State Revenue – Loss In Times Of Lockdown

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

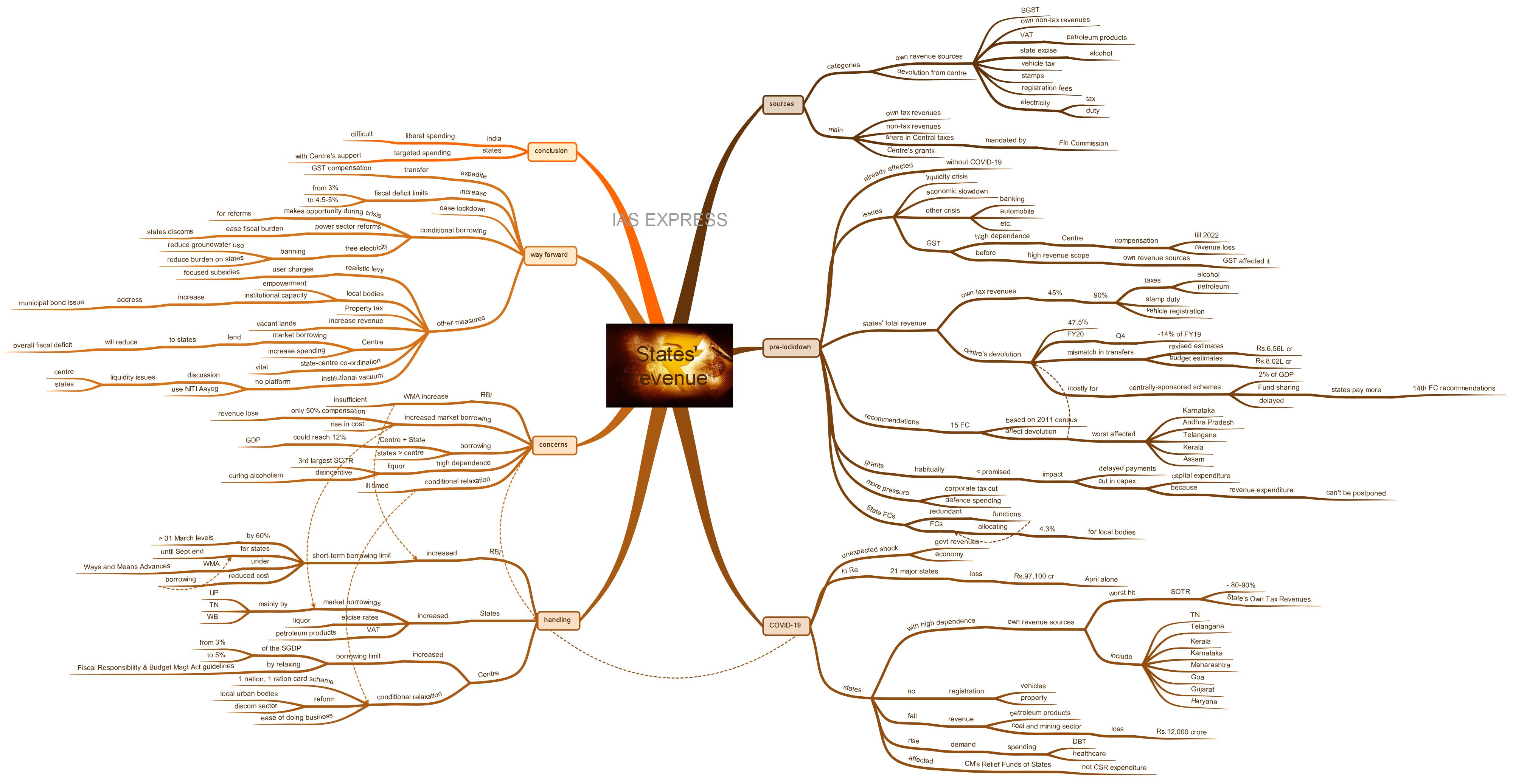

With the imposition of nationwide lockdown and the resulting near-standstill in economic activity, the revenue sources of the government have taken a major hit. Both central and state governments are struggling with drying up of revenues, while simultaneously dealing with increased demand for expenditure in light of the COVID-19 crisis. However, the state governments are affected more as the bulk of expenditure takes place at the state level. Unlike the central government, many of the states depend on the central devolution of funds for its finances.

What are the sources of state revenues?

- The sources of state revenue can be classified under 2 heads:

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses