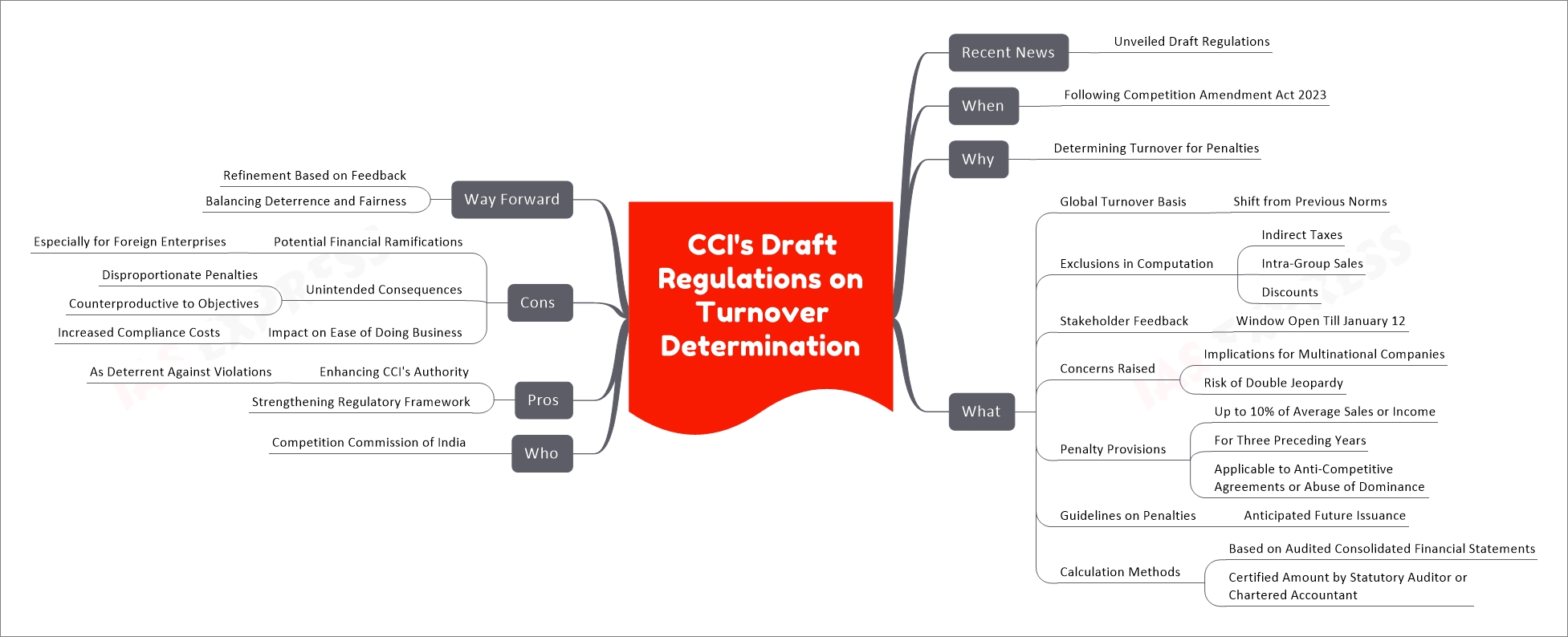

CCI’s Draft Regulations on Turnover Determination

To summarize, the CCI’s draft regulations on turnover determination are pivotal in shaping the penalty framework for anti-competitive practices. By shifting to a ‘global turnover’ basis for penalties, the CCI aims to strengthen its deterrent capabilities. However, this approach has raised concerns about disproportionate financial implications, especially for multinational companies and enterprises with a global presence. The CCI is currently soliciting public feedback to refine these regulations, indicating an effort to balance effective deterrence with fairness and practicality in enforcement.

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses