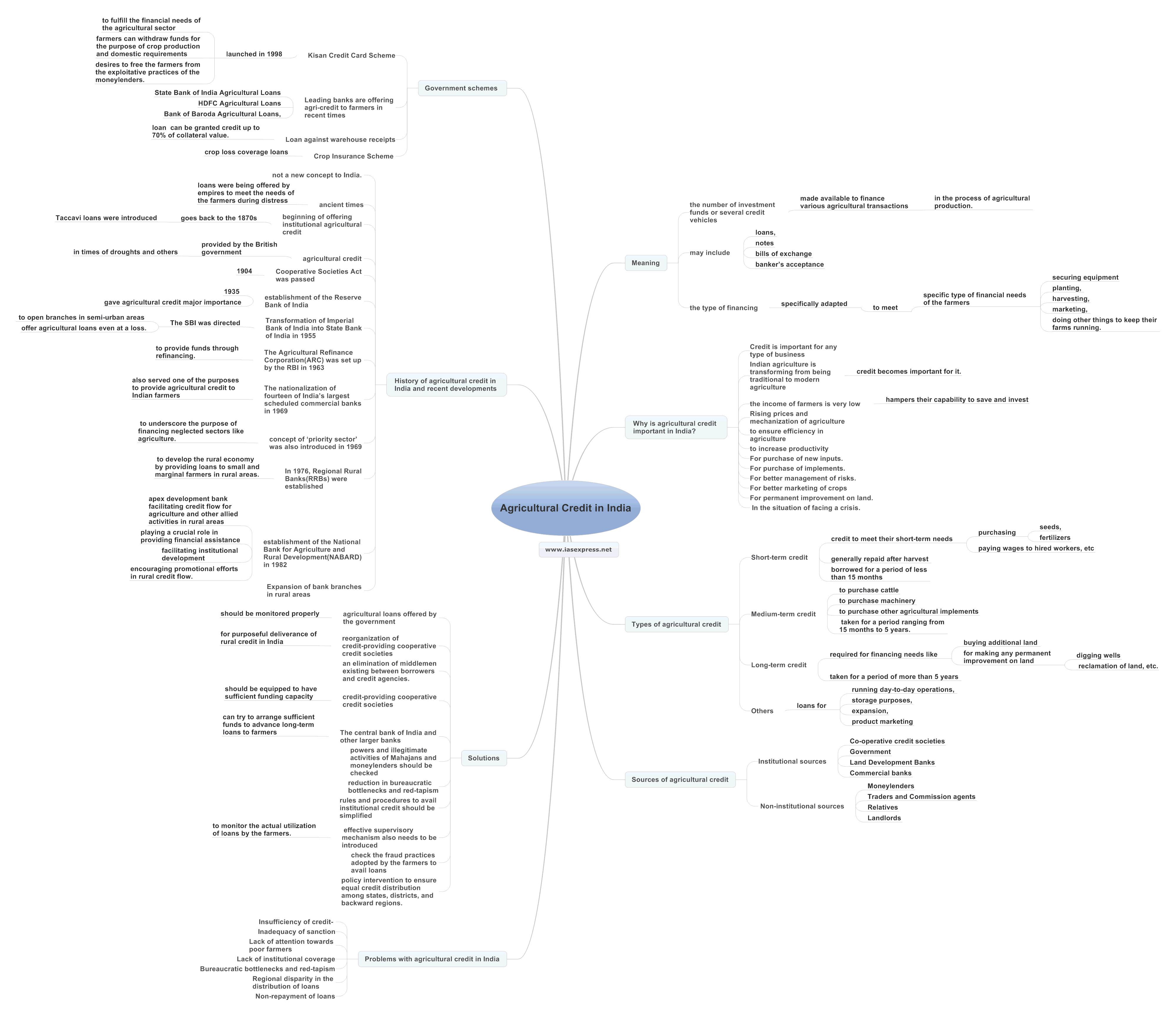

Agricultural Credit in India – Types, Sources, Problems and Way Forward.

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

In recent times, with the ongoing farmers’ agitation near the Delhi-Haryana border, agriculture as an issue has again captured the limelight. Various issues related to farmers have cropped up. The Union Government has dedicated a significant part of the 2021 Budget towards providing agricultural credit to the farmers. As the country is facing a number of problems in agriculture of which financing the agricultural needs tends to be a major issue, agricultural credit has become an important subject now to discuss and to pay attention to.

Meaning

Agricultural credit is the number of investment funds or several credit vehicles made available to finance various agricultural transactions in the process of agriculturRelated Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses