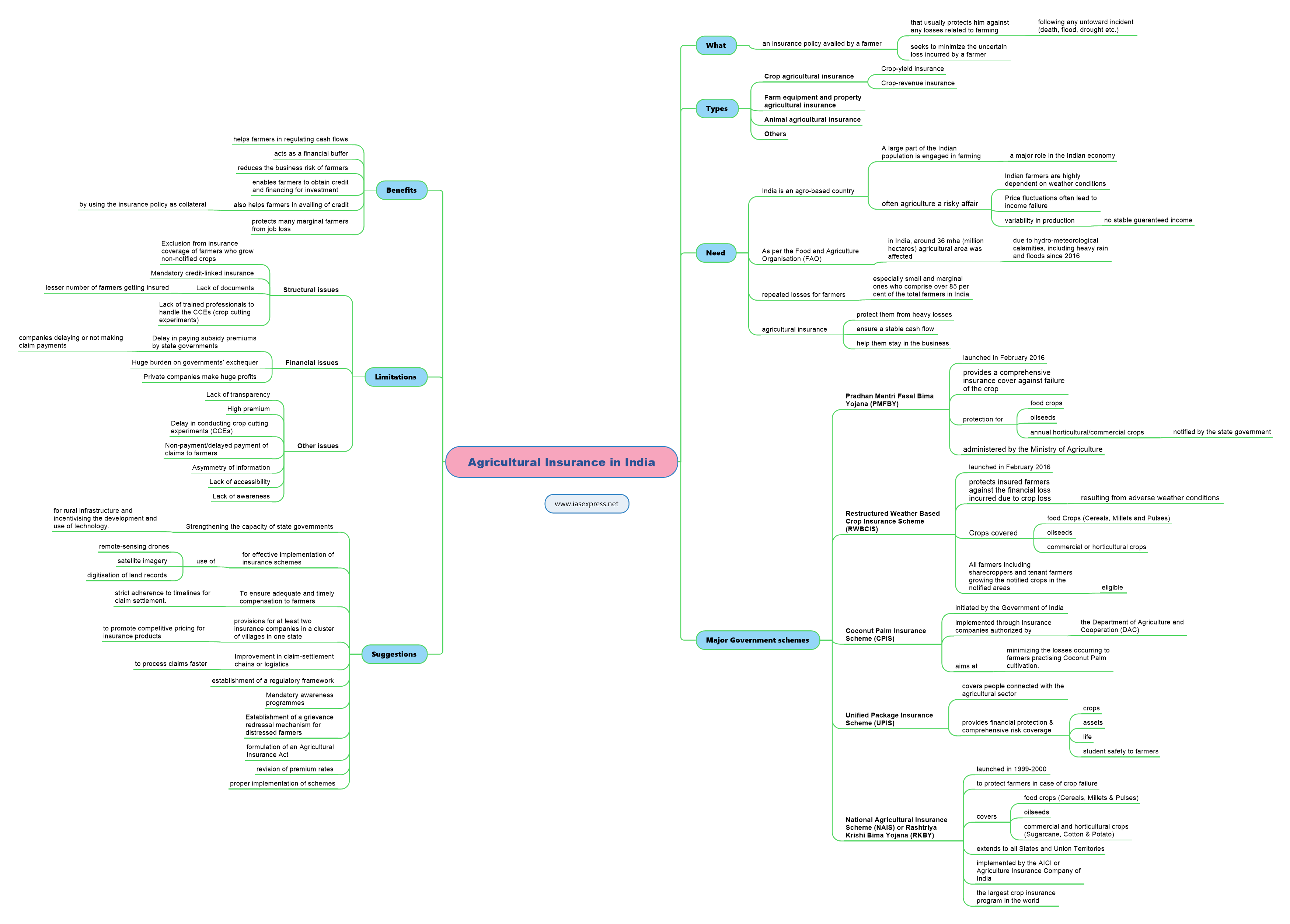

Agricultural Insurance in India – Benefits, Limitations and Way Forward

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

Although India is an agro-based country and farmers and farming activities form an integral part of the Indian economy yet the farmers in India have been facing numerous issues since time immemorial. Beginning from the uneven nature of the Indian monsoon to its unpredictability, it has always been a difficult situation for farmers to ensure a stable income for themselves and protect themselves from losses they incur while carrying out farming. Given this situation, agricultural insurance has always been thought of as being the way forward. However, there are several facets to this subject that need to be looked into to get a real picture.

What is agricultural insurance?

Agricultural insurance refers to an insurance policy availed by a farmer

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses