PRS Monthly Policy Review (October 2025): India’s Structural & Macroeconomic Landscape

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

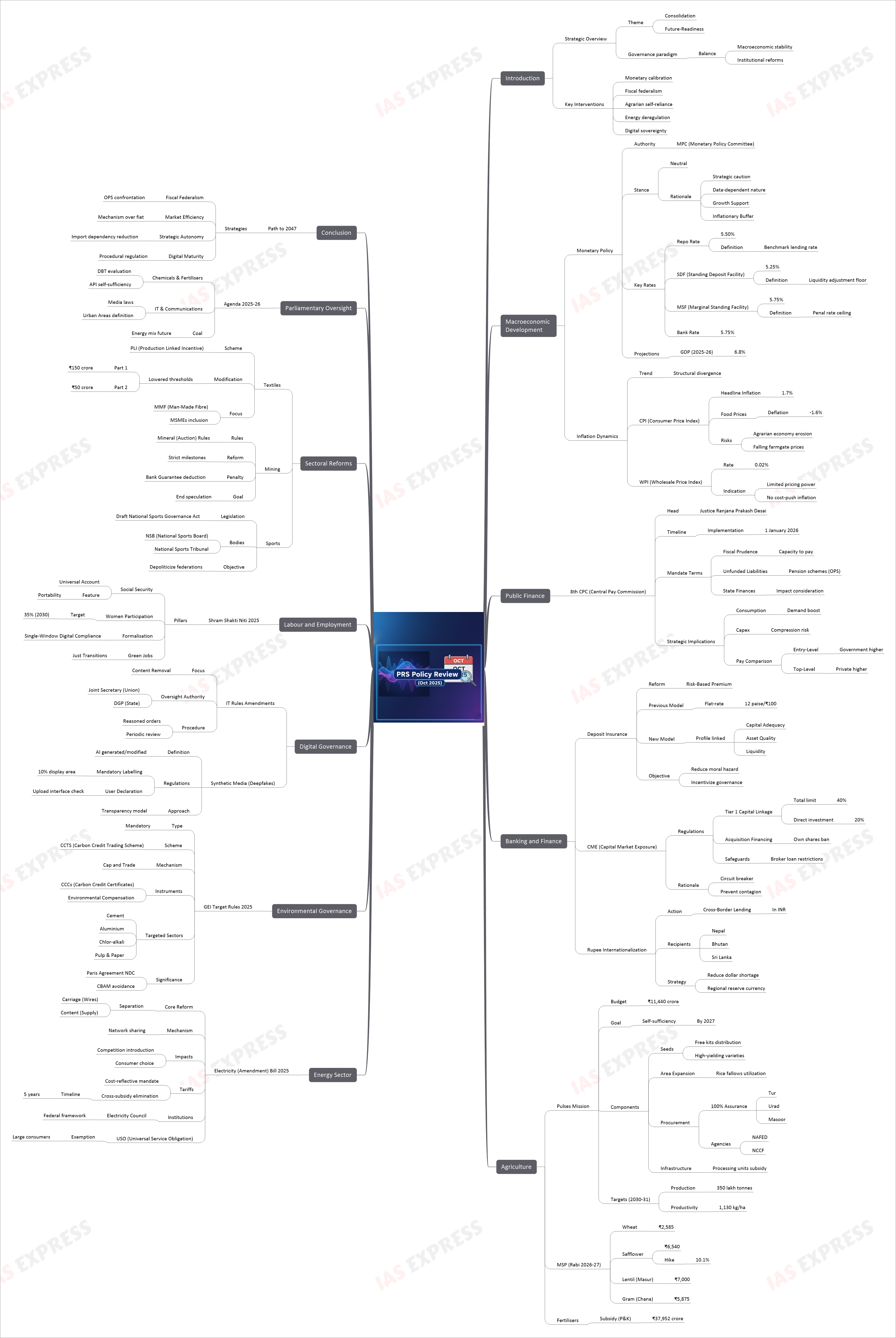

1. Executive Summary and Strategic Overview

October 2025 serves as a microcosm of the broader structural transformation currently reshaping the Indian political economy. The policy interventions observed during this month—spanning monetary calibration, fiscal federalism, agrarian self-reliance, energy deregulation, and digital sovereignty—reflect a governance paradigm that attempts to balance immediate macroeconomic stability with long-term institutional reforms.

The overarching theme of the period is “Consolidation and Future-Readiness.” On the macroeconomic front, the Reserve Bank of India (RBI) has opted for a “neutral” stance, maintaining the repo rate at 5.5% to foster growth, which is now projected at an upgraded 6.8% for 2025-26. This monetary stability provides the foundation for ambitious fiscal and sectoral reforms. The constitution of the Eighth Central Pay Commission (CPC) marks a pivotal moment in fiscal management, explicitly tasked with balancing employee welfare against the fiscal prudence required for developmental expenditure, particularly in the context of the contentious Old Pension Scheme (OPS) debate.

Sectoral reforms demonstrate a shift from state-led protectionism to market-based efficiency. The agricultural sector witnesses a decisive push for “Aatmanirbharta” in pulses to cure chronic import dependency and protein inflation. The energy sector faces its most radical overhaul since 2003, with the draft Electricity (Amendment) Bill, 2025, proposing the separation of carriage and content through network sharing—a move aimed at dismantling public monopolies to aid industrial competitiveness. Simultaneously, environmental governance is being institutionalized through the Greenhouse Gas Emission Intensity (GEI) Target Rules, transitioning India from voluntary targets to a mandatory, market-linked carbon credit regime.

In the digital domain, the state is reasserting its role as a regulator of information integrity. New amendments to IT Rules target the rising threat of “synthetically generated information” (Deepfakes), establishing high-level bureaucratic oversight for content moderation to balance national security with constitutional liberties.

This comprehensive report offers an exhaustive analysis of these developments, structured as detailed study notes suitable for advanced policy analysis and Civil Services preparation. It integrates historical context, economic theory, and legislative nuance to interpret not just what happened, but why it matters for India’s trajectory towards 2047.

2. Macroeconomic Development: Monetary Policy and Inflation Dynamics

The macroeconomic environment in October 2025 is characterized by a “Goldilocks” scenario of robust growth and moderating inflation, though underlying structural divergences necessitate vigilant policy calibration.

2.1 Monetary Policy Statement: The Rationale for the Neutral Stance

The Monetary Policy Committee (MPC) of the Reserve Bank of India, in its review ending October 1, 2025, voted to maintain the status quo on policy rates.

2.1.1 Key Policy Rates and Decisions

| Policy Rate / Tool | Current Rate (Oct 2025) | Status | Definition & Significance |

| Repo Rate | 5.50% | Unchanged | The benchmark interest rate at which the RBI lends to commercial banks against government securities. It anchors the cost of capital in the economy. |

| Standing Deposit Facility (SDF) | 5.25% | Unchanged | The floor of the liquidity adjustment facility corridor. It allows the RBI to absorb excess liquidity from banks without offering collateral. |

| Marginal Standing Facility (MSF) | 5.75% | Unchanged | A penal rate for banks borrowing overnight funds above the statutory limit; acts as the ceiling for the interest rate corridor. |

| Bank Rate | 5.75% | Unchanged | The rate at which the RBI lends for long-term requirements; also used as a penal rate for SLR/CRR defaults. |

| GDP Projection (2025-26) | 6.8% | Upgraded | Revised upwards from 6.5%, indicating strong investment demand and consumption resilience. |

2.1.2 Analysis of the “Neutral Stance”

The decision to maintain a neutral stance despite low headline inflation (1.7%) is rooted in strategic caution. A “neutral” stance implies that the central bank is not committed to either hiking or cutting rates in the immediate future; it is data-dependent.

- Growth Support: By not raising rates, the RBI supports the credit growth necessary for the projected 6.8% GDP expansion. The upgrade in GDP estimates reflects improved capacity utilization in manufacturing and sustained momentum in services.

- Inflationary Buffer: Although current inflation is low, the RBI is wary of “event risks”—geopolitical tensions affecting oil prices or erratic monsoons impacting food supply. Keeping real interest rates positive (Repo Rate 5.5% minus Inflation 1.7% = ~3.8% Real Rate) encourages savings and prevents asset bubbles.

2.2 Inflation Dynamics: The Divergence Dilemma

The inflation data for the second quarter (July-September) of 2025-26 reveals a significant structural divergence between consumer and wholesale prices, primarily driven by the food basket.

2.2.1 Consumer Price Index (CPI)

- Headline Inflation: Averaged 1.7%, a sharp deceleration from 4.3% in the corresponding quarter of 2024-25.

- Food Price Deflation: The critical driver was a 1.6% decline in food prices. In contrast, the previous year saw a 6.8% rise in food prices.

- Insight: While beneficial for urban consumers (lower cost of living), deflation in food prices poses a severe risk to the agrarian economy. It implies falling farmgate prices, which could erode farmer incomes and suppress rural demand for industrial goods (FMCG, two-wheelers).

- Implications for UPSC: Aspirants must note that sustained low food inflation can lead to “terms of trade” turning against agriculture. This explains the government’s parallel move to increase MSPs and launch the Pulses Mission to provide price support.

2.2.2 Wholesale Price Index (WPI)

- WPI Inflation: Averaged 0.02%, hovering near zero, compared to 1.8% in the previous year.

- Pricing Power: Near-zero WPI indicates that manufacturers have very limited pricing power. Input costs are stable, but they cannot raise output prices due to competitive pressures or fragile demand recovery in certain segments.

- Policy Correlation: The low WPI confirms that there is no “cost-push” inflation currently threatening the economy, validating the RBI’s decision to pause rate hikes.

3. Public Finance and Fiscal Federalism: The 8th Pay Commission

The constitution of the Eighth Central Pay Commission (CPC) is the single most significant fiscal event of October 2025, with ramifications that will extend well into the 2030s. Pay Commissions in India are not just salary review bodies; they are instruments of socio-economic policy that reset the baseline for public expenditure and center-state fiscal relations.

3.1 Context and Mandate

The Union Cabinet approved the Terms of Reference (ToR) for the 8th CPC, headed by Justice Ranjana Prakash Desai (Retd.). The recommendations are slated for implementation from January 1, 2026.

3.1.1 Historical Context of Pay Commissions

- First CPC (1946): Establishing the structure of the civil service in independent India.

- Decadal Cycle: Pay Commissions are typically constituted every 10 years to adjust public sector compensation for inflation and changing economic realities.

- Seventh CPC (2016): Introduced the “Pay Matrix” and recommended a 23.55% hike, which added approximately ₹1.02 lakh crore to the government’s annual expenditure.

3.1.2 The Unique Mandate of the 8th CPC

The ToR for the 8th CPC contains specific clauses that reflect the government’s concern over fiscal sustainability:

- Fiscal Prudence vs. Aspirations: The Commission is explicitly mandated to consider the “economic conditions in the country and the need for fiscal prudence”. This suggests that unlike previous commissions that focused heavily on “need-based minimum wage,” the 8th CPC will prioritize the “capacity to pay” of the sovereign.

- Unfunded Pension Liabilities (The OPS Question): A critical addition to the ToR is the examination of the “unfunded cost of non-contributory pension schemes”.

- Analysis: This is a direct response to the political demand for restoring the Old Pension Scheme (OPS). The NPS (National Pension System) is a defined contribution scheme (fiscal neutrality), while OPS is a defined benefit scheme (fiscal burden). By asking the CPC to study the “unfunded cost,” the Centre is likely seeking empirical data to demonstrate the fiscal unsustainability of reverting to OPS, thereby building a case to maintain the NPS architecture.

- Impact on State Finances: The ToR explicitly requires the Commission to keep in view the impact on state finances.

- Federal Ripple Effect: Although the CPC technically covers only Central employees, state governments are politically compelled to match the hikes. Since states spend a larger portion of their budget on salaries than the Centre, a generous CPC award often destabilizes state budgets, crowding out capital expenditure for irrigation and infrastructure.

3.2 Strategic Implications for the Indian Economy

3.2.1 Consumption vs. Investment

- Consumption Boost: Pay Commissions act as a massive fiscal stimulus. The increased disposable income of over 1 crore employees and pensioners typically boosts demand for real estate, automobiles, and consumer durables.

- Capex Compression: Conversely, the higher revenue expenditure (salaries) leaves less room for the government to spend on capital assets (roads, railways). The 8th CPC will need to balance this trade-off to ensure the government’s “Capex-led growth” strategy is not derailed.

3.2.2 The Comparison with the Private Sector

The Commission is tasked with comparing public sector emoluments with the private sector.

- Entry-Level Distortion: Historically, government jobs pay significantly more than private sector jobs at the entry level (Group C/D), creating a distortion where highly over-qualified candidates apply for low-skill government jobs.

- Top-Level Stagnation: At the senior level (Joint Secretary and above), government pay lags behind the corporate sector, leading to a talent drain. The 8th CPC may attempt to correct this skew to attract domain experts into the bureaucracy (Lateral Entry).

4. Banking and Finance: Structural Reforms and Risk Management

The Reserve Bank of India’s regulatory interventions in October 2025 focus on ring-fencing the banking sector from systemic risks and enhancing the global footprint of the Indian Rupee.

4.1 Risk-Based Premium for Deposit Insurance

The RBI has proposed a paradigm shift in how deposit insurance is funded in India, moving from a “flat-rate” to a “risk-based” model.

4.1.1 The Current Framework

- Deposit Insurance and Credit Guarantee Corporation (DICGC): Insures bank deposits up to ₹5 lakh per depositor.

- Flat Premium: Currently, all banks—regardless of whether they are a robust HDFC Bank or a fragile Cooperative Bank—pay a uniform premium of 12 paise per ₹100 of assessable deposits.

- Problem: This creates a “moral hazard” and “cross-subsidization.” Sound banks effectively subsidize the risk-taking behavior of weaker banks.

4.1.2 The Proposed Risk-Based Model

- Mechanism: The premium will be linked to the bank’s risk profile (Capital Adequacy, Asset Quality, Liquidity). Safer banks will pay less; riskier banks will pay more.

- Global Best Practice: Jurisdictions like the USA (FDIC), Canada, and France already use differential premiums.

- Significance for India:

- Incentive Structure: Banks will be financially incentivized to improve their governance and asset quality to reduce premium outgo.

- Systemic Stability: It builds a more robust safety net without penalizing efficient institutions. However, the RBI must ensure that high premiums do not push already weak cooperative banks into insolvency.

4.2 Regulating Capital Market Exposure (CME)

With the Indian equity markets witnessing high retail participation, the RBI has tightened norms to prevent banking capital from fueling asset bubbles.

4.2.1 New CME Guidelines

- Tier 1 Capital Linkage: Total direct investment in capital markets and lending against securities is capped at 40% of a bank’s net worth (Tier 1 Capital), with direct investment limited to 20%.

- Acquisition Financing: Banks can lend to companies for M&A (Mergers and Acquisitions), but they cannot fund the acquisition of their own shares (which would reduce capital) or partly paid shares. Promoters must contribute at least 30% equity; banks can fund up to 70%.

- Safeguards: Loans to stockbrokers (CMIs) are restricted to day-to-day operations and cannot be used for the brokers’ proprietary trading.

4.2.2 Rationale

The guidelines act as a “circuit breaker.” By linking exposure to Tier 1 capital (the core equity that absorbs losses), the RBI ensures that a stock market crash does not threaten the solvency of the banking system. This is a lesson drawn from global banking crises where entangled banking and market risks led to contagion.

4.3 Internationalization of the Rupee

- Cross-Border Lending: Authorized Dealer banks can now lend in Indian Rupees (INR) to residents in Nepal, Bhutan, and Sri Lanka.

- Geopolitical Strategy: This is a subtle but powerful tool of economic diplomacy. By facilitating trade and credit in INR, India reduces the “dollar shortage” stress on its neighbors (who faced severe forex crises recently) and integrates their economies closer to the Indian market. It is a step towards making the INR a regional reserve currency.

5. Agriculture: Mission for Self-Reliance and Crop Diversification

The agricultural policies of October 2025 reflect a decisive shift from “food security” (cereals) to “nutritional security” (pulses/oilseeds), addressing the dual challenges of malnutrition and soil degradation.

5.1 Mission for Aatmanirbharta in Pulses (2025-31)

The Union Cabinet launched a ₹11,440 crore mission to achieve complete self-sufficiency in pulses by 2027.

5.1.1 The Structural Crisis in Pulses

- Import Dependency: India is the world’s largest producer but also the largest importer of pulses (14% of global trade). It relies on imports of Tur (Pigeon pea) from Mozambique and Malawi, and Masoor (Lentils) from Canada.

- Yield Gap: Indian pulse yields (~740 kg/ha) are significantly below the global average (~949 kg/ha) and developed nations (>1800 kg/ha).

- Ecological Necessity: Pulses are leguminous (nitrogen-fixing) and water-efficient. Promoting them is essential to break the wheat-rice cycle that is depleting water tables in Punjab and Haryana.

5.1.2 Mission Strategy and Components

The Mission adopts a “whole-of-supply-chain” approach:

| Component | Target / Action | Objective |

| Seeds | Distribute 88 lakh free seed kits; 126 lakh quintals of certified seeds. | Replace old, low-yield varieties with high-yielding, climate-resilient strains (e.g., short-duration Tur). |

| Area Expansion | Expand cultivation to 310 lakh hectares (including rice fallows). | Utilize fallow lands in eastern India after the paddy harvest. |

| Procurement (The Game Changer) | 100% Procurement of Tur, Urad, and Masoor for 4 years by NAFED/NCCF. | This removes “price risk.” Farmers hesitate to grow pulses due to price volatility; assured MSP procurement provides the safety net needed to switch crops. |

| Infrastructure | 1,000 processing/packaging units with ₹25 lakh subsidy. | Promote local value addition (Dal mills) to increase farmer share in the consumer rupee. |

5.1.3 Expected Outcomes by 2030-31

- Production: Increase to 350 lakh tonnes.

- Productivity: Increase yield to 1,130 kg/ha.

- Strategic Autonomy: Eliminating imports insulates India from diplomatic leverages (e.g., tensions with Canada affecting Lentil trade) and global price shocks.

5.2 MSP for Rabi Crops 2026-27: Signaling Diversification

The Cabinet Committee on Economic Affairs (CCEA) approved MSP hikes that structurally favor diversification.

| Crop | New MSP (₹/quintal) | % Increase | Policy Signal |

| Wheat | 2,585 | 6.6% | Standard increase to cover cost of production. |

| Safflower | 6,540 | 10.1% | Highest hike; aggressive push for edible oil self-reliance to cut palm oil imports. |

| Gram (Chana) | 5,875 | 4.0% | Encouraging pulses in Rabi season. |

| Lentil (Masur) | 7,000 | 4.5% | High absolute value encourages production. |

5.3 Fertiliser Subsidy and Soil Health

The approval of ₹37,952 crore subsidy for P&K fertilizers for the Rabi season ensures inputs remain affordable. However, the parallel push for pulses (which require less urea) indicates a long-term strategy to reduce the overall fertilizer subsidy bill, which has ballooned in recent years.

6. Energy Sector: The Electricity (Amendment) Bill, 2025

The Ministry of Power has released the draft Electricity (Amendment) Bill, 2025, aimed at the “democratization of the distribution network”. This is the most contentious and transformative reform in the infrastructure space.

6.1 Core Reform: Separation of Carriage and Content

The Bill proposes to separate the “wires” business (Carriage) from the “supply” business (Content).

6.1.1 Network Sharing Mechanism

- Proposal: The Bill allows multiple distribution licensees (supply companies) to operate in the same area using the existing network of the incumbent Discom.

- Analogy: Similar to the telecom sector, where different operators can share towers, or the banking sector, where you can use any ATM.

- Impact:

- Competition: Currently, Discoms are monopolies. Consumers have no choice. The Bill introduces competition, forcing Discoms to improve service and reduce rates to retain customers.

- Efficiency: New players can enter the market without the massive capital expenditure of laying new wires, reducing the barrier to entry.

6.2 Rationalizing Tariffs and Subsidies

6.2.1 Cost-Reflective Tariffs

The Bill mandates that tariffs must reflect the actual cost of supply. Currently, tariffs are politically determined, often kept below cost, leading to huge losses for Discoms (Operational Deficit).

6.2.2 Elimination of Cross-Subsidy

- Current Scenario: Industries pay high rates (₹8-10/unit) to subsidize agriculture/domestic users (₹0-3/unit). This makes Indian manufacturing uncompetitive globally.

- The Mandate: The Bill requires the elimination of cross-subsidies for manufacturing, railways, and metros within 5 years.

- Implication: This is a massive boost for “Make in India.” However, it shifts the burden of subsidizing farmers entirely to the State Government’s budget (Direct Benefit Transfer), which states like Punjab are vehemently opposing due to fiscal constraints.

6.3 Institutional Changes

- Electricity Council: Establishment of a Council with Union and State Ministers. Modeled on the GST Council, it aims to create a consensus-based federal framework for power reforms, addressing the “Concurrent List” challenges.

- USO Exemption: Discoms can be exempted from the Universal Service Obligation (USO) for large consumers (>1 MW) who choose open access. This prevents “cherry-picking” where large consumers leave the Discom but return when market prices rise.

7. Environmental Governance: The Carbon Market Era

India formally transitioned from “energy efficiency” to “carbon trading” in October 2025 with the notification of the Greenhouse Gases Emission Intensity (GEI) Target Rules, 2025.

7.1 The Carbon Credit Trading Scheme (CCTS)

7.1.1 Scope and Compliance

- Sectors: Cement, Aluminium, Chlor-alkali, and Pulp & Paper. These are “hard-to-abate” sectors with high emission footprints.

- Targets: 282 specific industrial units have been given legally binding targets to reduce their Emission Intensity (tCO2e per tonne of product).

- Examples: Cement sector targets reduction of 4.7-7.6%; Pulp & Paper up to 15% reduction by 2027.

7.1.2 The Trading Mechanism (Cap and Trade)

- Over-Achievers: A unit that reduces emissions beyond its target earns Carbon Credit Certificates (CCCs).

- Under-Achievers: A unit that fails to meet its target must buy CCCs from the market or pay an “Environmental Compensation”.

- Penalty: The compensation is set at twice the market price of carbon credits, creating a strong financial deterrent against non-compliance.

7.2 Strategic Significance

- Paris Agreement: This mechanism is the primary vehicle for achieving India’s NDC target of reducing GDP emission intensity by 45% by 2030.

- Global Competitiveness: With the EU implementing the Carbon Border Adjustment Mechanism (CBAM), Indian exports (steel, cement, aluminium) face taxes if they are carbon-intensive. A domestic carbon market helps Indian industries decarbonize, thereby avoiding carbon taxes in export markets.

- Evolution: This replaces the earlier PAT (Perform, Achieve, Trade) scheme which focused only on energy efficiency. The CCTS focuses directly on carbon, covering process emissions as well.

8. Digital Governance: IT Rules and the Fight Against Deepfakes

The Ministry of Electronics and IT (MeitY) introduced critical amendments to the IT Rules, 2021, focusing on accountability for content removal and the regulation of AI-generated content (Deepfakes).

8.1 Amendment to Content Removal Protocols

The amendments to the Information Technology (Intermediary Guidelines and Digital Media Ethics Code) Rules, 2025 tighten the procedure for state-ordered censorship.

- Senior Oversight: Content removal orders (blocking orders) can now only be issued by officers of the rank of Joint Secretary (Union) or Director General of Police (State).

- Reasoned Orders: Orders must explicitly state the legal basis (e.g., “public order” under Section 69A) and the specific URL.

- Periodic Review: A monthly review by a Secretary-level officer is mandated to check the validity of standing orders.

- Significance: This creates a “check and balance” within the executive. By removing the power from lower-level officials, it reduces the risk of arbitrary blocking of critical journalism or political dissent, aligning with the proportionality principle laid down by the Supreme Court (Shreya Singhal case).

8.2 Regulating Synthetic Media (AI)

New draft rules address the proliferation of Synthetically Generated Information.

- Definition: Information generated/modified by AI to appear authentic (Deepfakes).

- Mandatory Labelling: Platforms must ensure such content carries a visible label or unique identifier covering at least 10% of the display area.

- User Declaration: Significant Social Media Intermediaries (SSMIs like Meta, X, YouTube) must modify their upload interfaces to require users to declare if content is synthetic.

- Rationale: Rather than banning AI content (which stifles innovation), the government is opting for a “transparency” model. The goal is to preserve “information integrity” so citizens can distinguish between reality and fabrication, which is crucial for the sanctity of elections and public discourse.

9. Labour and Employment: The Shram Shakti Niti 2025

The Draft National Labour and Employment Policy (Shram Shakti Niti 2025) outlines a vision for a “dignified and future-ready” workforce.

9.1 Key Pillars of the Policy

- Social Security for All: Creation of a Universal Social Security Account. This integrates data from EPFO (formal), ESIC (health), and e-SHRAM (informal).

- Portability: The key innovation is portability. A migrant worker moving from Bihar to Mumbai should not lose their benefits. The account travels with the worker.

- Women’s Participation: Targets increasing Female Labour Force Participation (FLFP) to 35% by 2030. It proposes “care economy” infrastructure (creches) and flexible working hours as structural enablers.

- Formalisation via Facilitation: Moving away from the “inspector raj,” the policy proposes a “Single-Window Digital Compliance” system. MSMEs that formalize (register and pay taxes) will receive fiscal incentives, aiming to reduce the massive informal sector.

- Green Jobs: It explicitly plans for “Just Transitions”—reskilling workers in coal/thermal sectors for jobs in renewable energy and electric mobility.

10. Sectoral Reforms: Textiles, Mining, and Sports

10.1 PLI Scheme for Textiles: Course Correction

The government amended the PLI Scheme for Textiles to make it more accessible.

- Investment Thresholds Reduced:

- Part 1: From ₹300 cr → ₹150 cr.

- Part 2: From ₹100 cr → ₹50 cr.

- Analysis: The original thresholds were too high for India’s textile industry, which is fragmented. By lowering them, the government is inviting Medium Enterprises (MSMEs) to participate, specifically boosting the Man-Made Fibre (MMF) sector where India lags behind China and Vietnam.

10.2 Mining Reforms: Ending Speculation

Amendments to Mineral (Auction) Rules, 2015 introduce strict milestones.

- The Problem: Companies often win mine auctions and then sit on the assets (“squatting”) to block competitors or wait for higher prices, delaying national production.

- The Fix: Strict timelines (Mining Plan in 6 months, Environment Clearance in 18 months). Failure leads to penalty appropriation (1% of Bank Guarantee per month). This ensures mineral security for domestic industry.

10.3 Sports Governance

The Draft National Sports Governance Act, 2025 establishes the National Sports Board (NSB) and National Sports Tribunal.

- Objective: To depoliticize sports federations and ensure compliance with the Olympic Charter. The Tribunal provides a specialized forum for disputes, removing them from the slow civil court system.

11. Parliamentary Oversight Agenda (2025-26)

The Standing Committees of Parliament have identified critical future-looking subjects for examination. These agendas signal the areas where the legislative branch feels executive gaps exist:

- Chemicals & Fertilisers: Evaluation of DBT in fertilisers (checking diversion) and Self-sufficiency in APIs (drug security vis-a-vis China).

- IT & Communications: Implementation of media laws and the definition of “Urban Areas” for Census (crucial for delimitation and urban fund allocation).

- Coal: “Future of Coal in India’s Energy Mix”—balancing energy security (coal) with climate goals (Net Zero).

12. Conclusion: The Path to 2047

The policy landscape of October 2025 reveals a mature governance strategy that is willing to take short-term political risks for long-term structural gains.

- Fiscal Federalism: The 8th Pay Commission’s mandate to study “unfunded pensions” sets the stage for a decisive confrontation with the populist reversion to the Old Pension Scheme.

- Market Efficiency: Whether it is the “Risk-Based Premium” in banking, “Network Sharing” in electricity, or “Carbon Trading” in environment, the government is consistently choosing market mechanisms over administrative fiat to drive efficiency.

- Strategic Autonomy: The “Mission for Pulses” and “PLI for Textiles” are not just economic schemes; they are strategic tools to reduce import dependency and create domestic resilience in food and employment.

- Digital Maturity: The IT Rules amendments show a government moving from “reactionary banning” to “procedural regulation,” acknowledging that in the AI age, transparency (labelling) is a more effective tool than censorship.

For Civil Services aspirants, these developments underscore the interconnectedness of the syllabus. A question on Food Inflation (GS-3) cannot be answered without referencing the Pulses Mission. A question on Center-State Relations (GS-2) is incomplete without discussing the Electricity Bill and 8th Pay Commission. The policies of October 2025 provide the raw material for understanding the structural transformation of India.

Appendix: Statistical Snapshot (October 2025)

| Indicator | Value | Context |

| Repo Rate | 5.50% | Neutral Stance |

| GDP Growth (Proj.) | 6.8% | Upgraded for 2025-26 |

| CPI Inflation (Q2) | 1.7% | Food Deflation (-1.6%) |

| Pulses Mission | ₹11,440 Cr | Self-sufficiency by 2027 |

| Safflower MSP | ₹6,540/qtl | +10.1% Hike |

| Textile PLI (Min) | ₹50 Cr | Lowered Investment Cap |

| Carbon Targets | Mandatory | 282 Industrial Units |

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses