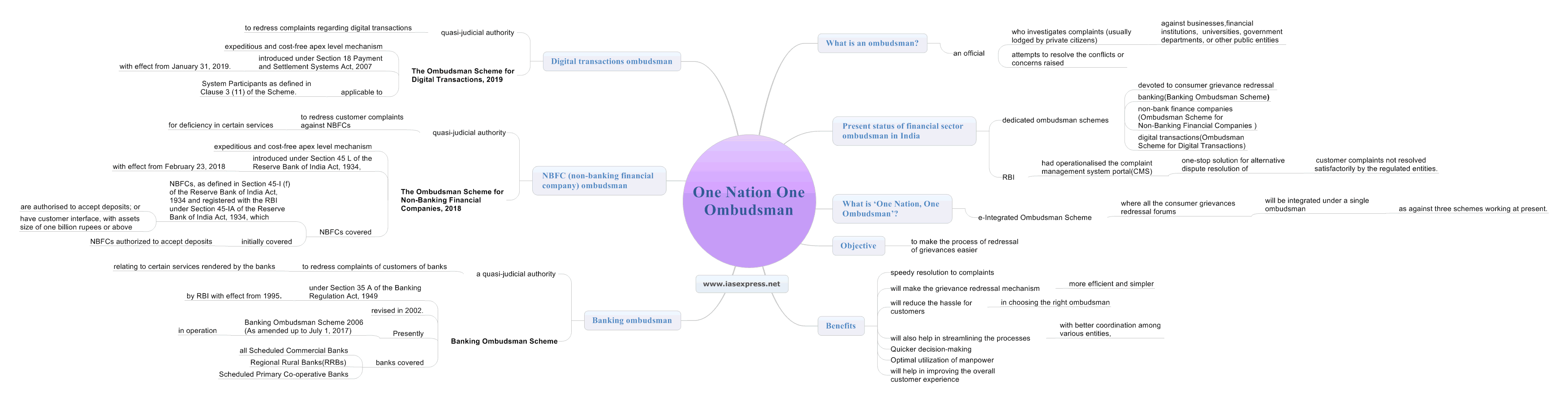

One Nation One Ombudsman – Objectives and Benefits

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

The Reserve Bank of India (RBI) in a recent move has announced that it will be integrating consumer grievances redressal under a single ombudsman as against three schemes working at present. The move comes at a time when there is an increase in digital transactions and the consumers have to face a lot of problems while getting their complaints redressed. The move is a step forward in the direction of customer empowerment and is an initiative towards providing speedy and inexpensive redressal to millions of users of India’s banking and non-banking infrastructure.

What is an ombudsman?

An ombudsman is an official, usually appointed by the government, who investigates complaints (usually lodged by private citizens) against businesses, financial institutions, universities, governRelated Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses