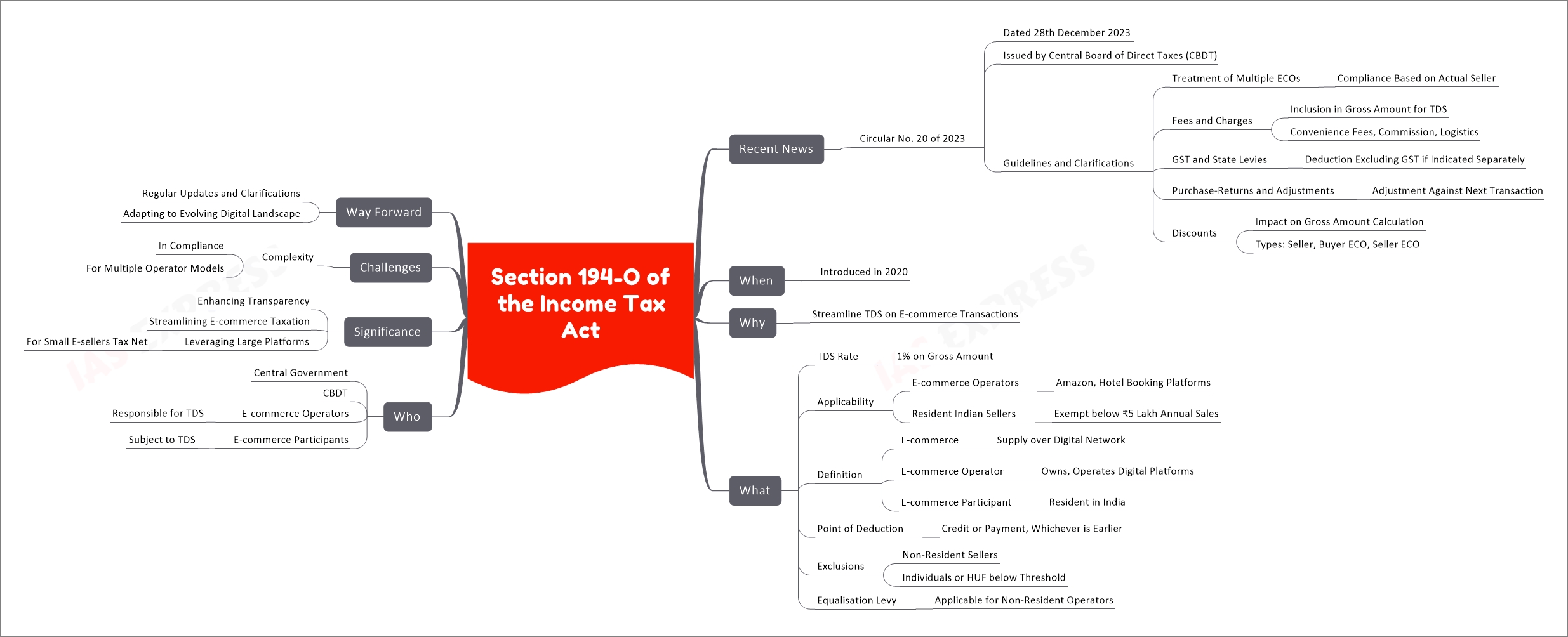

Section 194-O of the Income Tax Act

Section 194-O of the Income Tax Act, introduced in 2020, mandates e-commerce operators in India to deduct Tax Deduction at Source (TDS) at a rate of 1% on the gross amount of sales or services facilitated through their digital platforms. It covers resident Indian sellers and enterprises, termed e-commerce participants, and exempts those with annual sales below ₹5 lakh. The provision aims to streamline the taxation process for e-commerce transactions, enhancing transparency and compliance in the digital economy. The guidelines issued by the Central Board of Direct Taxes (CBDT) address various aspects of TDS deduction, including the treatment of fees, GST, purchase-returns, and discounts, ensuring clarity for multiple e-commerce operator models.

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

Responses