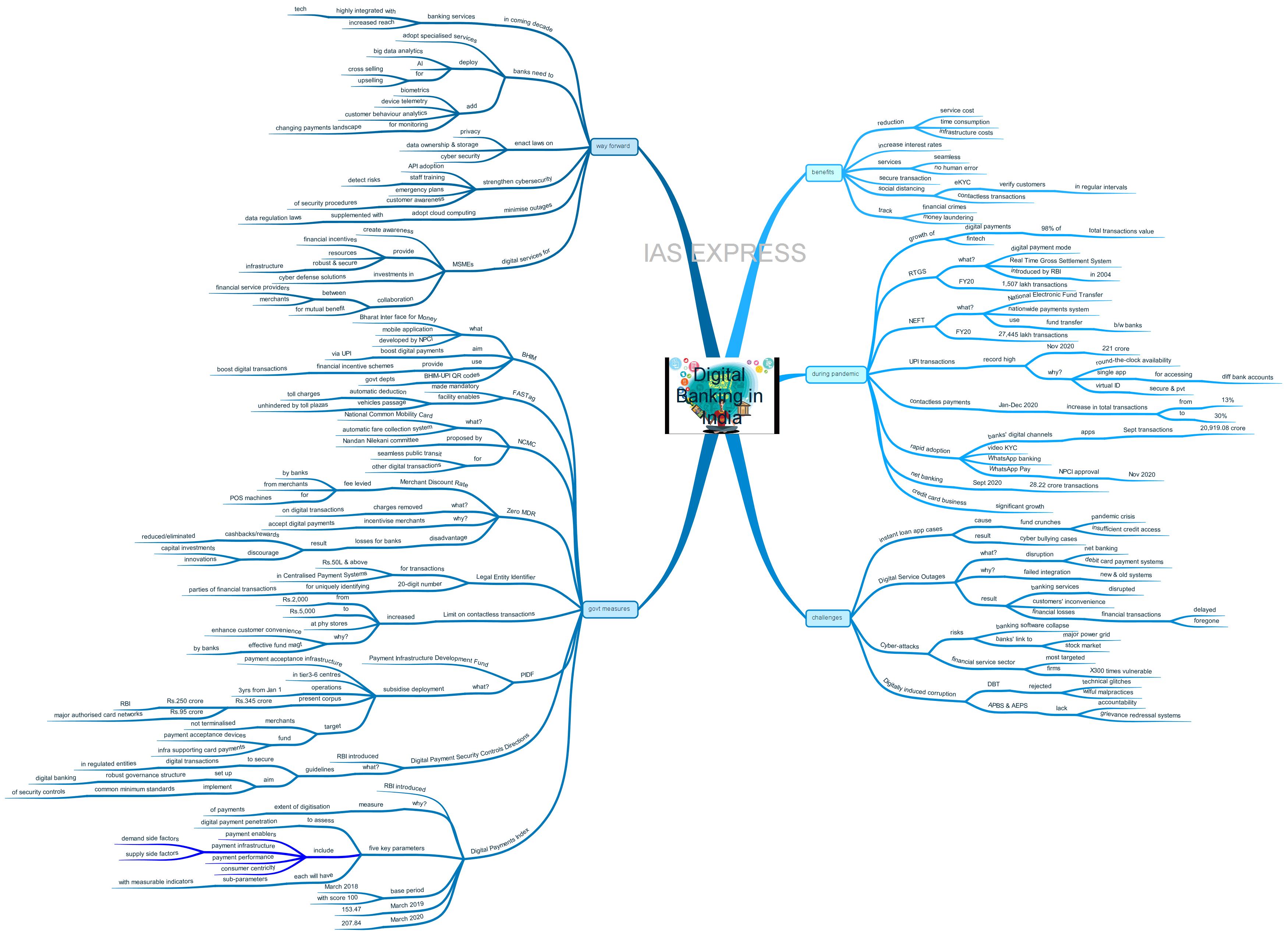

Digital Banking During Pandemic – All You Need to Know

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

With the advent of COVID-19 crisis, social distancing has become the new normal. This has caused a surge in adoption of digital banking and payment solutions across the world. In India, banks are rapidly moving towards digital transactions, regardless of infrastructural challenges and glitches. This has led to instances of outages. These rapid changes may also cause potential threats of increased cybercrimes, which are novel and needs to be addressed efficiently in a rapid manner.

What are the benefits of digital banking?

- Digital banking reduces financial services costs, time consumption and infrastructure costs as majority services will be

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses