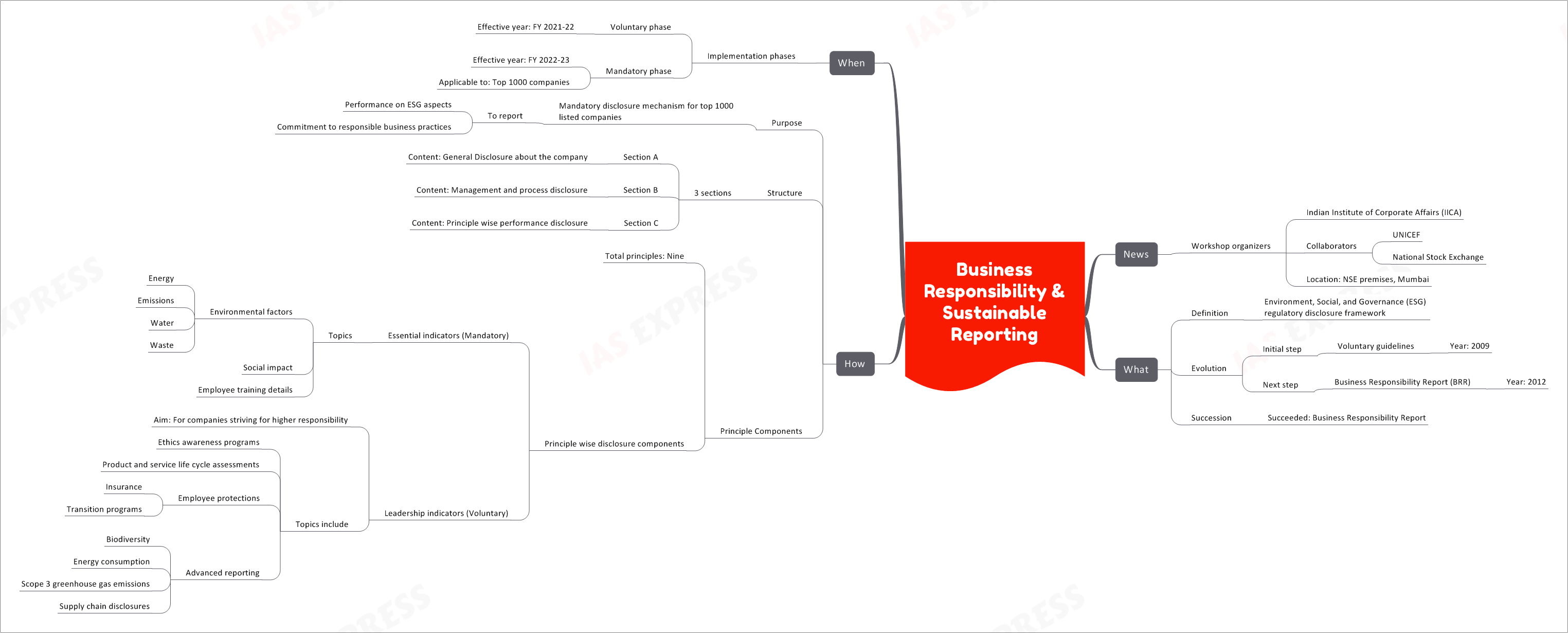

Business Responsibility and Sustainability Reporting

The Business Responsibility and Sustainability Reporting (BRSR) initiative is a critical development in the corporate world, aimed at promoting transparency, ethical practices, and sustainability among businesses.

Workshop Organizers and Collaborators

The BRSR workshop was organized by the Indian Institute of Corporate Affairs (IICA) and saw collaboration from prominent entities such as UNICEF and the National Stock Exchange (NSE). The workshop took place at the NSE premises in Mumbai.

What is BRSR?

Definition

BRSR stands for Business Responsibility and Sustainability Reporting, which serves as an ESG (Environment, Social, and Governance) regulatory disclosure framework.

Evolution

BRSR has evolved through various stages:

Initial Step: Voluntary Guidelines (2009)

In 2009, the journey towards corporate responsibility and sustainability reporting began with the introduction of voluntary guidelines.

Next Step: Business Responsibility Report (BRR) (2012)

In 2012, a significant step was taken with the introduction of the Business Responsibility Report (BRR).

Succession

BRSR has succeeded the Business Responsibility Report, signaling a more structured and comprehensive approach to corporate sustainability and responsibility.

How Does BRSR Work?

Purpose

BRSR serves as a mandatory disclosure mechanism for the top 1000 listed companies. Its primary purpose is to compel these companies to report on their performance regarding ESG aspects and their commitment to responsible business practices.

Structure

BRSR consists of three main sections:

Section A

- Content: General Disclosure about the company

Section B

- Content: Management and process disclosure

Section C

- Content: Principle-wise performance disclosure

Principle Components

BRSR is built around nine principles, each with specific disclosure components. These include:

Essential Indicators (Mandatory)

- Topics:

- Environmental Factors

- Energy

- Emissions

- Water

- Waste

- Social Impact

- Employee Training Details

- Environmental Factors

Leadership Indicators (Voluntary)

- Aim: Designed for companies striving for higher responsibility

- Topics include:

- Ethics Awareness Programs

- Product and Service Life Cycle Assessments

- Employee Protections

- Insurance

- Transition Programs

- Advanced Reporting

- Biodiversity

- Energy Consumption

- Scope 3 Greenhouse Gas Emissions

- Supply Chain Disclosures

When Does BRSR Take Effect?

Implementation Phases

Voluntary Phase

- Effective Year: FY 2021-22

Mandatory Phase

- Effective Year: FY 2022-23

- Applicable to: Top 1000 Companies

In conclusion, the Business Responsibility and Sustainability Reporting (BRSR) framework represents a significant step towards fostering responsible business practices and sustainability among corporations. With its mandatory phase applicable to the top 1000 listed companies, BRSR is expected to drive greater transparency and accountability in the corporate world, benefiting both businesses and society at large.

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses