Corporate Ownership of Banks – Challenges & Way Ahead

From Current Affairs Notes for UPSC » Editorials & In-depths » This topic

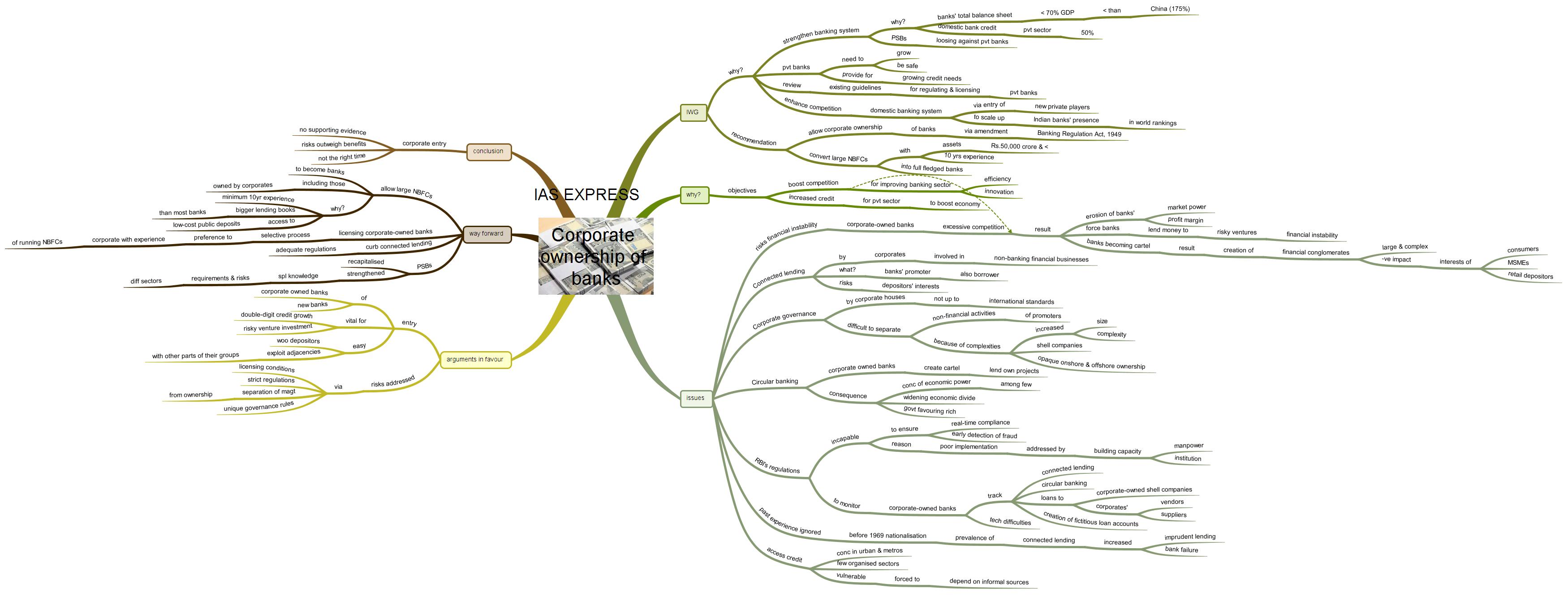

The RBI had recently released a report of the Internal Working Group that reviewed the current licensing and regulatory guidelines related to the ownership, control and corporate structure of private banks. This group’s most controversial recommendation was to allow corporate and industrial houses to promote and operate banks within the country. With banks playing a critical role in the economy, this recommendation, if implemented, will have large-scale implications in economic growth.

Why was RBI’s Internal Working Group set up?

- The banking system plays a critical role in sustaining the economic growth of a country.

- The Indian banking system has undergone significant changes since independence when the private ownership of banks led to a large

Related Posts

If you like this post, please share your feedback in the comments section below so that we will upload more posts like this.

{kind=link}

Responses